Monthly Market Rollup: May to June 2024

Landing a jet on an aircraft carrier is like "landing on a postage stamp." But with interest expense eclipsing defense spending for the first time, it's the US Treasury coupon making the hard landing.

Hello again to our Monthly Market Rollup for the end of May 2024. We aim to send out these chart heavy market summaries at the turn of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes up into an Economic watch currently focused on the potential for a Recession, an Inflation section, and a Fed focused section, along with a Conclusion. Enjoy!

Introduction:

U.S. Naval Aviators have long said that landing a jet on an aircraft carrier is like "landing on a postage stamp." So this month with interest expenses surpassing defense spending for the first time in US history, the real challenge now is figuring out how to land the rest of the US Federal Budget as net interest expense keeps expanding amidst ongoing Inflation concerns.

Source: https://www.tftc.io/us-interest-payments-surpass-defense-budget/

Original Source: https://finance.yahoo.com/news/us-federal-budget-crosses-grim-milestone-as-interest-payments-overtake-defense-spending-155521072.html

“But hasn’t Interest Expense always been a big component of the Federal Budget?” You ask.

No. No it hasn’t.

Source: https://x.com/GameofTrades_/status/1791853753823359229

But before we dive in to what to expect about Inflation, let’s cover the table stakes for this discussion. (Please check out last month’s note if you have any questions.)

The Fed is passive and apolitically minded in this election year.

‘Fiscal Dominance’ is real.

More inflation is coming this summer.

We see Recession indicators pointing towards a market downturn at some point in 2025.

Jay Powell wants to jawbone markets for the foreseeable future without having to change rates but while making you think he might change rates, both with fantom hikes and fantom cuts.

Meanwhile, it’s an election year and Yellen is spending like crazy. So long term inflation remains a challenge.

10yr UST rates have decoupled from Gold (see our April Leads note if you are a subscriber) on the geopolitical front, so god help us all.

USD will still be the reserve currency for the foreseeable future, but long bond Treasuries might not be the reserve asset that they once were.

Everyone still here? Ok, good.

Last month we landed on a precarious set of potential scenarios for this summer, with the key themes that inflation was now getting the attention it deserved, which put the Fed’s apolitical stance at odds with the potential that inflation keeps ticking higher into the summer.

Really though, the Fed is happy to let some excess inflation chew through the Federal debt in real terms.

Most importantly, the US Treasury market remains stable.

US Treasury market stability in this context is the opposite of the mini banking crisis last year of Signature Bank and Silicon Valley Bank. The US Treasury market became unorderly in that period, and the Fed is determined to keep that from happening any time soon.

That ‘shadow mandate’ of UST market stability trumps the Inflation and Unemployment mandates that are on the books. (For more on this please read and watch Luke Gromen.)

For now, let’s take a look at what’s driving that ballooning Net Interest Expense: Inflation and Inflation Expectations.

Inflation Watch:

First off, commodity prices are up for the year:

Source: https://x.com/JesseCohenInv/status/1792980764939677799

But Inflation is lagging commodities:

Source: https://x.com/TaviCosta/status/1792560022347555215

Copper is forecasting higher prices:

Source: https://x.com/AndreasSteno/status/1790465482069271030

Inflation surprises are forecasting higher CPI:

Sources: https://x.com/AndreasSteno/status/1792209226590486534

Shipping rate futures are moving higher:

Source: https://x.com/AndreasSteno/status/1794756966000001340

The US Dollar is falling:

Source: https://x.com/GameofTrades_/status/1792935883143880797

Now, let’s look at how the Economy is doing and why we see a Recession on the 2025 horizon, but not in 2024.

Economy Watch:

As a reminder the Yield Curve has been underwater for a considerable amount of time.

Source: https://x.com/GameofTrades_/status/1787150260277563435

The net savings rate is low:

Source: https://x.com/GameofTrades_/status/1792956016289796102

While credit card default rates are up:

Source: https://x.com/GameofTrades_/status/1791478781737312447

On a larger amount of credit card debt:

Source: https://x.com/great_martis/status/1792958979938853181

Unsurprisingly, multifamily delinquencies are up:

Source: https://x.com/GameofTrades_/status/1793674522094436733

With elevated lending costs and exhausted savings, buying conditions for Houses, Cars, and Durables are all at relative low points - looking back over the last twenty five years:

Source: https://x.com/KobeissiLetter/status/1795111781620175118

Which is leading to a contraction in Median home prices (though some of this is post Covid mean reversion):

Source: https://x.com/GameofTrades_/status/1792193495526199699

Loan availability is becoming a challenge for small businesses and is foreshadowing increased jobless claims:

Source: https://x.com/MichaelAArouet/status/1792453086251978759

The Kansas Fed Labor Market Conditions Index is indicating an eventual increase in Unemployment as well:

Source: https://x.com/MichaelAArouet/status/1793530622453100687

Broadly speaking, small companies have a harder time in Recessions than larger companies, and Russell 2000 earnings are trending towards the type of negative earnings levels we see in Recessions:

Source: https://x.com/GameofTrades_/status/1791498925507285047

Some other indicators are pointing towards a Recession as well, like the Year-on-Year growth in Unemployed Persons 3 month moving average:

Source: https://x.com/MichaelKantro/status/1786522462701715859

But in all of this, we have not yet seen both a steepening yield curve and risising unemployment together that signals the Recessions begining:

Source: https://x.com/GameofTrades_/status/1790391050986754453

And without those double triggers, we would not say that a Recession is imminent.

Geopolitics:

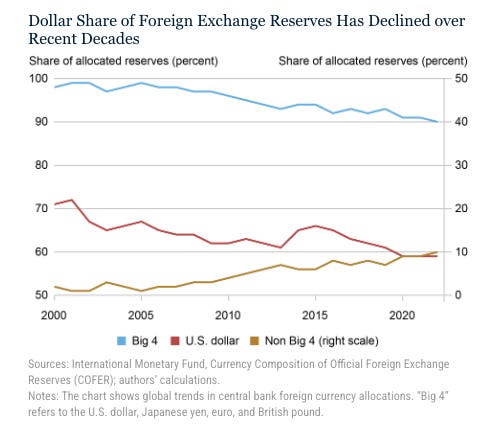

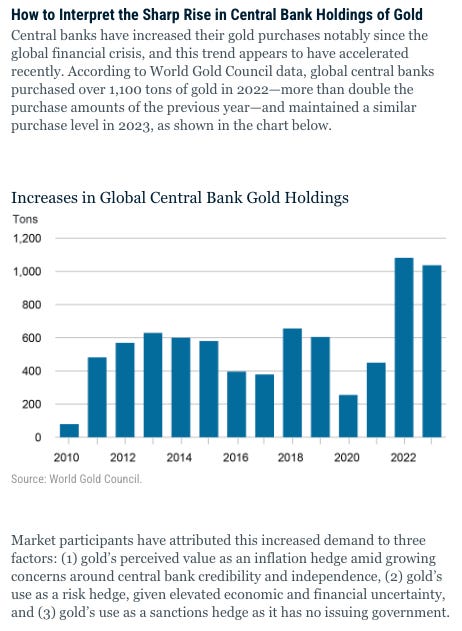

Before we get to the Fed, we need to put of attention on Gold as a Geopolitical instrument:

Recently, the Federal Reserve Bank of New York wrote recently a summary of the recent increase in Gold reserves and the next three images are all from that article (link):

Notably, “[m]ore than half of reported gold accumulation since 2009 was from China and Russia“.

Original Source: https://x.com/balajis/status/1796208316907126841

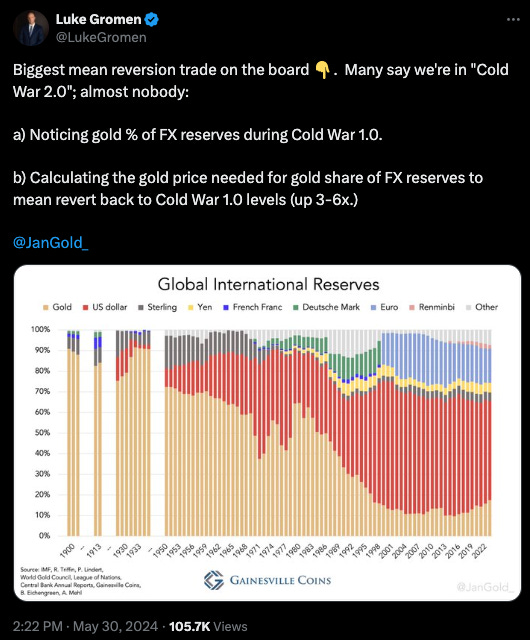

The upside here for Gold looks like a 1981 Cold War scenario:

Source: https://x.com/LukeGromen/status/1796276029356384504

All of this comes with Gold now beating Bonds on a 50 year lookback:

Source: https://x.com/MichaelAArouet/status/1793664825081692482

All this Gold watching is -in my view- related to the Fed’s challenge of maintaining US Treasury Market stability. So let’s check in on that topic next.

Federal Reserve Watch:

With more inflation coming this summer, the question of predicting the Fed’s actions becomes one of trying to understand the timeline for the pending market downturn that we are seeing on the horizon in the Economy.

That said, in the US there is an ongoing dynamic that higher interest rates are hitting Multifamily, Credit Card debt, and new buyers much more than existing home owners, because US home buyers are mostly able to lock in long term fixed rate mortgages, usually on 30 years mortgages.

This dynamic also means that US consumers are much less sensitive to interest rates than their European counterparts whose mortgages are likely to be floating.

Commercial Real Estate loans (with usually a five to ten year time duration) remains the next shoe to drop in the US as many of the pre-covid era loans are coming up for a much needed refinancing, with regional bank losses being one harbinger of the lurking damage to this sector.

Source: https://x.com/Barchart/status/1795977819094188183

Separately, in terms of election years, we are already in the upper handful of SP500 returns for the year (the red line in the chart below is 2024).

Source: https://x.com/granthawkridge/status/1794964627560014063

Conclusion:

My view from last month hasn’t changed much.

The Fed’s position remains a challenging one, but it is one the Fed can muddle through with so long as US Treasury market plumbing doesn’t break, and the US Dollar weakens.

Those things seem to be happening, so with an attentive eye on CRE and regional banks, we should see the Inflation trade move forward for the time being.

The potential move from Treasuries to Gold continues to be a big deal.

Recession remains a post election concern if markets remain functioning.

There’s a Goldilocks scenario this election cycle where some exposure to duration bonds could become an amazing asymmetric trade depending on how the global market interprets the election’s outcome. Not because there will be a belief that the twin deficits will be contained, but that some combination of growth factors (shale and nuclear enabled energy abundance, an AI fueled productivity and US manufacturing/mining boom amidst re-shoring concerns, and the prospect of a contained regulatory apparatus) will draw in global investment as global inflation erodes global purchasing. In this Goldilocks scenario a virtuous cycle of lower long term US rates gives the US CRE market another refinancing opportunity, which in turn enables more growth all around. But the likelihood of this scenario is hard to peg down.

However, in that vein of thinking, it’s worth reminding everyone that GDP per capita loves energy consumption:

Source: https://x.com/ConceptualJames/status/1793338142340120963

That’s all for this month, but before we adjourn until mid June, here’s something to remind you that your poor understanding of Bitcoin is only in its infancy.

Source: https://x.com/nsquaredvalue/status/1793013885144006862

Until next month.

Please subscribe if you haven’t already and consider our Pro Tier if you would like direct on-demand access to my entertaining views on the Economy.

Intriguing insights and correlations!