Monthly Market Rollup: End of June 2024

Nothing's broken yet with Regional Banks and CRE, so for the time being - So goes Nvidia, so goes the market.

Hello again, and welcome to our Monthly Market Rollup for the end of June 2024. We send these chart heavy market summaries at the beginning of each new month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes up into an Economy section currently focused on the potential for a Recession, an Inflation section, a Geopolitics section, and a Fed focused section along with a Conclusion. Enjoy!

Introduction:

Well, we are back at it after another month. We are now halfway into the summer, and the market is bouncing along at all time highs. This despite Nvidia, crypto, and gold all falling off a bit, and much of the Economy signaling an impending Recession.

Broadly the Economy seems to be bifurcated, with much of the Economy experiencing declining numbers, while a small group of the AI fueled stocks experiencing a different world.

And for awareness, let’s take a quick look at Nvidia’s share of the market:

Source: https://x.com/burrytracker/status/1802845509029359697

Wow. What should we make of that amount of the market being wrapped up in the AI story?

But how is the rest of the market doing?

Well, before we dive in, let’s do a quick recap of last month.

The Fed's position remains challenging but manageable as long as the US Treasury markets’ plumbing doesn't break, and the US Dollar weakens.

The inflation trade is likely to continue in the near term, though again assuming nothing breaks with Commercial Real Estate (CRE) and regional banks.

The potential Geopolitical shift from Treasuries to Gold continues to be a significant factor in the ongoing US Dollar story. Though I’ve had additional thoughts on this in my mid month Leads note.

A Recession remains a concern for the post-election period, assuming that markets remain functional until then.

On a longer term horizon, the relationship between energy consumption and GDP per capita may spur future growth if the Economy can shrug off potential breaking points and Recession indicators. The US is set up for an amazing run if it can get out of its own way.

The Election looms large over everything. Fiscal goodies are expected in the coming months, which could coincide with our Inflation views.

Additionally, it seems like drama is brewing around the Democratic Party’s Nomination.

With that review in place, let's see where things are headed.

Inflation Watch:

On the inflation side, we are still looking at a likely upswing in the next few months:

For starters, US M2 expanding:

Source: https://x.com/GameofTrades_/status/1807443985419444641

Globally, Central Banks are in an easing cycle despite the Fed staying put on rates:

Source: https://x.com/crossbordercap/status/1800898557375033787

Shipping rates and commodities prices are both headed up:

Source: https://x.com/crossbordercap/status/1795827049921454393

And importantly, those shipping rates lead inflation:

Source: https://x.com/AndreasSteno/status/1800615302285443115

Global Liquidity has a cyclicality to it, and though it had a more pronounced rhythm in the last century, it appears ready to increase in the near term:

Source: https://x.com/martypartymusic/status/1801297536604352964

That all said, on the other side of the Inflation debate we see a declining number of small business (26%) with planned price increases…

… though this is still above the norm of the last few decades and still an increase.

Source: https://x.com/ericwallerstein/status/1799821246756175958

Economy Watch:

Turning to the Economy, the Yield Curve is not optimistic about where we are headed…. though the curve has not started to de-invert yet, so the Recession is not imminent, just likely a few months off:

Source: https://x.com/RonStoeferle/status/1800425283310543346

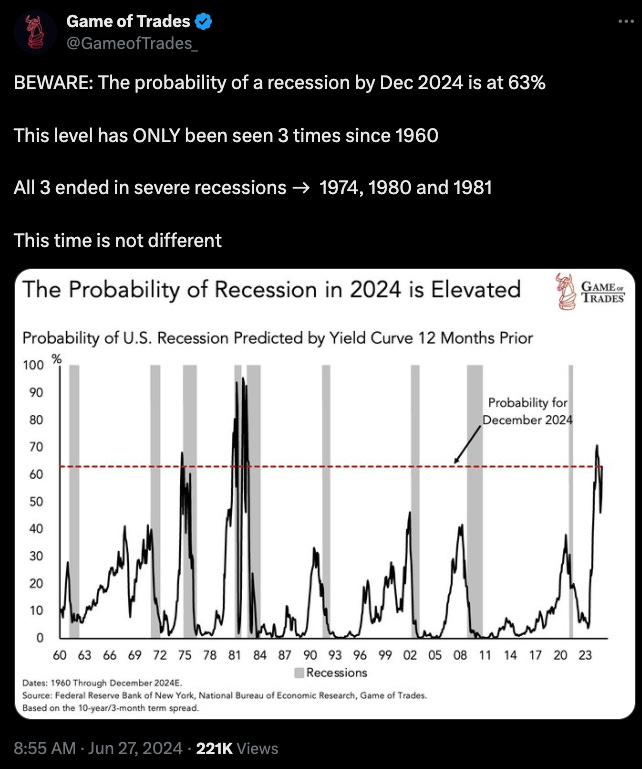

By taking the yield curve as a prediction tool we can say that the enormity of our current yield curve is comparable only to 1974, 1980, and 1981 over the last 60 years:

Source: https://x.com/GameofTrades_/status/1806340458810884335

Let’s focus on the dramatic oscillations of the early 1980s for a moment.

In that period we had a perceived weak President (fair or not) in Jimmy Carter, along with rampant inflation, and the drama of moving in and out of an inverted yield curve before inflation was finally put under control by the Volcker Fed.

That drama of moving in and out of yield curve inversion, more-so than the potential for a Recession, undercut market stability.

Here’s a Log Scale chart of the SP500 showing the relative weakness of the market during that period:

Source: https://www.macrotrends.net/2324/sp-500-historical-chart-data

Turning back to the current moment let’s look at a few leading Economic indicators…

Median Home prices are contracting (though it may be just a post-2020 reversion to the mean):

Source: https://x.com/GameofTrades_/status/1804544884122275884

Banks are tightening lending standards on Commercial and Industrial Loans, though not as dramatically as recent months:

Source: https://x.com/GameofTrades_/status/1804877066711568574

And on the heels of that tightening, we have a declining number of construction starts, most dramatically with industrial constructions:

Source: https://x.com/PeterBerezinBCA/status/1807061554199732288

Which is in line with the stalling we are seeing in Industrial Production:

Source: https://x.com/GameofTrades_/status/1803417448575848449

And despite the cheap Energy situation that we focused on in my mid month note, there’s an ongoing drawdown in Energy stocks:

Source: https://x.com/marketplunger1/status/1807086382256447930

With lower numbers of construction projects, we should see lower Employment numbers in certain areas, and indeed we are.

We have Trucking Employment remaining down year-over-year, which often leads private sector employment:

Source: https://x.com/GameofTrades_/status/1805978071230542179

Separately, and for your awareness, public sector employment has been adding new positions at a fast clip:

Source: https://fred.stlouisfed.org/series/USGOVT

Labor market conditions look like they are pointing towards a higher level of unemployment:

Source: https://x.com/MichaelAArouet/status/1798963822851698752

Job openings are declining:

Source: https://x.com/GameofTrades_/status/1803031043978703323

Small business hiring plans look really bad:

Source: https://x.com/MichaelAArouet/status/1798320697070277108

Permanent job losses accelerated, but have yet to move up dramatically:

Source: https://x.com/GameofTrades_/status/1803095326578151793

The need for Temporary help is collapsing. This usually happens near sharp economic downturns, but the slope of the decline is not the same as what we’ve seen in previous sharp downturns:

Source: https://x.com/GameofTrades_/status/1803115458587148507

And with all these Employment issues, it’s no wonder that we are starting to see rising Consumer loans default rates:

Source: https://x.com/GameofTrades_/status/1797991788428644585

And Credit Card defaults at small banks are spiking:

Source: https://x.com/GameofTrades_/status/1799109061725782473

And with Investor Sentiment at a high (which often happens before a selloff) it isn’t too hard to imagine that we’re near a market inflection point of some type if you’re ready to go to war with Nvidia’s ticker:

Source: https://x.com/GameofTrades_/status/1805957969521328477

Geopolitics:

In Geopolitics, my focus is on the tension around the US Dollar, Gold vs. US Treasuries as a reserve asset discussion, and the strengthening Energy complex within the US.

(For more details on my current thinking please subscribe and read my last Leads note.)

So turning to the US Dollar and US Treasuries for now, we see some signs of strain.

The USDJPY pair is out of sync with 5yr real rates:

Source: https://x.com/AndreasSteno/status/1806409923053420860

The yield error on US Treasuries (which is a measure of Treasury market liquidity) is at 14 year highs.

Source: https://x.com/GlobalMktObserv/status/1806001978302152946

We discussed it a bit in the mid-month Market Leads note, but the Saudis have dropped the US dollar as a payment mechanism for selling Oil. Under normal circumstances this would portend bad things for the US Dollar, but amazingly, the Dollar is showing some strength over recent weeks.

My partial answer is that the US Energy sector might be the primary reason for that Dollar strength.

Source: https://x.com/MichaelAArouet/status/1803694534003421551

For more please subscribe and read the Leads note from mid June. We cover the U.S. energy sector advantage, the potential for this energy advantage to lead to a refinancing opportunity in the curve belly and in longer term durations, along with the Fed’s divergence from other Global central banks.

Federal Reserve Watch:

We’ve discussed it before, but for the moment the Fed seems to be able to plug holes in the banking sector despite the simmering CRE and Regional Bank situation:

Source: https://fred.stlouisfed.org/series/RPONTSYD

So unless something breaks, we continue to think the Fed will try to keep rates where they are.

My estimation is that Inflation will come along in the next month or so (as we’ve seen above in the Inflation section), and I think the Fed will want the flexibility to make the market think it can raise rates, even if the Fed doesn’t raise rates ultimately.

The Fed is well placed to move the market with their words, without the need to move it with their actions.

And with the Fiscal side still in the driver’s seat, we think the Fed will play for time and keep rates flat if they can in this higher-for-longer world where Treasury markets are so attentive to the twin deficits along with the spending habits of the US Government.

Conclusion:

Every month as I’m writing this note I pull up the last few note’s conclusions so I can see what I’ve written in the recent past.

And once again, my view of this market hasn’t changed much. Though I have shifted my thinking a bit on the Dollar.

The Fed’s position remains a challenging one. But I think the odds are that the Fed can muddle through with this situation- so long as US Treasury market plumbing doesn’t break.

The CRE and regional bank challenges remain the key focus areas for that (US Treasury market plumbing) at the moment.

The potential move on the Geopolitical stage from Treasuries to Gold is important, but with the US Energy sector in such a great position, there’s likely more strength in Treasuries and the Dollar than the Inflation watchers would like us to think.

Recession remains on my post election dance card - but maybe (just maybe) there’s some weird way out of the pending surge in unemployment - maybe if industrial construction lending can pick up the pace.

Until next month.

Please subscribe if you haven’t already and also please consider our Pro Tier.