Monthly Market Rollup: April to May 2024

Welcome to the Summer of the Passive Fed! Where hot Inflation and even hotter long bond rates threaten to melt away market stability. Can Powell's apolitical stance withstand the heat?

Hello again to our Monthly Market Rollup for the end of April 2024. We aim to send out these chart heavy market summaries at the turn of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes up into an Economic watch currently focused on the potential for a Recession, an Inflation section, and a Fed focused section, along with a Conclusion. Enjoy!

Inflation Watch:

Inflation!!!

After last month’s note, and the market’s change in opinion on the number of Fed rate cuts this year (from 3 rate cuts to something closer to zero, with a dash of probability of even a rate hike), I’ve moved the ‘Inflation Watch’ section to the top of the note.

So, let’s check on where this Inflation thing might be headed next, now that we are all on the same page.

First off we have Copper signaling more strength to come in prices:

Source: https://x.com/AndreasSteno/status/1779910257398960481

And the rest of the commodity index is agreeing with that direction:

Source: https://x.com/AndreasSteno/status/1777428130916954303

Which is linked to rising supply chain costs:

Source: https://x.com/AndreasSteno/status/1779765501138256373

And which seems unlikely to slow down given the ongoing Red Sea shipping issues

Source: https://www.ft.com/content/434ba2c0-fd47-44e0-92a3-cafddce09769

Separately, the National Federation of Independent Business survey of price plans show potential upside for CPI:

Source: https://x.com/RBAdvisors/status/1777713579908898983

The Financial Conditions Index (FCI) leads CPI by six months and points to rising inflation towards the end of the summer:

Source: https://x.com/AndreasSteno/status/1785756162773651639

And in a possible act of chart-crime, here’s a “Bitcoin as a 3 month lead of Inflation” chart that signals more Inflation to come as well - despite the recent Bitcoin selloff:

Source: https://x.com/MikaelSarwe/status/1778044355120377862

As I go through charts each month, some charts stand out to me that are a bit off the beaten path, that I find pretty interesting.

Here is one such interesting chart, showing the motor vehicle insurance component of inflation and the rollercoaster it’s been on over the last few years but which is now trending higher:

Source: https://x.com/AndreasSteno/status/1780530738854584794

So for Inflation, it looks like we have more coming and likely towards the middle to end of the summer.

And if your wondering how high the commodity driven input to inflation can go, then here’s a scary chart of where things are starting for the commodities bulls:

Source: https://x.com/trend_bullish/status/1778920045545943050

Recession Watch:

On the Economic side it seems that everyone is waiting for the Unemployment shoe to drop and confirm that a Recession is here.

This hasn’t happened yet.

And this potential Unemployment spike is under heavy debate, and may or may not be delayed by a combination of immigration and a resurgent US manufacturing sector fueled by relatively cheap US energy production and the re-shoring of US production.

On the immigration side, and for your awareness, Fed Chair Powell is attentive to immigration’s impact on Unemployment.

Here’s Powell from his interview on ‘60 Minutes’ from February 4th, 2024 discussing the matter:

Source: https://www.cbsnews.com/news/full-transcript-fed-chair-jerome-powell-60-minutes-interview-economy/

But let’s consider the case for how Unemployment could spike in spite of immigration and supply chain re-shoring.

For starters, Multifamily Housing delinquencies have been rising:

Source: https://x.com/GameofTrades_/status/1783141344971812866

So with that and higher interest rates, Banks have tightened credit:

Source: https://twitter.com/MFHoz/status/1778863227880833057

New Chapter 11 Bankruptcies are on the rise:

Source: https://x.com/MichaelAArouet/status/1785182589092778254

And the Housing sector has starting to cool as Buying Conditions drop:

Source: https://x.com/GameofTrades_/status/1783163999439434169

Median Home Prices are still in free-fall:

Source: https://x.com/GameofTrades_/status/1774451607037497764

As a result, Housing Construction has starting to roll over but hasn’t started a meaningful decline yet:

Source: https://x.com/DonMiami3/status/1780223841400217993

The Year-over-year change in the growth of Full Time Employed has just turned negative:

Source: https://x.com/NorthmanTrader/status/1776254517815672871

With the NFIB ‘Poor Sales’ leading indicators pointing to rising Unemployment:

Source: https://x.com/FrancoisTrahan/status/1777697934445793626

And we’ve seen a dramatic separation between Part Time Employment and Full Time Employment that looks reminiscent of the beginning of the GFC:

Source: https://x.com/spomboy/status/1776235892425871469

That all said the double confirmations of a Recession have not hit yet.

Those confirmations being:

Rising Initial Unemployment Claims

Un-inverting yield curve

Source: https://x.com/GameofTrades_/status/1785648174511919353

So I guess we still have some time on this, assuming nothing breaks.

Federal Reserve Watch:

Luke Gromen (https://fftt-llc.com/), a financial commentator, and other commentators have pointed out that the Fed actually has a third mandate of ensuring a functioning Treasury Market.

This is common sense to me, but it bears mentioning at the moment because there are some ongoing issues with the US Treasury market.

Readers of my mid-month subscription note saw this great chart two weeks ago, showing a potential rotation away from US Treasuries to Gold starting in 2022.

Source: https://x.com/DTAPCAP/status/1777139680599027872

The coming wave of inflation has now added selling pressure to the gold buyer types.

And as that has happened the dollar has started to strengthen, first against the yen…

Source: https://x.com/LukeGromen/status/1783481960033091668

and more recently against other major currencies:

Source: https://www.marketwatch.com/investing/index/dxy

Now… no one wants a strong dollar for too long. And eventually if the Dollar and long bond yields continue to rise, then something in the market will break and things will become dysfunctional.

So either before or after that potential breakdown, the dollar needs to weaken.

That weakening probably comes through the US Fiscal side with Yellen putting USD into the market each day. but if something breaks then the Fed can intervene and fix whatever the issue is.

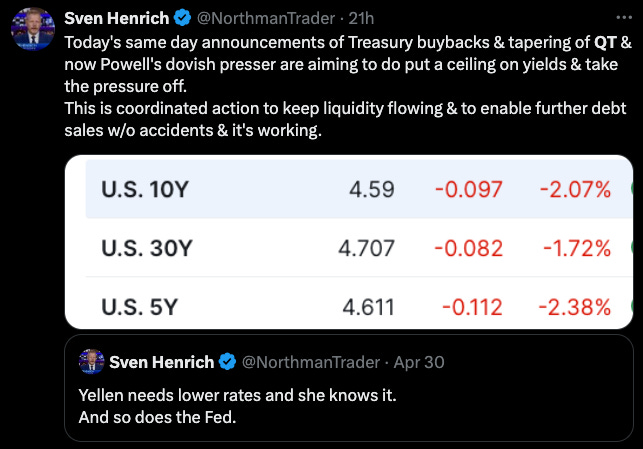

But with the Fed reducing tapering QT, my guess is that both the Fed and the Treasury understand the issue with long bond yields and is attempting to manage the situation.

Source: https://x.com/NorthmanTrader/status/1785745996351217686

In the longer term there are only a few ways out of all this.

Austerity is one way out, but everyone thinks that's unlikely. Maybe we check back in with the actuaries in a few years to see where Social Security payments are, but for the moment that’s not a discussion.

Some commentators like Russell Napier (https://russellnapier.co.uk/) see the potential for the Fed regulatory apparatus to incentivize Banks and Pensions to hold more Treasuries as a form of “financial repression”.

This could work temporarily as Banks and Pensions only have so much balance sheet, but we could start seeing this as a release valve if Treasuries continue to back up.

Others like Dr. Lacy Hunt (https://hoisington.com) note a small potential hope for a productivity miracle on the order of something like the advent of indoor plumbing, the rollout of electricity and the industrial revolution, or the building of the railroads in the mid 1800s.

The US has had a high number of these miracles relative to the rest of the world, but it seems like an Artificial Intelligence powered robotization and nuclear energy rollout is not ready for prime time just yet. Maybe after the bank and pension stuff.

Conclusion:

The Fed remains in a challenging position.

The potential for resurgent Inflation is set to arrive in the summer… though this risk is now recognized by markets.

Longer duration bonds are selling off in recognition of the inflation story.

Global Markets are rotating away from Treasuries to Gold, potentially due to Inflation, and potentially due to other geopolitical concerns.

As a result, the risk of a non-functioning Treasury Market is an immediate one and compounds the Commercial Real Estate issues noted in previous notes.

Paradoxically, the recognition of the inflation risk by the market now makes credit even tighter - causing large swaths of the broader economy to now reassess their refinancing options with lower hopes of a refinancing happening.

This increases the risk that something breaks somewhere, which would force the Fed’s hand to accommodate with additional liquidity sooner rather than later.

So all hands will be on deck soon to hopefully weaken the dollar in the near term before something breaks.

The potential for a Recession lurks on a medium time horizon, potentially coming after the election, perhaps in the 2025 time frame, so long as nothing breaks with Treasuries.

“Fiscal Dominance” is the buzzword of the day. And it means that Janet Yellen is more in control of Markets than Jay Powell is, and that seems to explain the various gyrations of different markets which seem inscrutable from a ‘Rates’ perspective:

Source: https://x.com/agnostoxxx/status/1778314510425583920

The “Maestro“ Alan Greenspan danced between the raindrops of the 90’s market, hiking here, cutting there … hike, cut … cut, hike.

Source: https://fred.stlouisfed.org/series/DFEDTAR

I don’t think Jay Powell wants to try to be this cute.

The Dollar is in a different place.

The Fiscal side is in a different place.

It’s easier for Powell to point at fiscal policy as key, stay apolitical, and only jump in if things become painful somewhere - forcing cuts, or if inflation gets really out of hand - forcing hikes.

But likely Powell hopes the Treasury plumbing will hold, and the USD will weaken from the Fiscal side until a Recession hits, which will clean up everyone’s financing, though perhaps with a bit shorter duration for the next go-round.

In my conclusion last month I said the following:

“As we’ve been saying for months now, the Fed is going to get itself stuck between the coming wave of re-flation, and a deteriorating Economy. And for the Fed, the easiest thing to do will be to emphasize the role of the Fiscal side of government and stand pat.

Three rate cuts this year? I’ll take the under.

There’s still a potential for the wheels to fall off the Commercial Real Estate Market and/or for regional banks to have a problem, but with the 2yr now going back higher on rates we seem mired in a yield curve that enjoys being inverted. And [t]he Recession won’t land until that Yield curve de-inverts.”

And all of that still seems correct to me.

If inflation becomes a bigger challenge over the summer, and a Recession starts some time after the election, then the short end of the curve is probably a better place to be than the long end.

The Fed needs to keep the Treasury Market functioning in the mean time, but a breakdown somewhere would be bullish for the short end.

Election Fiscal stimulus is on the near horizon.

Treasury market risk is a persistent issue, but the problem appears to be being addressed.

The Fed can incentivize/force/allow regulatory flexibility for Banks and Pensions to hold higher levels of Treasuries if other countries continue to unload their Treasuries.

Which allows the Fed to remain apolitical, while the Treasury does the lifting.

The next few summer months could go in a few different directions, but a weaker Dollar lets us all muddle through somewhere between Stagflation and rising risk assets.

Until next month.

Please subscribe if you haven’t already and consider our Pro Tier if you would like direct on-demand access to my entertaining views on the Economy.

Great insights!