Monthly Market Compass: September 2025

Trump fires shots at the Fed. AI vs. the Consumer remains the debate. Bitcoin and Equities at a crossroads, but no catalyst yet for derailment. What about Gold and Commodities?

Hello again, and welcome to our Monthly Market Compass for September 2025. We send these chart heavy market summaries at the beginning of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: an introduction and inflation watch, an economy section, a Fed focused section, and a geopolitics and commodities section. A market conclusion follows these sections. Enjoy!

Introduction and Inflation Watch:

Welcome back to another month!

Another month goes by, and another month of waiting for a catalyst that could reverse the equities market. The debate rages about which market analogue is correct, 1998 or 2008. Do we have another few years of upward momentum, or will we see a dramatic selloff?

The US continues to show a bifurcated market with the AI and tech story battling with the weakening of the US Economy.

The AI Economy continues to steam ahead despite some selling of Nvida surrounding their recent earnings call. The AI economic narrative as a whole has been strong, but now looks like it might be weakening. Meanwhile, the non-AI economy continues to deteriorate.

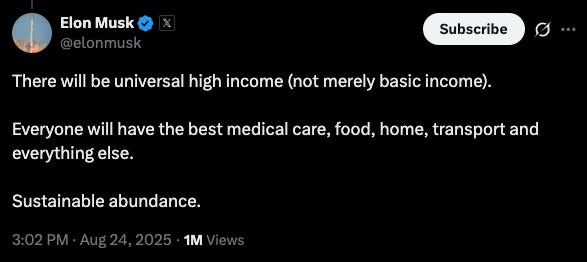

The AI world is so heady at this point (this time is clearly different) that Universal Basic Income (UBI) is being talked about as a potential reality as Elon Musk and others anticipate a productivity spiral through AI productivity gains.

Source: https://x.com/elonmusk/status/1959723029531181380

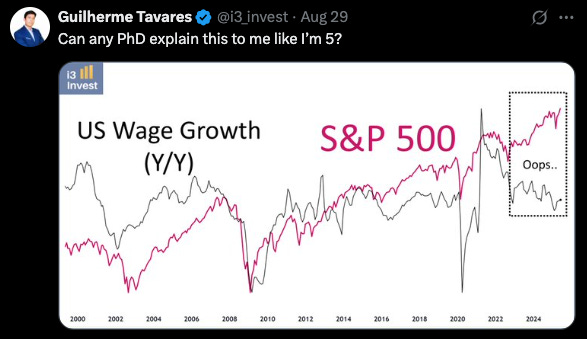

For the moment, however, it appears that the AI to wage growth relationship has moved in the opposite direction:

Source: https://x.com/i3_invest/status/1961519222636622232

By contrast, the non-AI economy continues to worsen, with various indicators of unemployment starting to rise. Official unemployment figures have had a circus of revisions from early 2024 through to present which show a much weaker job market than originally expected, but with recent official unemployment figures at moderate levels, the Fed has been sluggish to cut rates.

The Trump administration also believes the Fed is being sluggish and is doing everything in its power to fire unprecedented warning shots at the Fed. This includes verbal criticism of the Fed Chair, attempting to remove one Fed Governor for cause, and signaling that Trump would hire a dovish Fed chair after Jay Powell's term expires in May 2026.

All of these actions look like ways to have the market look through the current set of Fed actions to an eventual dovish Fed which would likely cut rates more dramatically, in line with Trump’s ambitions for the Fed Funds rate.

Although recent Fed statements at Jackson Hole were interpreted as more dovish on rates, for Trump and others, this pivot is likely seen as too little and too late.

The Fed—as always—is attempting to remain apolitical in all of this, but this political tension between the Fed and the Trump administration remains a fixture of the current global macro environment."

Last year, we outlined our comparison of the US in Trump's second term to both President Reagan's first term and Prime Minister Milei's election in Argentina in late 2023, noting that leaders in these similar positions showed a correlation between local currency direction and the inverse performance of their associated stock markets.

For the US now, this implies that we’ll see a strong USD coupled with a weak US Equities market, or a weakening USD and an increase in US Equities.

All indications point to Trump wanting a weaker dollar to bolster US equities, which explains his actions towards the Fed. What remains to be seen is how much Fiscal spending he will support with infrastructure spending and support for the US consumer.

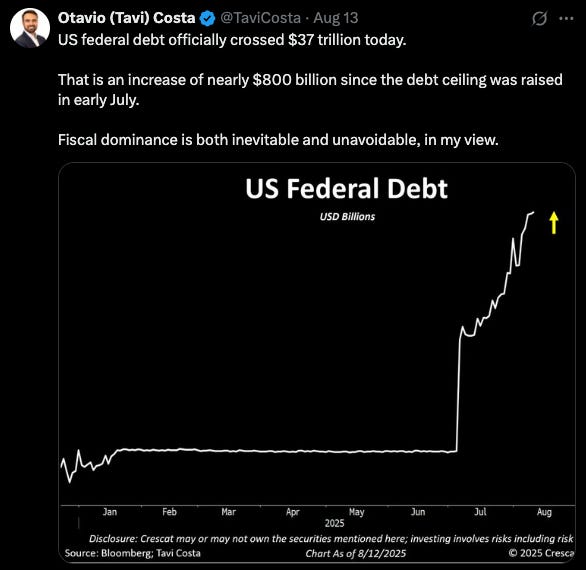

The US and Global debt remain high:

Source: https://x.com/TaviCosta/status/1955654519825879178

This leads to long-term concerns that at some point the US, along with the rest of the western world, will not be able to pay its bills and en masse will start to print money in order to pay its interest expense.

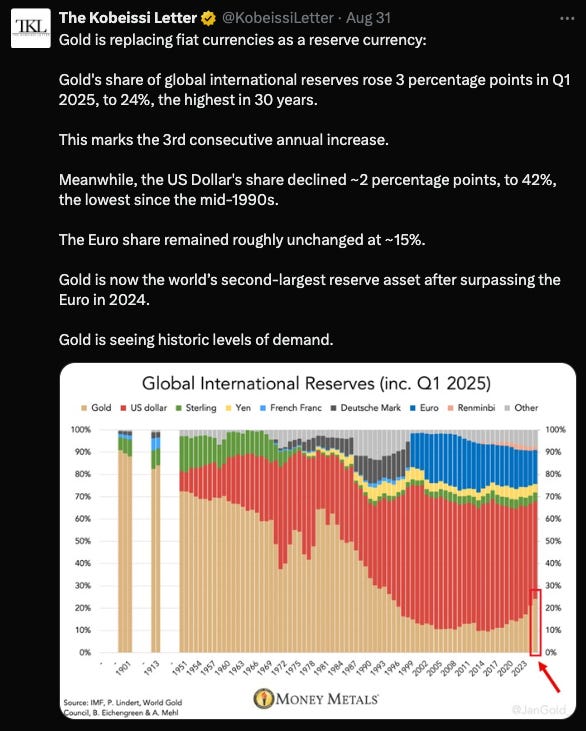

Related to this, central banks continue to buy gold, rotating away from US Treasuries, despite the sideways price action in the yellow metal.

Source: https://x.com/KobeissiLetter/status/1962235795622035767

Some unverified sources on the internet are also claiming that central banks are underreporting the total amount of gold they are buying.

In doing so foreign central banks now hold more gold than US Treasuries, and don’t seem ready to stop this ongoing rotation.

Source: https://x.com/TaviCosta/status/1960908250980999436

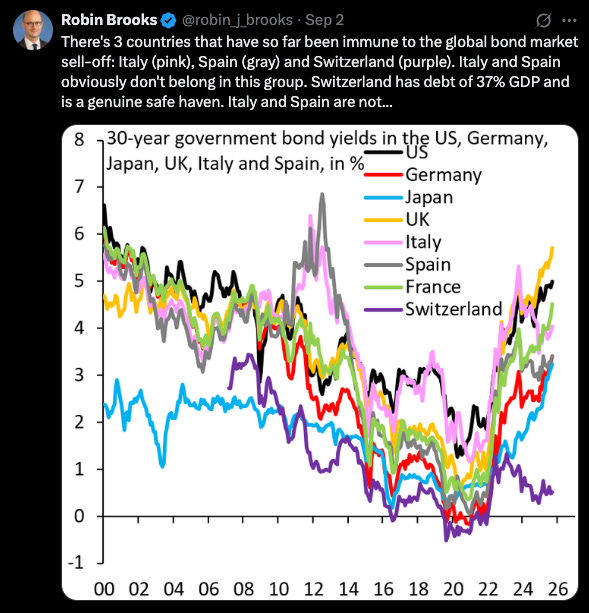

And long-term bonds are paying the price now, with the additional concern of the debt and printing cycle that seems to be coming at some point:

Source: https://x.com/robin_j_brooks/status/1962857075395969082

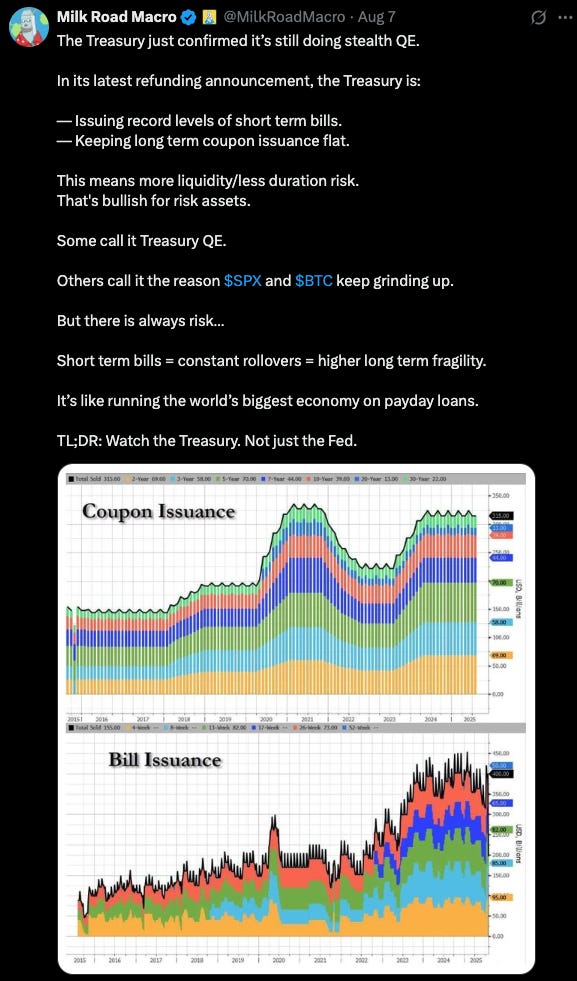

Wisely the US Treasury is funding the US government through short end issuance:

Source: https://x.com/MilkRoadMacro/status/1953501447959842905

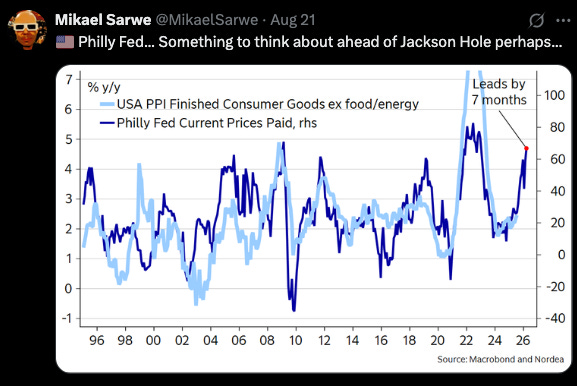

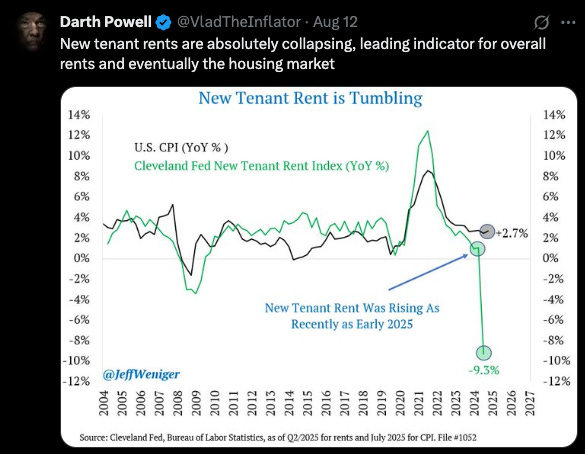

The short-term inflation outlook looks like a mixed bag.

By some measures, Inflation is set to continue to rise in coming months:

Source: https://x.com/MikaelSarwe/status/1958530404970869177

By others, inflation is set to fall:

Source: https://x.com/VladTheInflator/status/1955272697249689730

The Truflation number for inflation moved dramatically up to 2.31% this past month before falling back to 2.02%:

Source: https://truflation.com/marketplace/us-inflation-rate

In previous months we've pointed to a divided view on short-term US inflation, with CPI being dramatically different from this Truflation figure.

I suspect this change is due to increase energy costs from the AI boom, but am not certain on this.

Longer-term inflation concerns swarm around the continued debt of the US government, the resulting challenges of rolling over short-term debt at higher rates, and the associated increasing interest expense burden.

Eventually, without a solution, short-term inflation debate will merge with the reality of long-term inflation expectations, and this sharp upswing in Truflation may seem in hindsight as a shot across the bow of what is coming at some point in the next few years.

When that happens the dollar will likely weaken dramatically. Given the large moving pieces surrounding US fiscal spending, government debt, interest expense, and tax receipts have all yet to change, all roads still lead to that eventual weaker dollar.

US Treasury Secretary Scott Bessent is optimistic about the amount that President Trump’s ongoing tariffs might generate for the US. On August 26, 2025, he stated that annual customs duty revenues could reach "well over $500 billion" and might approach $1 trillion as collections continue to rise. Source

The US annual deficit stands at approximately $1.63 trillion, so a trillion in revenue would reduce but not zero-out the annual deficit. Source

Add to this the new legal challenges to President Trump’s tariffs, which are already headed to the US Supreme Court. Without a reversal by the Supreme Court, an earlier ruling from a US appeals court that most of Trump's tariffs are illegal will go into effect in mid-October. Source

But the question remains whether we will see some type of equity market selloff, or US Treasury market dysfunction before then that changes the timeline. It also remains to be seen how aggressive the Federal Reserve and US Treasury would be in those two scenarios.

For the moment, the fear is that inflation will move higher towards a repeat of the 1970s: