Monthly Market Compass: October 2025

Trump looks to cut spending amidst the ongoing US Government shutdown. US Equities face a moment of truth, while crypto and alt-coins look for the reattachment to the global M2 indicator.

Hello again, and welcome to our Monthly Market Compass for October 2025. We send these chart heavy market summaries at the beginning of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: an introduction and inflation watch, an economy section, a liquidity section, a Fed focused section, a geopolitics and commodities section, this month we are adding a crypto section, which is followed by an Equities section. A market conclusion follows these sections. Enjoy!

Introduction and Inflation Watch:

Welcome back to another month!

Just a quick reminder that if you are not signed up for our $10 a month subscription, you will not be able to read this entire article. If you enjoy these blogs, please help by supporting this Substack and subscribing for only $10 a month, or for $100 a year.

We write this note amidst the ongoing government shutdown after failed U.S. Government funding discussions.

The U.S. government shutdown began at midnight on October 1, 2025, due to Congress failing to pass a funding bill that would finance federal government operations for the new fiscal year.

The main cause of the shutdown is the political deadlock over federal spending levels, health insurance subsidies, and proposed cuts and rescissions to foreign aid.

President Trump and Republicans seek to maintain specific budget priorities and policy provisions, while Democrats demand the continuation of existing healthcare subsidies and oposed cuts to welfare and health-related programs.

President Trump has signaled he will use the shutdown to cut various programs:

“Republicans must use this opportunity of a Democrat forced closure to clear out dead wood, waste, and fraud. Billions of Dollars can be saved.”

Source: https://www.newsweek.com/donald-trump-vows-to-use-shutdown-to-clear-out-dead-wood-10815476

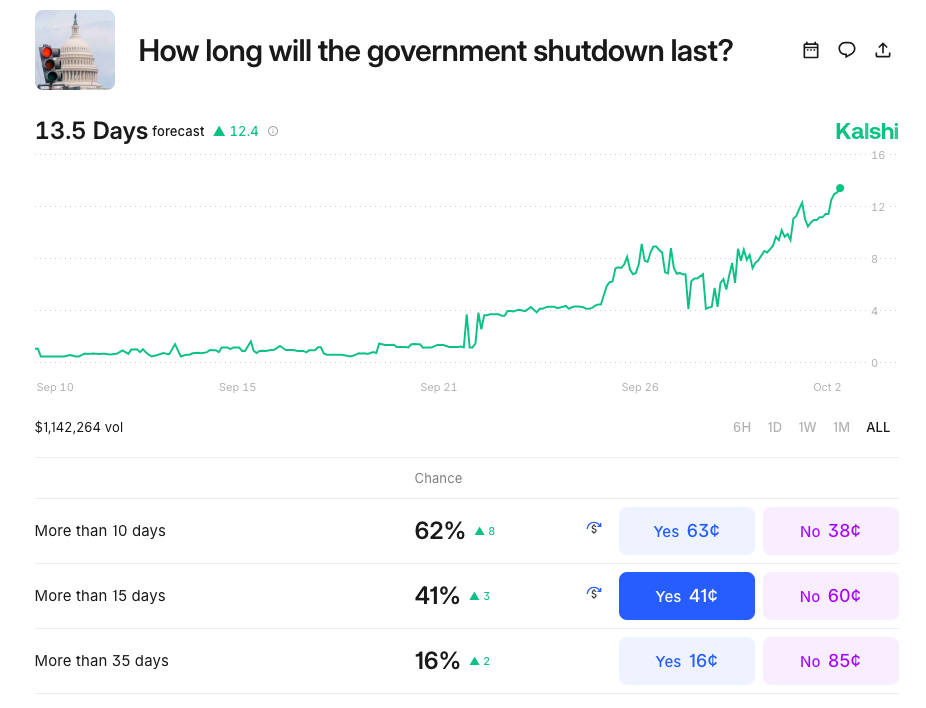

We don’t know how long this will go on, so investors should be wary of the potential for a protracted delay in the funding of the government.

However, in previous years, these delays have resolved themselves relatively quickly. This time, prediction markets are expecting a delay of around two weeks.

Source: https://kalshi.com/markets/kxgovshutlength/days-of-government-shutdown

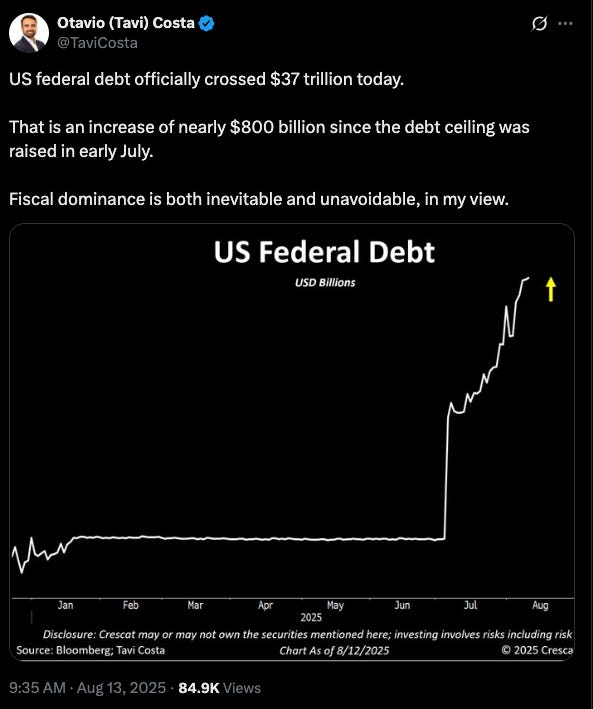

That said, the key challenge for the US remains the federal debt and the cost of running the government.

Source: https://x.com/TaviCosta/status/1955654519825879178

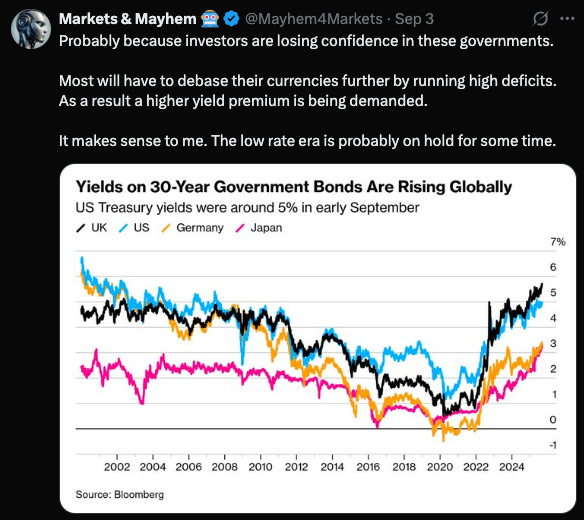

As we’ve written about before, most of the long bonds in the developed world are being sold off. This includes the US:

Source: https://x.com/Mayhem4Markets/status/1965076453181280267

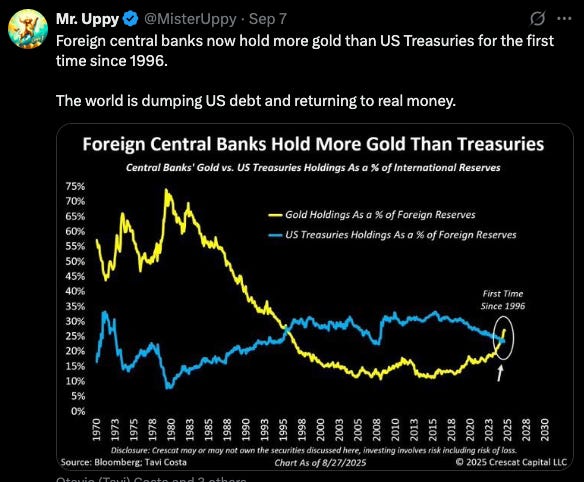

Central banks and others are rotating out of U.S. Treasuries and into gold:

Source: https://x.com/MisterUppy/status/1964718175209275667

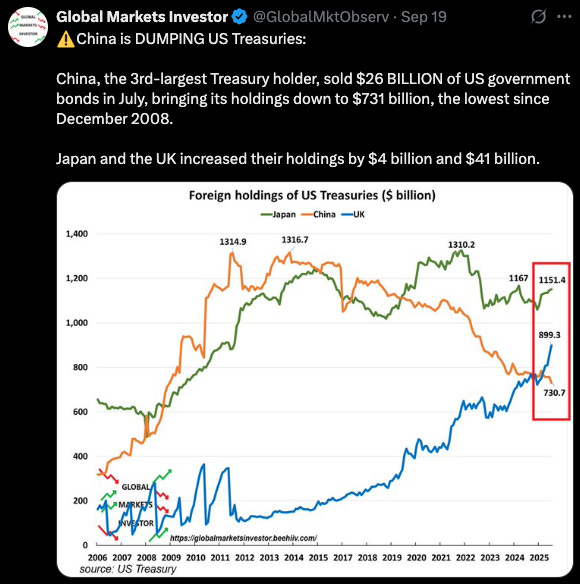

China specifically is dumping USTs, while Japan and the UK make up most of the difference:

Source: https://x.com/GlobalMktObserv/status/1969031233477685423

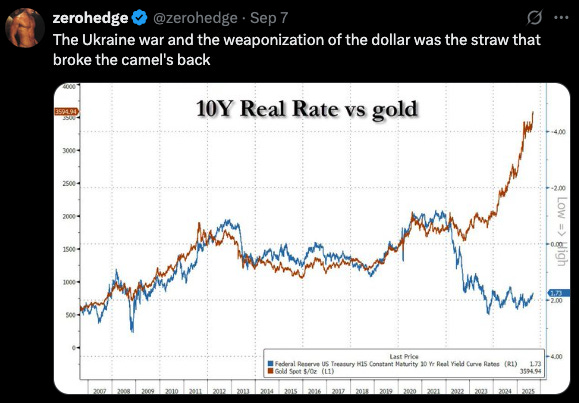

The 10yr UST vs gold rotation that we’ve shown many times in our writing is now is being understood as the result of USD weaponization towards Russia:

Source: https://x.com/zerohedge/status/1964813380839211312

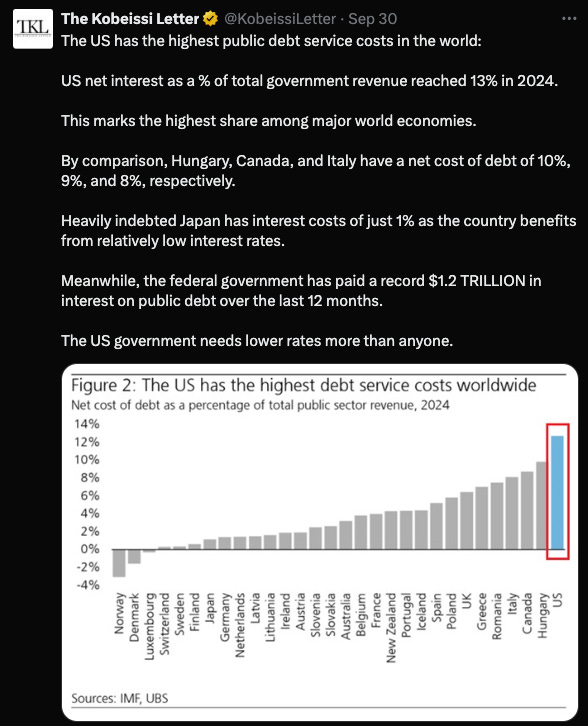

The net effect is that the U.S. interest expense has become the highest in the advanced world:

Source: https://x.com/KobeissiLetter/status/1973039883922116673

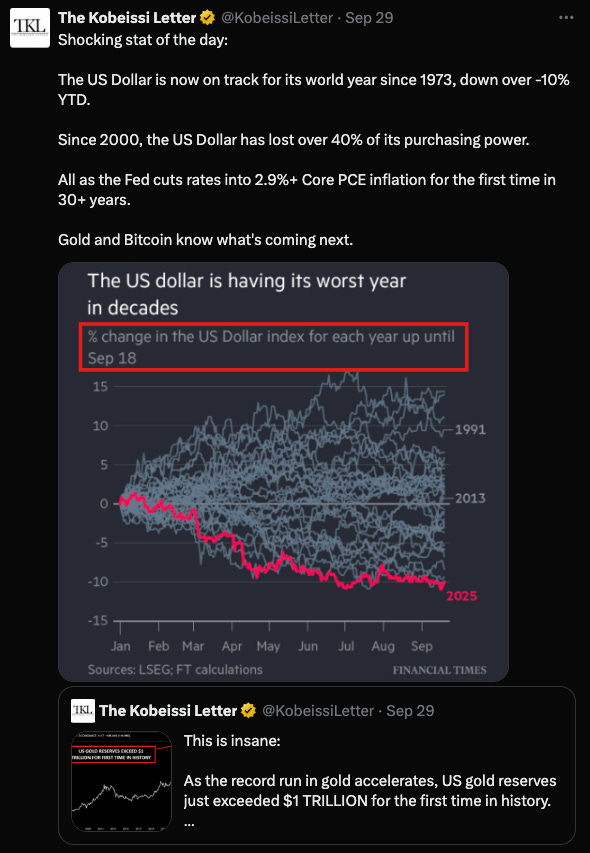

More dollars are likely to be printed to pay the U.S. debt down, and as you might expect, the U.S. dollar has been declining now for most of the last year:

Source: https://www.marketwatch.com/investing/index/dxy

Indeed, the USD is having its worst year since 1973:

Source: https://x.com/KobeissiLetter/status/1972747205271241119

The USD is now looking to break (down) against a resistance of its 14 year rising channel trendline:

Source: https://x.com/Barchart/status/1968061273469489222

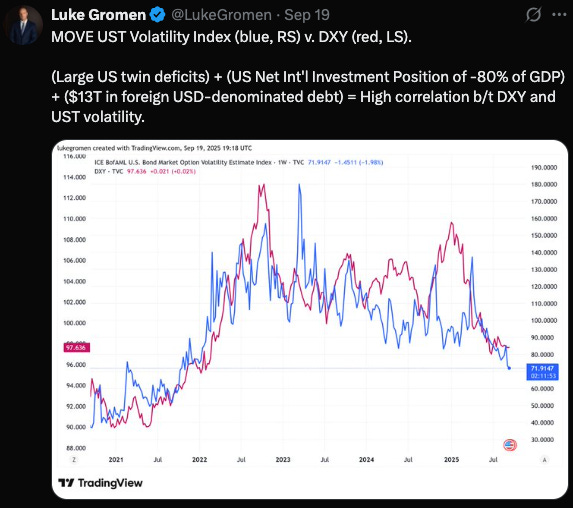

A correlation between the DXY (USD) and the U.S. Treasury MOVE volatility index is pointing towards that happening:

Source: https://x.com/LukeGromen/status/1969119997193568707

For many market observers, the Fed is likely 100bps to 150bps behind where they should be in rate cuts despite the recent rate cut this past month.

In the meantime, the Trump administration continues to make moves (signaling a looser Fed chair for next May, trying to find more favorable Fed governors for an upcoming renewal cycle, and of course, tariffs) in hopes that they can soften the blow from seemingly high rates from the Fed

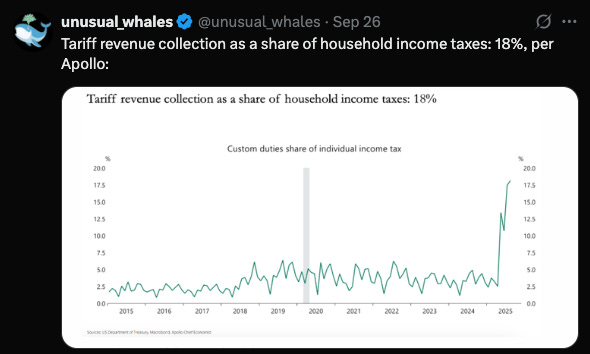

Tariffs specifically are starting to move much higher in revenue, but it remains to be seen if these will be meaningful for funding the U.S. Government, or if they will be too little too late.

Source: https://x.com/unusual_whales/status/1971549563979739275

Turning to inflation:

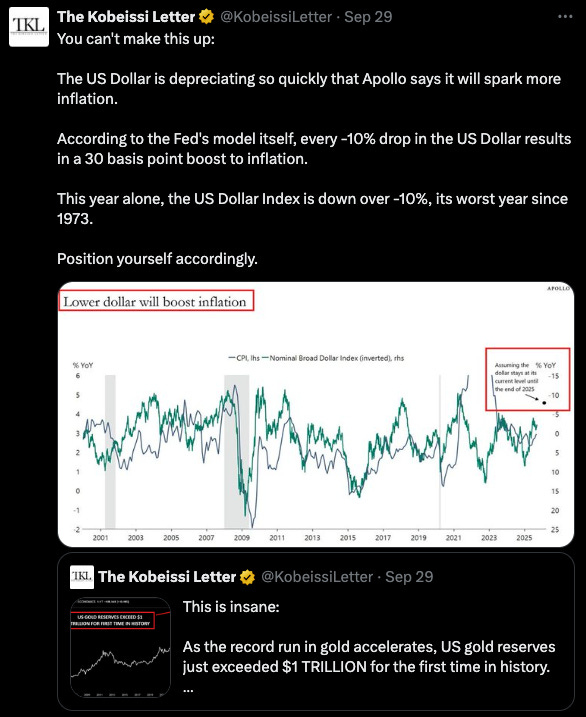

A weaker dollar eventually produces more inflation:

Source: https://x.com/KobeissiLetter/status/1972729840832024752

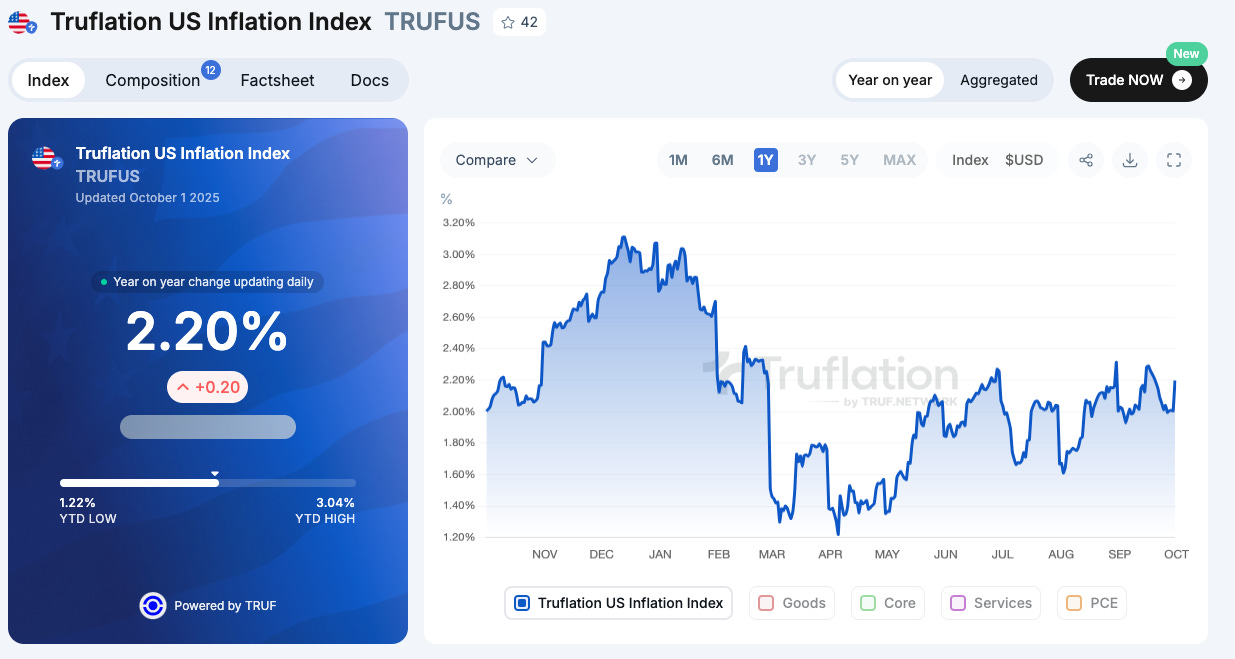

Specifically, the Truflation metric that we follow continues to move between 2% and the 2.5% range, but could be trending higher:

Source: https://truflation.com/marketplace/us-inflation-rate

But future inflation numbers look harder to predict.

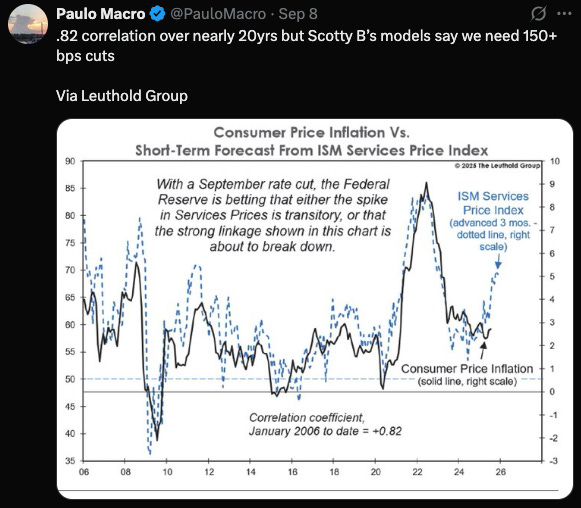

Here, Consumer Price Inflation could soon be in the five handle:

Source: https://x.com/PauloMacro/status/1965228780055908809

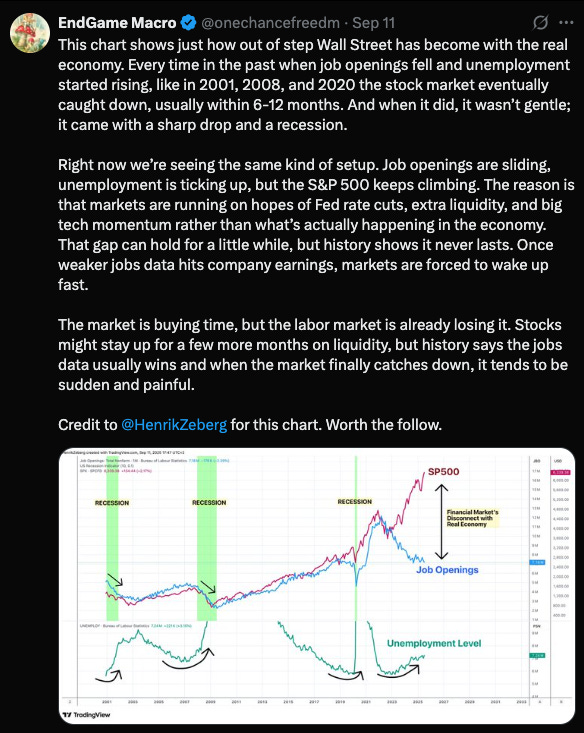

The question remains from the AI story: how high can the S&P 500 go without a workforce?:

Source: https://x.com/onechancefreedm/status/1966259658970247584