Monthly Market Compass: February 2026

Software in a Selloff! Gold and Silver epically gyrating! USD breaks its 14-year trend in the DXY. And Kevin Warsh likely to be the next Fed Chair, but US rates haven't yet exploded.

Hello again, and welcome to our Monthly Market Compass for February 2026. We send these chart-heavy market summaries at the beginning of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: an introduction and inflation section, an economy section, a liquidity section, a Fed-focused section, a geopolitics and commodities section, a crypto section, which is followed by an equities section. A market conclusion follows these sections. Enjoy!

Introduction and Inflation:

Welcome back to another month!

Just a quick reminder that if you are not signed up for our $10-a-month subscription, you will not be able to read this entire article. If you enjoy these blogs, please help by supporting this Substack and subscribing for only $10 a month or $100 a year.

What an interesting month for Macro investors! I’ve heard many say that this is the golden age of macro investing, and I couldn’t agree more. “May you live in interesting times”, indeed!

Gold and silver prices skyrocketed to record highs in late January 2026, with silver surging nearly fourfold before a brutal 30% single-day crash last week, the worst since 1980.

This all comes amidst the longer-term trends we’ve been outlining for months.

Japan has joined the rest of the modern world with higher bond yields:

Gold vs. US dollar assets continues to be the backdrop of the US Treasury market:

And on that front, Gold continues to climb against US Treasuries in central bank vaults:

We’ve shown in past months that the USD via the DXY remained above a 14-year trendline of upward momentum.

That trend is now broken, as the DXY is now below where the 14-year trend would put it for early February of 2026, roughly 98.43 vs. the current DXY level of 97.39.

This points towards further coming dollar weakness, and likely higher prices for various asset classes that have not yet seen dramatic price moves.

Multiple global currencies look like they could be strengthening against the Dollar, which reinforces this idea:

For reference, here is the 35-year view of the US’s ‘cleanest-dirty-shirt’ against gold:

Bitcoin weakened dramatically along with the gyrations in Silver and Gold, dropping more than 22% and marking its largest drawdown since 2022. However, Bitcoin is correlating more closely with the ongoing selloff in software equities:

But tension is rising when we look at Inflation. US CPI is up around 1.24%, while the Truflation number is nearly a half point lower around 0.86%:

In a traditional sense of monetary policy, the Fed is well behind where it ‘should’ be in terms of cutting rates, but this discrepancy between CPI and where inflation likely is, will give some latitude to Jay Powell over the coming months before his upcoming exit.

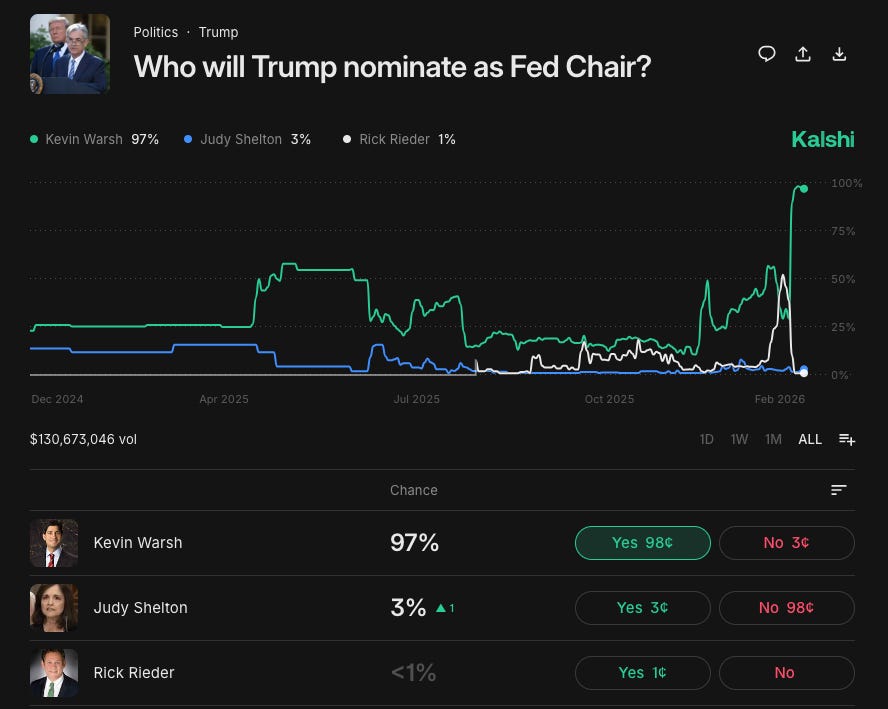

Powell is slated to leave the Fed Chair seat in May, with Kevin Warsh as the current clear frontrunner to take the Fed Chair seat:

Source: https://kalshi.com/markets/kxfedchairnom/fed-chair-nominee/kxfedchairnom-29

If Kevin Warsh secures the Federal Reserve Chair position, he would become the second former Druckenmiller protégé in the Trump administration, joining Treasury Secretary Scott Bessent.

Scott Bessent and Kevin Warsh did not overlap in their professional tenures under Stanley Druckenmiller, but the implied coordination points to Druckenmiller’s potential influence on U.S. fiscal and monetary policy through his protégés now holding both pivotal roles in the Trump administration.

Druckenmiller is famously attentive to US fiscal spending and the concerns around the US’s twin deficits.

Here’s Druckenmiller’s ‘The Endgame’ presentation from the 2016 Sohn Investment Conference: https://covestreetcapital.com/wp-content/uploads/2016/07/The-Endgame-Presentation.pdf

It is very notable that when Warsh became the front runner for the Fed Chair seat, long-term US Treasuries did not sell off dramatically.

Most market viewers point to Warsh’s reputation as an inflation hawk during his tenure as a Federal Reserve governor from 2006 to 2011, where he (in line with Druckenmiller’s views on fiscal spending) consistently expressed concerns about rising inflation risks even amid economic downturns like the 2008 financial crisis, advocated for tighter monetary policy, and often warned against overly accommodative measures such as prolonged QE.