Monthly Market Compass: December 2025

The government shutdown is over. Google's Gemini looks like a real threat to OpenAI. The market is expecting a December rate cut by the Fed. Gold looks like it is moving higher, but where is Bitcoin?

Hello again, and welcome to our Monthly Market Compass for December 2025. We send these chart heavy market summaries at the beginning of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: an introduction and inflation section, an economy section, a liquidity section, a Fed-focused section, a geopolitics and commodities section, a crypto section, which is followed by an equities section. A market conclusion follows these sections. Enjoy!

Introduction and Inflation:

Welcome back to another month!

Just a quick reminder that if you are not signed up for our $10-a-month subscription, you will not be able to read this entire article. If you enjoy these blogs, please help by supporting this Substack and subscribing for only $10 a month or $100 a year.

This past month saw a number of interesting developments, so let’s dive right in.

In the important AI-tech world, Google released its Gemini 3.0 model across all its platforms on November 17 this past month. The model eclipsed OpenAI’s GPT-4 Turbo on reasoning and multimodal tasks. And in response, OpenAI CEO Sam Altman declared an internal “code red,” pausing ads and non-core projects to focus on ChatGPT after reports of losing 6% of daily users.

Google paired the release with “The Thinking Game,” a 90-minute feature-length documentary chronicling Demis Hassabis and Google’s DeepMind team’s pursuit of artificial general intelligence. The film highlights pivotal breakthroughs like AlphaGo’s victory in Go and AlphaFold’s Nobel Prize-winning solution to the 50-year-old protein-folding problem.”

This all marks a potential turning point in the AI race.

Google represents the only “full-stack” AI company, meaning it controls custom silicon, in-house model development, unified developer tools, and billions-user distribution surfaces like Search and Workspace, all combining to enable seamless user experiences and built-in financing mechanisms.”

Source: https://x.com/AndreasSteno/status/1993636070945071389

Interestingly, the US government has started to take action that leans in favor of the AI tech story.

On November 24, 2025, President Trump announced The Genesis Mission, a national effort to accelerate AI-driven scientific discovery by building an integrated federal AI platform that combines the country’s 17 national laboratories, massive computing resources, and federal scientific datasets. The initiative will train AI foundation layer models and create AI agents for automated research across priority domains like nuclear fusion, quantum information science, biotechnology, and semiconductors. Source: https://x.com/AskPerplexity/status/1993096098823491845

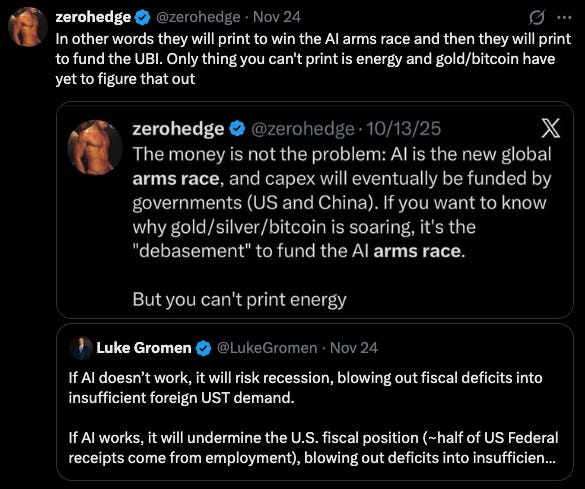

Whether or not the AI boom ends up creating a productivity growth boom of the type that is hoped for remains to be seen, but commentators are starting to expect the same results regardless of how the AI story pans out: money printing and QE.

Source: https://x.com/zerohedge/status/1993132203254112307

Despite this potential future money printing, the US Dollar currently remains relatively strong.

The US government shutdown is over after chalking up a whopping 43 days of government inaction—from October 1 to November 12.

Since November 12, the US Dollar has moved higher from 99.50 in the DXY to 100.23 before round-tripping back to 98.85 at the time of writing this note.

Source: https://www.marketwatch.com/investing/index/dxy

Readers of last month’s note will recall that I was worried about the US Dollar’s strength over the last month.

We showed this chart last month and noted that the DXY (USD) index found support on its 14-year trendline:

Source: https://x.com/Barchart/status/1975339316990947819

We’ve been expecting the USD to weaken, and its resilience above this trendline has been a confounding factor for some of our long-term debasement ideas.

If we project this trendline out to December 3, we get a number around 98.39, which is very close to where the DXY sits at the time of writing this note (98.85).

So once again we look like the market is on the precipice of confirming or rejecting a major macro breakpoint.

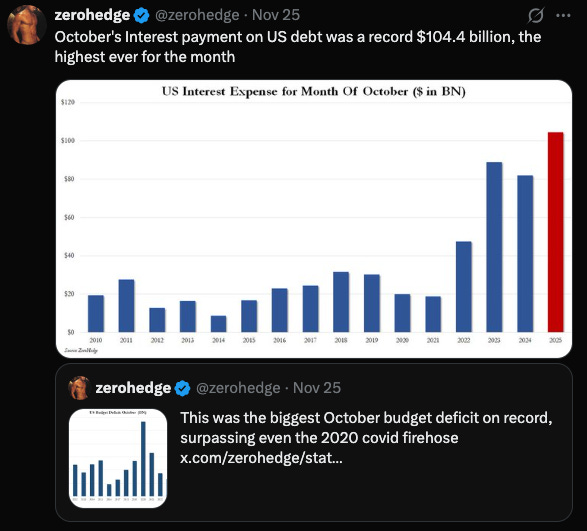

The US Interest expense continues to rise as more Treasuries get refinanced at higher yields:

Source: https://x.com/cooltechtipz/status/1993316848071590200

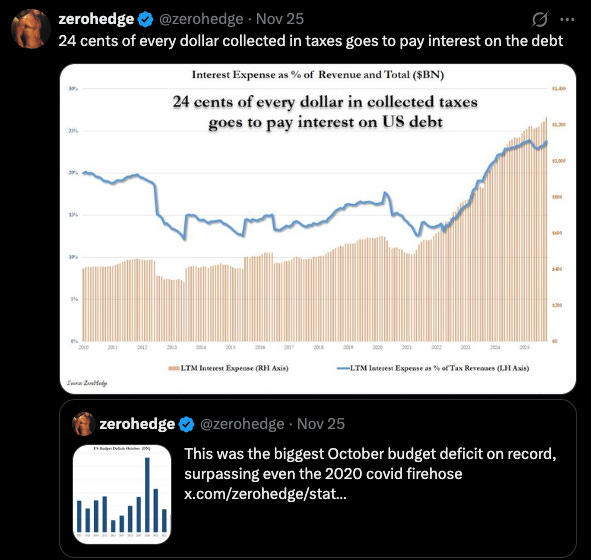

Currently 24 cents of every dollar collected in taxes go to pay this interest rate expense:

Source: https://x.com/zerohedge/status/1993526341665542237

We’ve been noting for months that this increasing amount of US tax receipts to pay down interest rate expenses likely doesn’t end well.

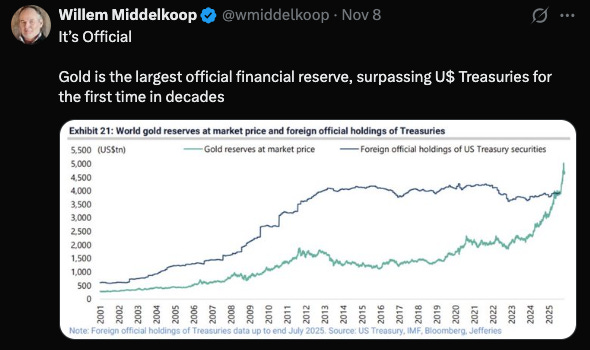

Gold has officially shot past US Treasuries as reserve assets globally:

Source: https://x.com/wmiddelkoop/status/1987233548433051893

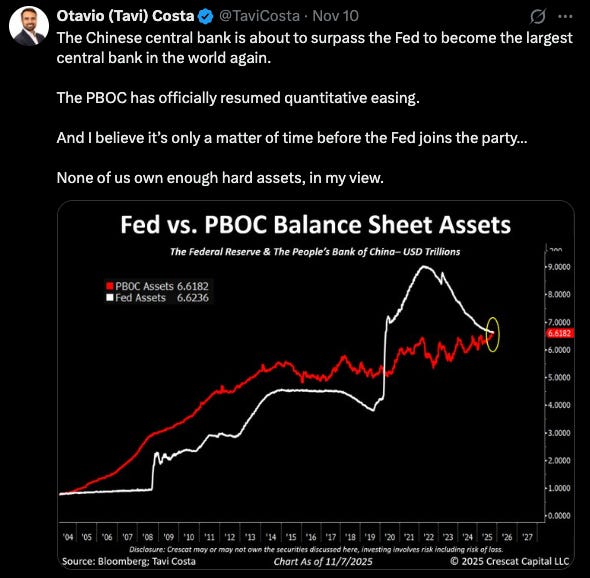

Relatedly, we’ve shown that China has been acquiring large positions in gold over the past months, and with these purchases and the gains in gold, the PBOC balance sheet assets have now eclipsed again the balance sheet assets of the US Federal Reserve:

Source: https://x.com/TaviCosta/status/1987902545097085317

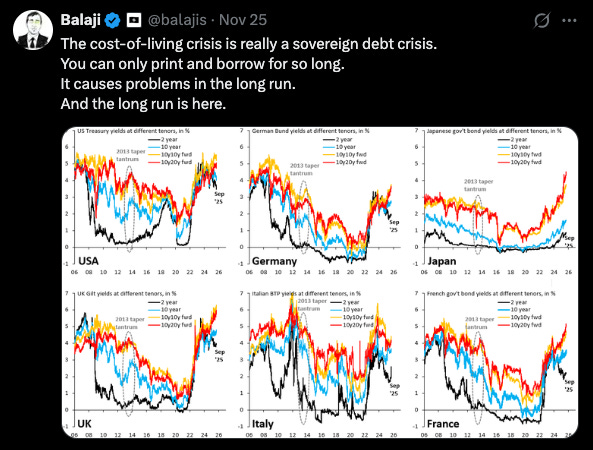

Globally, bonds have continued to back up in yields as most developed nations encounter similar challenges in long term rates to what the US has recently faced.

Source: https://x.com/balajis/status/1993555279838093324

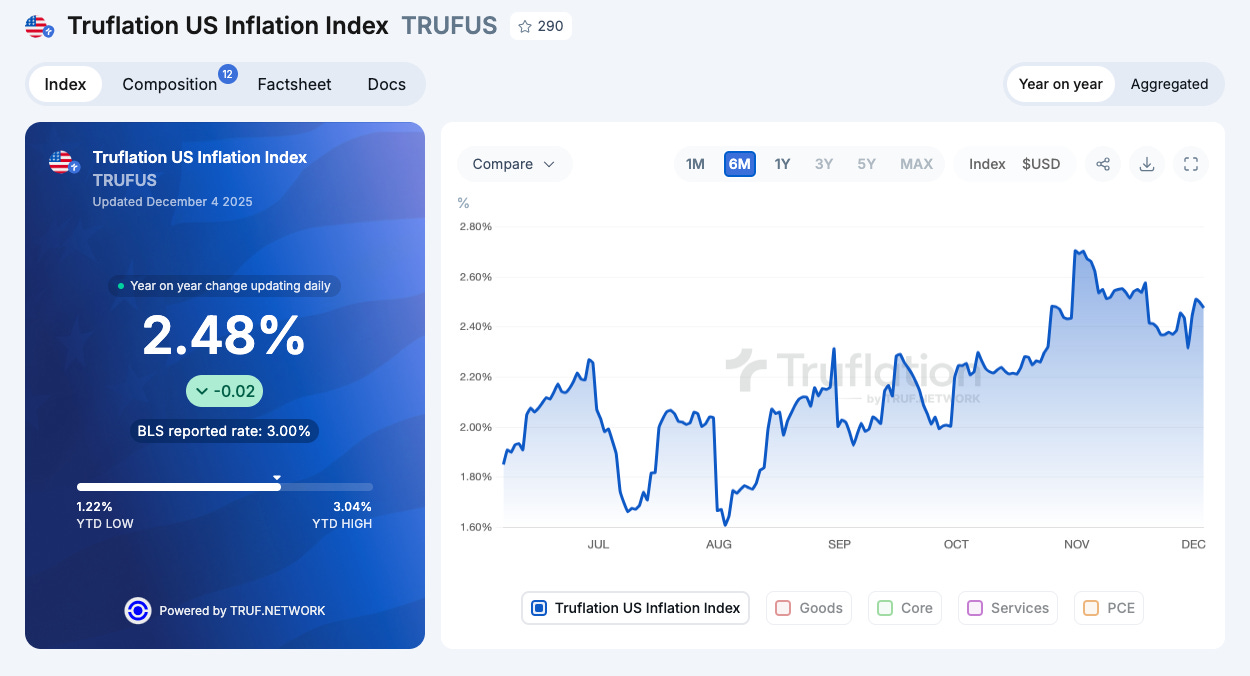

Truflation points to an upwardly sloping inflation rate over the last few months:

Source: https://truflation.com/marketplace/us-inflation-rate

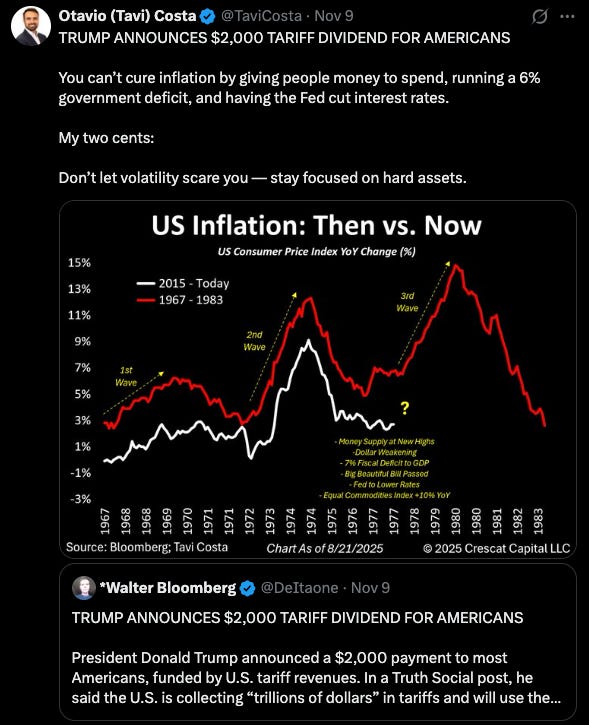

The challenge, to show a graph we’ve shown before, is that the US is about to repeat a surge in inflation over the coming few years: