How to Think About Universal Basic Income (UBI) in the Age of AI

UBI critics argue it risks hyperinflation, so why does Elon Musk think we'll have "Universal HIGH Income (not merely basic income)"? Can AI deflate prices faster than UBI inflates them?

The Musk Paradox

In late August 2025, amidst the ongoing breakneck rollout of new AI models and tools, Elon Musk wrote a tweet response on Twitter/X about Universal Basic Income (UBI), where he indicated that we will have “…universal high income (not merely basic income).”

Source: https://x.com/elonmusk/status/1959723029531181380

UBI has long been seen as a risky extension of welfare that risked any country bold enough to try it experiencing a potential inflation spiral scenario where payments exceeded government tax receipts, causing a fiscal mismatch of funds that would lead to a debt crisis.

Musk, whose level-headed focus on fiscal spending mere months ago with his lead role in the Department of Government Efficiency (DOGE) project, made him an unlikely candidate to forecast a more muscular form of UBI for the entire population.

So what about this new AI world has Musk thinking along high level UBI lines?

Existing UBI Programs

Energy-rich regions such as Saudi Arabia, or Alaska offer programs that provide some amount of monthly income, but often those programs are below what a Western household needs to survive in modern times.

Alaska has a Permanent Fund Dividend: $1,000 (annual as of 2025 - down from prior years)

Iran has a Universal Cash Transfer: Originally $30/month per person

Macau (China) has a Wealth Partaking Scheme: $750–1,250 annually

Brazil has the Bolsa Família/Auxílio Brasil: Variable by family size since 2003, but averaging around $120 per family per month

Saudi Arabia has a Citizen Account Program: $395/household/month

These all felt like gestures at having residents of the area take part in the wealth that was being created out of (often) natural resource extraction taking place in the region, but came at the expense of organic domestic growth.

Economic history is littered with the ideas of the Dutch Disease/Resource Curse/Paradox of Plenty dynamic, where resource-rich countries experience slower growth, weaker institutions, and worse development outcomes than resource-poor countries due to the resource-rich country’s lack of organic economic development, as resource extraction often funneled through foreign-owned companies to the local government, bypassing local residents.

UBI Pilot Programs

Three major pilots offer concrete evidence: Finland (2017–2018) found no employment boost but significant mental health gains. Stockton, California (2019–2021) saw recipients more likely to find full-time work, with most spending on essentials. Kenya’s GiveDirectly program (2017–present), the largest test, showed reduced hunger, increased entrepreneurship, and durability against economic shocks—with no dependency effects.

US Government Expansion?

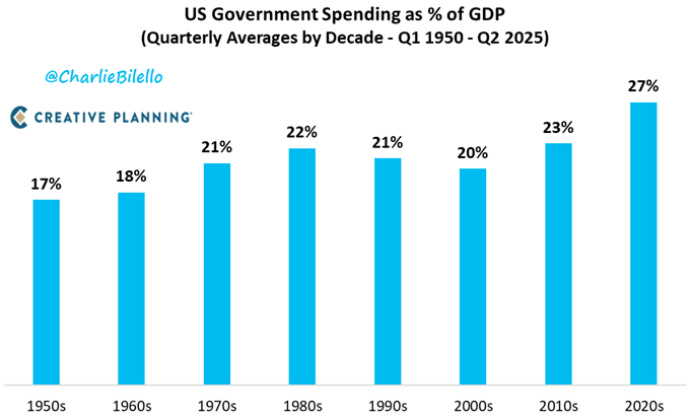

Separately, the share of the US GDP that is directly related to US government spending has been increasing over the last few decades.

Source: https://x.com/charliebilello/status/1966249768335606185

If that number theoretically were to increase to 100%, then that result would rhyme with the idea of government-provided UBI.

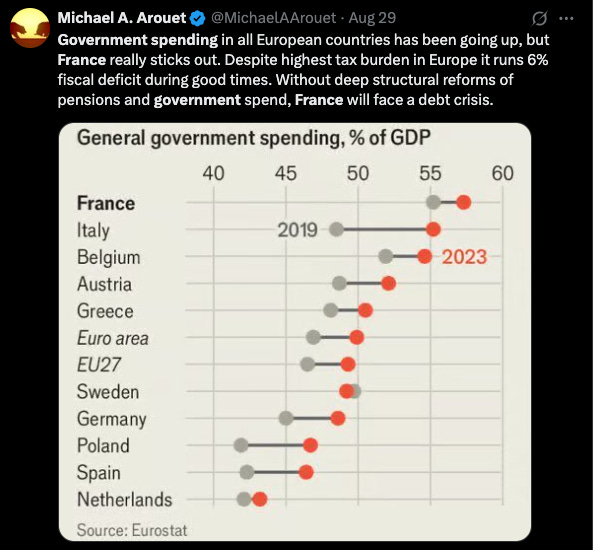

Multiple European countries seem like they are already moving in this direction, with France leading the way:

Source: https://x.com/MichaelAArouet/status/1961660469296439677

A Conservative Breaks Ranks

In 2016, the conservative writer Charles Murray, broke ranks with his fellow US-based conservatives with a UBI plan that he detailed in his book “In Our Hands.”

In it, he proposed giving every American citizen aged 21 and older $13,000 annually ($3,000 mandatory for health insurance, $10,000 discretionary cash), with payments phasing out above $30,000 income at a 30-cent reduction per additional dollar earned.

He argued that his plan would have completely eliminated the entire welfare state—Social Security, Medicare, Medicaid, food stamps, housing assistance, unemployment insurance, and all other transfer programs—and funded the UBI through the redirection of existing welfare spending, which Murray claimed would actually save $200 billion annually.

Murray’s conservative-libertarian rationale was that this would end involuntary poverty in the US while eliminating bureaucratic inefficiency, reducing dependency, and revitalizing civil society institutions like family and community. However, critics argued the $10,000 discretionary amount would be inadequate for basic living costs, and particularly harmful to families with children and disabled individuals who would lose specialized support programs worth far more than the flat UBI payment.

MMT Accounting Shell Games

In the late 2010s, Modern Monetary Theory suggested governments that issue their own currency are constrained by inflation, not revenue.

Per Wikipedia, MMT’s core tenants are:

…that a government that issues its own [fiat money]:

Creates money with any and all government spending

Effectively destroys money via taxation

Cannot be forced to default on debt denominated in its own currency

Is limited politically in its money creation only by demand-pull inflation, which accelerates once the real resources (labour, capital and natural resources) of the economy are utilised at full employment

Should strengthen automatic stabilisers to control demand-pull inflation, rather than relying upon discretionary tax changes

Has the option to issue bonds as a monetary policy device or savings device for the private sector. Bonds cannot act as a means of funding public spending. The government can set whatever price for bonds it decides.

Uses taxation to provide the fiscal space to spend without causing inflation and also to drive demand for the currency.

Source: https://en.wikipedia.org/wiki/Fiat_money)

For the fiscally savvy, this was just reframing: inflation and bond markets still serve as the ultimate check on spending, and taxation still backstops everything.

But MMT raises a useful question: what if deflationary forces in the economy are bigger than government money printing? This shifts the entire UBI debate. If massive productivity gains could deflate prices faster than UBI inflates them, traditional constraints disappear. History suggests this isn’t theoretical—we’ve seen it before.

Growth Miracles

In contrast to the Resource Curse mentioned above, various economic students of history have written about the idea of Growth Miracles that dot the history of economic development in the world.

Many of these Miracles originated in the US or the West more broadly, and are hallmarked by the innovations they represented: steam engines, indoor plumbing, electricity, the Internet.

These innovations drive productivity gains throughout the economy by unlocking new technological use cases for the economy: electricity lighting offices during evening hours, railroads shipping goods long distances in substantially lower timeframes.

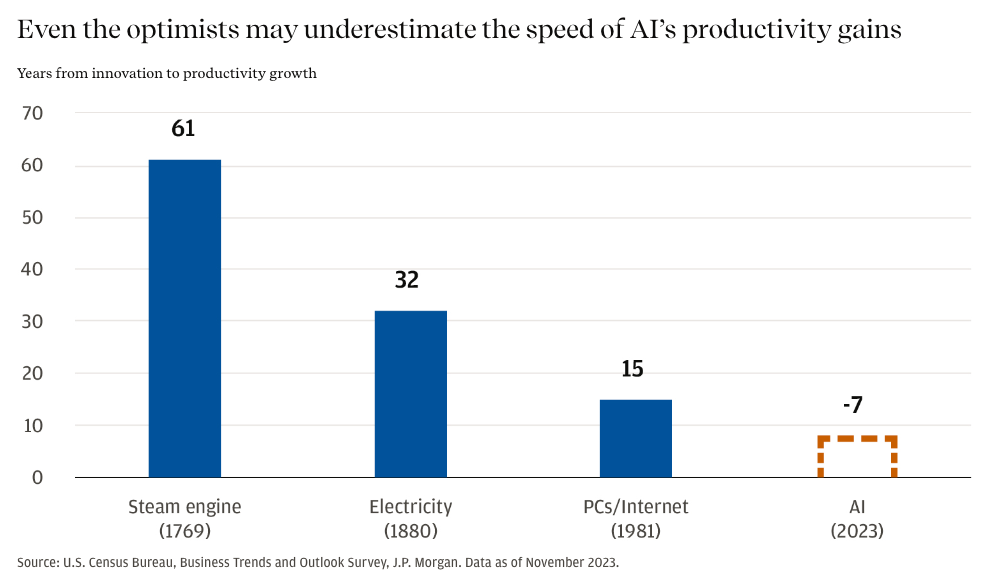

A recent report by the JPMorgan Private Bank, showed that the time between innovation and productivity gains were shortening for major innovations.

Often these Miracles take advantage of Jevons Paradox, which occurs when technological advancements make a resource more efficient to use. Here too the question arrises: is there a natural limit, an S curve of productivity which will plateau at some point, or will productivity from AI cause a cascading number of other technologies and associated productivity gains that cause a dependable trend like Moore’s Law for productivity?

Lastly, Growth Miracles also are characterized by employing vast numbers of people who build the railroads, or install the new technology, leading to gains in both productivity and labor.

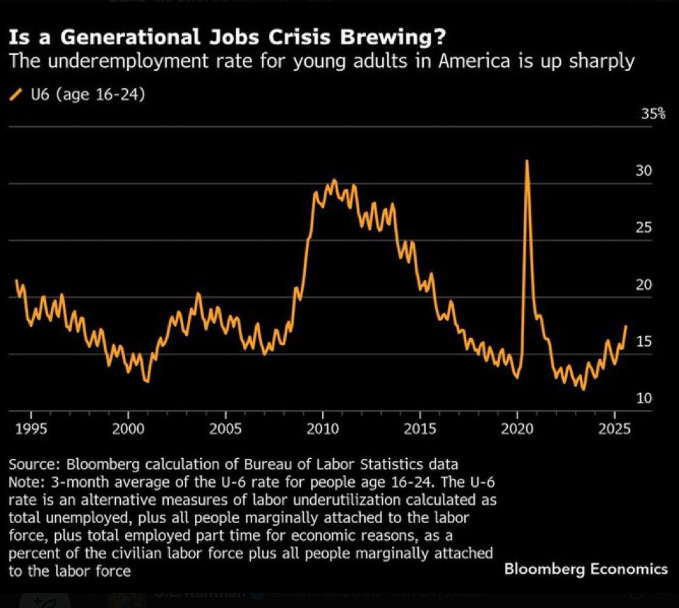

And what if AI doesn’t create jobs?

So far the AI story has been a mixed bag for employment, with many seeing a link between deteriorating job prospects for new graduates due to displacement effects from AI.

Source: https://x.com/AFpost/status/1954944855529881758

As of October 2025, emerging trends underscore the urgency of AI’s impact on employment, with Microsoft having cut over 15,000 jobs this year amid heavy AI investments, framing the layoffs as a push for remaining staff to adapt to artificial intelligence or risk obsolescence. Similarly, Anthropic’s CEO Dario Amodei has forecasted that AI could eliminate up to half of entry-level white-collar roles within five years, potentially driving unemployment rates to 10-20%. These developments align with JPMorgan’s analysis of shortening innovation-to-productivity lags in AI, suggesting disruption today but possible long-term growth—yet they highlight why UBI discussions are intensifying as a buffer against widespread job displacement.

Microsoft Source: https://www.cnbc.com/2025/07/24/microsoft-satya-nadella-memo-layoffs.html

Anthropic Source: https://www.axios.com/2025/05/28/ai-jobs-white-collar-unemployment-anthropic

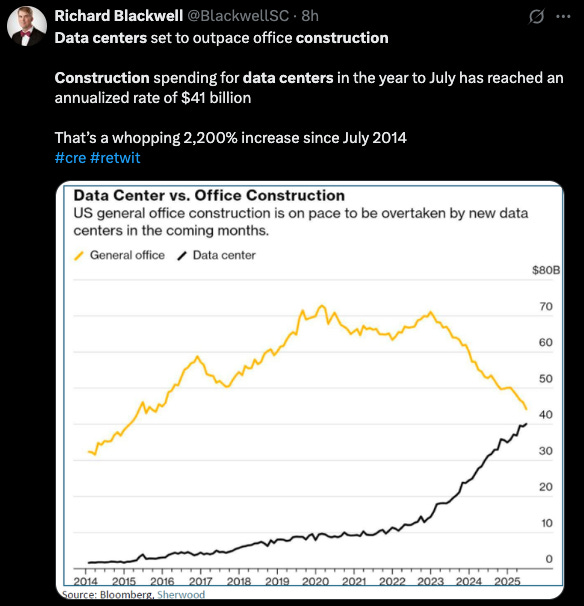

AI-focused data center construction will soon eclipse commercial building construction, which could provide some buoying effect to unemployment, but many wonder how long this trend will last, and by extension how accurate are the projections for data needs by the AI/technology companies.

Source: https://x.com/BlackwellSC/status/1976621987276509208

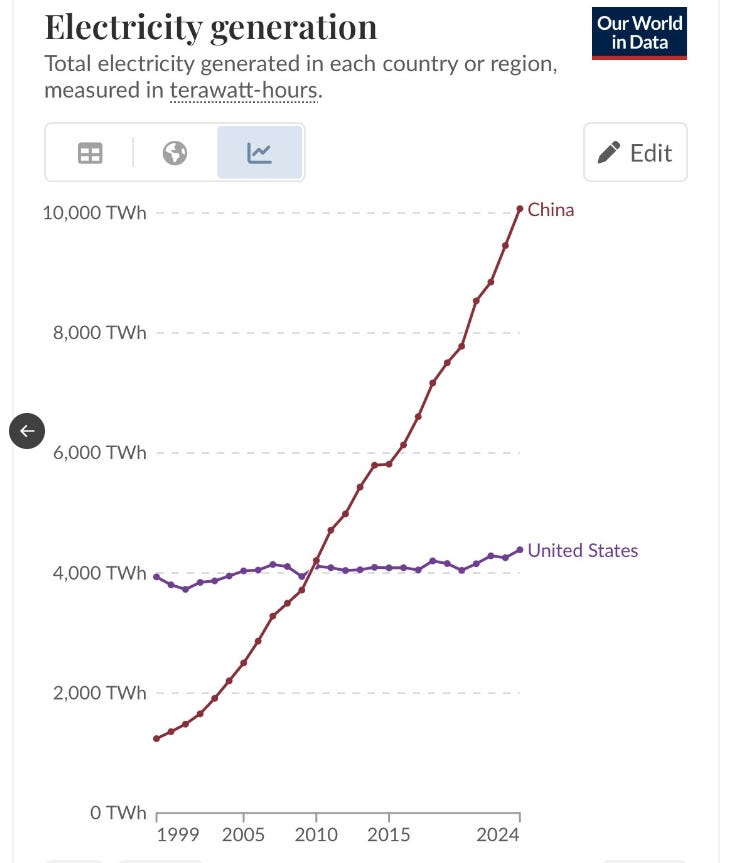

Along with the need for data centers, comes the related need for energy production. China is vastly in front of the US in terms of its energy creation.

Source: https://x.com/LegitTargets/status/1942644855265714497

Which leaves many in the US wondering if Nuclear power or a combination of green energy alternatives might make up the difference.

Labor vs. store of wealth

The crypto crowd would have us believe that Bitcoin and other deflationary crypto instruments offer an escape ramp. If the U.S. dollar is likely to fall in value, and jobs become scarce, then isn’t the alternative to simply hold Bitcoin and other cryptos as an off-ramp, bypassing the need for labor entirely?

The argument has surface appeal: if AI-driven deflation in goods and services coincides with fiat currency debasement through UBI spending, a fixed-supply asset could preserve purchasing power without requiring employment.

But the argument sidesteps the question of accessibility: how does a society provide a similar function for children, newborns, and the non-crypto-savvy? Would government set up a small crypto account at birth for citizens alongside their existing Social Security account?

The crypto solution, while appealing to some, doesn’t scale to a societal safety net. Which brings us back to the central question: what happens if AI eliminates jobs faster than it creates them?

UBI as a last resort

But if the labor side of the AI story fails to materialize, the last resort for supporting citizens is likely to be a UBI.

This seems to be where Musk has landed.

The potentials that could occur in this future would therefore have the following features:

AI produces enormous productivity gains

That productivity rapidly deflates prices across the economy

Much of the workforce is displaced

UBI is needed for many people who are no longer employed

A UBI with lower aggregate inflationary pressure than the deflationary pressures produced from AI would result in a UBI that is experienced as non-inflationary, as prices deflate faster than the money produced from UBI.

Ideas from Science fiction

Science fiction has been chewing on the idea of UBI for a number of decades. These fictional futures offer pattern recognition for policy design in ways economic models cannot.

Star Trek famously invokes replication technology that makes all but the largest construction requirements trivial in cost. But a quick review by an LLM points out many different sci-fi worlds with other UBI programs, some set in space, and some based on Earth, and many unrelated to AI.

For analogues to our current world, I reviewed sci-fi systems that are near-future, Earth-based, UBI systems specifically based around AI-produced productivity gains.

From that subset of sci-fi UBI programs, I reviewed Marshall Brain’s Manna: Two Visions of Humanity’s Future, Pantheon (Animated Series), and Matthew Binder’s The Absolved, which distilled into two themes: first, the potential for societal divide as ownership of AI-related assets becomes critical; and second, the importance of where the taxation that funds UBI is targeted relative to the human society.

Given that the likely reader of this post will be focused on themselves and their family, and unable to directly influence new taxes and taxable entities, the best advice for a scenario of increasing AI productivity gains seems to be a focus on owning productive, AI-related assets that will hold value into the future.

Conclusion: A Framework for Thinking About AI-Era UBI

When evaluating Universal Basic Income in the age of AI, three critical questions should guide your thinking:

1. What’s the feedback loop?

MMT’s critics were right to focus on inflation constraints, but in a deflationary AI scenario, the question inverts: How does inflationary UBI not expand beyond the deflationary trend of AI? What is the feedback loop? Does the bond market still play that role via government-issued debt?

The science fiction examples consistently show that UBI systems fail when they create dependency without maintaining human agency and purpose. The design challenge isn’t just financial then—it’s psychological and social.

2. Is the net effect inflationary or deflationary?

If inflation is the ultimate feedback mechanism constraining government spending, then the math changes entirely in an AI-driven deflationary environment. Traditional UBI concerns revolve around inflation, but what if AI productivity gains deflate prices faster than UBI inflates them? Then the UBI dynamics change. In an AI scenario where goods become radically cheaper (think electricity costs after the steam engine, or computation costs after Moore’s Law), a UBI of $2,000/month might have the purchasing power equivalent to $5,000 today. The critical variable isn’t the nominal payment amount—it’s whether aggregate demand from UBI exceeds or lags behind productivity-driven price collapse.

This is why Musk’s “universal high income” claim only works if deflationary forces dominate; otherwise, we’re back to traditional inflation constraints and more modest payment levels.

3. Is the goal to control or to enable?

The historical lesson from both Growth Miracles and Resource Curses is that who owns the productive assets determines where wealth accrues. In an AI economy, this means the distribution of compute resources, energy production, and AI model ownership will matter more than the UBI payment amount itself. Sci-fi UBI analogs (entertainingly) point to the risk of UBI being used as a control apparatus, and this dynamic, unfortunately, should lead as a risk in any evaluation of a new UBI program.

The Conservative and Radical Path Forward

Paradoxically, Charles Murray’s conservative instinct may point toward the radical solution: simplify before expanding. If AI productivity gains are real, the case for consolidating existing welfare bureaucracy into direct payments strengthens. But the transfer amount, taxation source, and asset ownership patterns will determine whether that creates Musk’s “high income” future or a divided society of asset-owners and dependents.

The key takeaway is that the proponents of AI are so bullish on AI’s deflationary effects on the economy, that a UBI of size might be achievable from taxing the remaining productive elements of the economy, so long as the inflationary pressures from UBI don’t overwhelm the deflationary impacts of the AI boom.

Until next time.