How to Think About Stablecoins

From the GENIUS Act, to Web3, to DeFi, to AI Agents, to Eurodollars, and the need to find buyers for U.S. Treasuries - learn how Stablecoins are about to take center stage in global finance and tech

How to Think About Stablecoins

In 2020, CD Projekt Red—the creator of the Witcher game series—released Cyberpunk 2077, which introduced players worldwide to a currency called “eddies”—shorthand for Eurodollars—that had replaced, in-game the once-mighty U.S. Dollar as the primary medium of exchange for that game’s Night City residents.

Transactions were quick, digital, and seamless, and underscored the advancement of technology in a world that had seen nation states lose power as corporations rose to even higher prominence.

Mike Pondsmith, the original developer of the Cyberpunk Red tabletop RPG, had envisioned a world where the United States had fractured and could no longer guarantee traditional U.S. Dollars, which resulted in the traditional USD greenback being replaced by the non-U.S. domiciled dollars, eddies, backed in the game by the by a consortium of banks (with heavy European involvement), which offered stability amid global chaos.

What seemed like pure science fiction in 1988—or even fantastical gaming lore in 2020—suddenly feels remarkably prescient as we witness the real-world emergence of stablecoins as an addition to the already complex global monetary system.

From speedy digital transactions, to a funding mechanism for the U.S. Treasury, to the potential preferred medium for the growing AI Agent world, here’s how to think of stablecoins as they enter the global U.S. Dollar system.

Stablecoins - what are they, and why do they exist:

In the aftermath of Bitcoin, and Ethereum rising from obscurity in the early 2010s to being considered by some as a new digital form of asset class, one of the use cases that most people could agree on was the value in the relatively quick resolution of transactions occurring on those networks.

Wire transfers that took a full business day or longer to clear, and T+2 trading transactions were put on notice by the new crypto currencies that offered a transaction settlement in minutes, and counter-parties that would unlock funds after only an hour or less after a crypto transfer had resolved.

Technologists took note. Why not optimize a crypto network for the use case of speed. How quickly could a system resolve a transaction if it was solely focused on this quickness.

The idea would be that some form of cryptocurrency could be designed to hold a steady value, usually pegged 1:1 to something that people would want to move quickly.

Many ideas were considered. Early ideas pegged a stablecoin to Bitcoin, which might be able to transfer more quickly than Bitcoin itself. Things like ‘wrapped’ Bitcoin, which are Ethereum-based tokens that represent a Bitcoin, are a version of this idea. PAXG is a gold-backed Ethereum token with a similar idea (though the distinction of ‘wrapped’ vs. ‘backed’ has a specific technical meaning in the crypto world).

Source: https://coinmarketcap.com/currencies/pax-gold/

At this point many other ‘wrapped’ and ‘backed’ offers are active in the crypto world.

Stablecoins Take the Stage:

The best use case for a backed cryptocurrency token emerged over time as a USD backed asset.

Tether (USDT) launched quietly in 2014, operating primarily through a claimed reserve of U.S. Dollars. Tether weathered significant scrutiny and established the template for stablecoins, but the opacity of Tether’s system and questions around its 1 to 1 peg against USD held assets forced it to operate primarily outside of U.S. jurisdictions.

In 2018, the U.S.-based Circle’s USD Coin (USDC) emerged as the transparent alternative to Tether, through its commitment to backing tokens with dollars held in verified financial institutions, and undergoing regular Deloitte-backed audits—becoming the stablecoin of choice for major U.S.-based exchanges like Coinbase.

As of October 2025, Tether’s market cap is approximately $176 billion, while USDC’s is around $74 billion.

Stablecoins at this point have become the indispensable backbone of decentralized finance (DeFi), with applications spanning every corner of the DeFi ecosystem. They serve as trading pairs on exchanges, collateral for lending platforms like Aave and Compound, liquidity providers in yield-generating protocols, and base assets for complex financial instruments and derivatives.

However, the road to this point was not smooth.

In May 2022, the sector’s most dramatic stress test came when a stablecoin called Terra (UST), which was an algorithmic stablecoin, collapsed spectacularly, triggering crypto market-wide panic that briefly pushed even Tether’s price down to 94.85 cents per USDT before it successfully restored its dollar peg shortly thereafter.

The issue for Terra was that it had backed its token with a collection crypto-backed assets. This meant that when the price of Bitcoin and other cryptos started to fall dramatically from November 2021 to mid 2022, the backing assets of Terra were insufficient to meet the dollar equivalents of what Terra had issued in USD terms. In essence this was a run on the Terra ‘bank’.

This watershed moment reinforced the dominance of fiat-backed stablecoins over their algorithmic cousins and highlighted the critical importance of traditional reserve backing. The Terra debacle became a defining moment that separated legitimate players from experimental projects, ultimately strengthening confidence in properly collateralized stablecoins like USDT and USDC, but paving the way for recent measures by the U.S. Congress with the GENIUS Act to more clearly define the requirements of stablecoins that wanted to play in U.S.-based markets.

Enter the GENIUS Act:

The Global Economic Navigation and Innovation for U.S. Stablecoins Act (GENIUS Act) of 2025, is a recently passed U.S. law signed in July 2025 that sets up rules for stablecoins, and represents the U.S. government’s first big step to regulate this part of the crypto world.

The law establishes a federal framework for **payment stablecoins**—non-interest-bearing, USD-backed digital tokens mainly used for payments and transfers.

Issuers: Only “permitted payment stablecoin issuers” (PPSIs)—federally supervised non-banks, qualified state-licensed firms, or banks under existing rules—can issue.

Reserves & Safety: Every stablecoin must be backed 1:1 with safe assets (cash or short-term Treasuries). Issuers need capital buffers, liquidity, and risk management (cybersecurity, fraud prevention, wind-down plans).

Transparency: Regular audits, disclosures, and restrictions on misleading marketing are required.

Custody: Reserves must be held by regulated custodians, keeping user assets separate from issuer operations.

Consumer & National Protections: Safeguards users against losses and scams, strengthens the dollar’s global role, and prevents misuse for illicit finance.

AI Agents at the Gates:

The key features of stablecoins remain their speed and versatility. Stablecoins, being digitally native, can be used for transactions that are code-based and this makes them ideal for new technologies that are emerging now and being considered within the financial world, and by new technology startups.

Google, for example, has unveiled a comprehensive payment infrastructure for AI agents centered around two groundbreaking initiatives: the Agent Payments Protocol (AP2) and the Google Cloud Universal Ledger (GCUL). These developments position stablecoins as the primary currency for autonomous AI transactions, with the potential to fundamentally reshape digital commerce.

AP2 operates through a sophisticated “mandate” system that ensures transaction security and user control. The protocol employs three types of digitally signed credentials.

Intent Mandate: Captures the user’s initial shopping request, such as “buy me running shoes under $120”. This creates an auditable record of user authorization and establishes the scope of the agent’s authority.

Cart Mandate: Provides final approval for specific purchases, creating an unchangeable record of exact items and prices. This prevents agents from making unauthorized modifications to transactions.

Payment Mandate: Offers ecosystem visibility to payment networks and includes additional risk assessment information.

The crucial component of AP2 is the x402 extension, developed in partnership with Coinbase and the Ethereum Foundation. This extension activates the long-dormant HTTP 402 “Payment Required” status code, enabling instant stablecoin payments directly through standard web protocols.

The x402 protocol allows AI agents to:

Complete transactions in under two seconds with fees as low as $0.001

Process payments using USDC and other stablecoins on low-fee Layer 2 networks like Base

Operate without complex wallet infrastructure or manual authentication

Execute micropayments for API access, content, and services

Complementing AP2, Google is developing the Google Cloud Universal Ledger (GCUL), a permissioned Layer-1 blockchain specifically designed for financial institutions. GCUL represents Google’s most direct entry into banking infrastructure, offering native commercial bank money on-chain rather than digital representations.

GCUL distinguishes itself through several innovative approaches:

Python-based smart contracts: Unlike most blockchains that use Solidity or Rust, GCUL employs Python, making it accessible to existing finance and data science teams.

Neutral infrastructure: Positioned as “credibly neutral” infrastructure that doesn’t favor specific tokens or vendors, addressing concerns about ecosystem lock-in.

Native bank money: Supports tokenized commercial bank deposits backed by regulated assets like money market funds, providing an alternative to traditional stablecoins

Compliance-first design: Built with integrated KYC checks, audit trails, and regulatory safeguards for institutional requirements.

CME Group, one of the world’s largest derivatives exchanges, has partnered with Google to pilot GCUL for tokenization and wholesale payments. The first phase of integration completed in March 2025, with broader testing scheduled for late 2025 and commercial deployment targeted for 2026.

The convergence of AP2 and GCUL positions stablecoins as the preferred medium for AI agent transactions. Industry leaders predict that AI agents will become “the biggest user of stablecoins” as autonomous systems require programmable, borderless, and instantly settleable digital currencies.

Web3 on the Horizon:

Further out in the future, stablecoins are positioned to become foundational infrastructure that could fundamentally reshape Web3’s and DeFi’s trajectory, serving as the bridge between traditional finance and decentralized systems while unlocking entirely new categories of applications and business models.

Stablecoins represent the first widespread implementation of programmable money—digital assets with embedded smart contract logic that enables automated, conditional execution of financial operations. This transforms money from a passive store of value into an active participant in business logic, enabling automated compliance checks, conditional payments, time-locked rewards, and self-executing escrow.

CBDC Concerns:

Concerns remain about future technology with a more Orwellian feel.

Central Bank Digital Currencies (CBDCs) represent the digital form of sovereign currency issued directly by a country’s central bank, functioning as digital cash with the full faith and backing of the government. As of 2025, CBDCs have emerged as one of the most significant developments in global monetary policy, with 134 countries representing 98% of global GDP actively exploring or developing these digital currencies.

A CBDC is fundamentally different from cryptocurrencies or stablecoins because it is issued by a central bank rather than private entities. Unlike Bitcoin or other decentralized cryptocurrencies, CBDCs maintain centralized control under a central bank’s authority and serve as legal tender. They would function as a digital representation of fiat currency, offering the same three essential properties of money: a medium of exchange, store of value, and unit of account.

At the moment, CBDCs exist in two primary forms:

Wholesale CBDCs: Intended for financial institutions and interbank settlements, facilitating large-value transactions between banks and other financial entities.

Retail CBDCs: Designed for everyday use by individuals and businesses, enabling direct transactions between consumers and merchants. These would replace or supplement physical cash and stablecoins for daily transactions.

What’s the big deal? Isn’t this similar to how Central Banks already operate?

Not exactly.

A concern exists that CBDCs at a retail level would start to take on legislative functions usually provided by governments themselves by incentivizing retail CBDC holders to make transactions of a certain type.

Want to keep your entire paycheck this month? You need to spend 75% of it in the next thirty days or the CBDC issuer might give your CBDC wallet a haircut.

Some department store is a concern for the Central Bank, and might be facing bankruptcy? The CBDC issuer might provide an incentive to use your CBDC tokens at the department store this month instead of buying your goods online.

How do stablecoins connect with CBDCs? Well, some people are viewing stablecoins as a gateway experience that could lead to a more natural adoption pathway for eventual CBDC adoption at the retail level. Stablecoins today, retail CBDCs tomorrow.

Ok, but why does the U.S. Treasury care so much about stablecoins?

Good question.

Everything we’ve talked about so far has been pretty easy to understand. This next part is a more technical understanding of where money (in our case U.S. Dollars) comes from and why stablecoins are such an interesting new addition to the global landscape of USD liquidity.

Modern liquidity—the U.S. Treasuries Question:

What many of the Cyberpunk 2077 game players from our introduction might not have known is that an existing Eurodollar system of dollar liquidity has been in place since the 1960s.

To understand it and how stablecoin capital might impact the global liquidity environment, we will first need to understand where new dollars come from.

Unlike most dollar allocators, like funds, pensions, and endowments which allocate capital out of existing pools of dollars, or by gathering up investor’s funds to allocate, three systems/entities are able to create new dollars by either lending them into existence or by printing those dollars into existence.

The Fed

The first, and best-known, is the Federal Reserve, which can create new dollars through various mechanisms including Open Market Operations, Quantitative Easing (QE), Repo and Reverse Repo Operations, Discount Window Lending, etc. Each of these has a technical mechanism underneath them, but generally the Fed is able to create new dollars to lend whenever they need to.

U.S. Commercial Banks

The second, and more esoteric to understand is the U.S. commercial banking system, which creates the vast majority of dollars in circulation through the process of “funding liquidity creation”—when banks make loans, they simultaneously create deposits on their balance sheets, effectively creating new money without requiring existing cash deposits.

Between 2001 and 2020, an astounding 92 percent of deposits in the U.S. banking system resulted from this funding liquidity created through lending activities, averaging $10.7 trillion per year—equivalent to 57% of GDP.

Importantly, though, this dollar creation is backed at the banking level by assets (mostly U.S. Treasuries) held on those banks’ balance sheets. Banking regulations can vary over time, but generally a U.S. Treasury can fund around ten times the amount of the face value of the Treasury in U.S. Dollar loans.

The Eurodollar System

The third, and most important for our understanding of stablecoins, is the offshore Eurodollar market, which allows foreign banks to create dollar-denominated deposits and loans outside U.S. jurisdiction, extending the dollar creation mechanism globally through the similar banking principles applied by U.S. domestic banks, but without U.S. Federal Reserve or U.S. state-level banking regulations.

Importantly, Eurodollar credit creation is notoriously opaque, as global banking institutions do not have to report new loans to U.S. regulatory bodies. While U.S. commercial banks can only create a limited amount of loans—traditionally linked to their capital base and regulatory ratios—Eurodollar lenders face different constraints.

For Eurodollar lenders, it is generally assumed that many of their liabilities are supported by comparable forms of collateral, such as Treasuries or short‑dated dollar assets, but there is no definitive accounting.

While U.S. commercial banks generally maintain a loan-to-backing asset ratio close to 10x, supported by high-quality assets like U.S. Treasuries, in Eurodollar markets, research suggests collateral reuse and “collateral multipliers” vary widely but range in estimate from 2x to 5x or higher in some parts of the Eurodollar/shadow banking system.

This absence of transparency has led to persistent uncertainty about the true scale of global dollar liquidity, as the Eurodollar market can expand or contract credit without the Federal Reserve’s direct oversight, thereby exerting significant influence over international funding markets and global financial stability.

And this is why stablecoins matter to the U.S. Treasury.

The Treasury’s Perfect Storm:

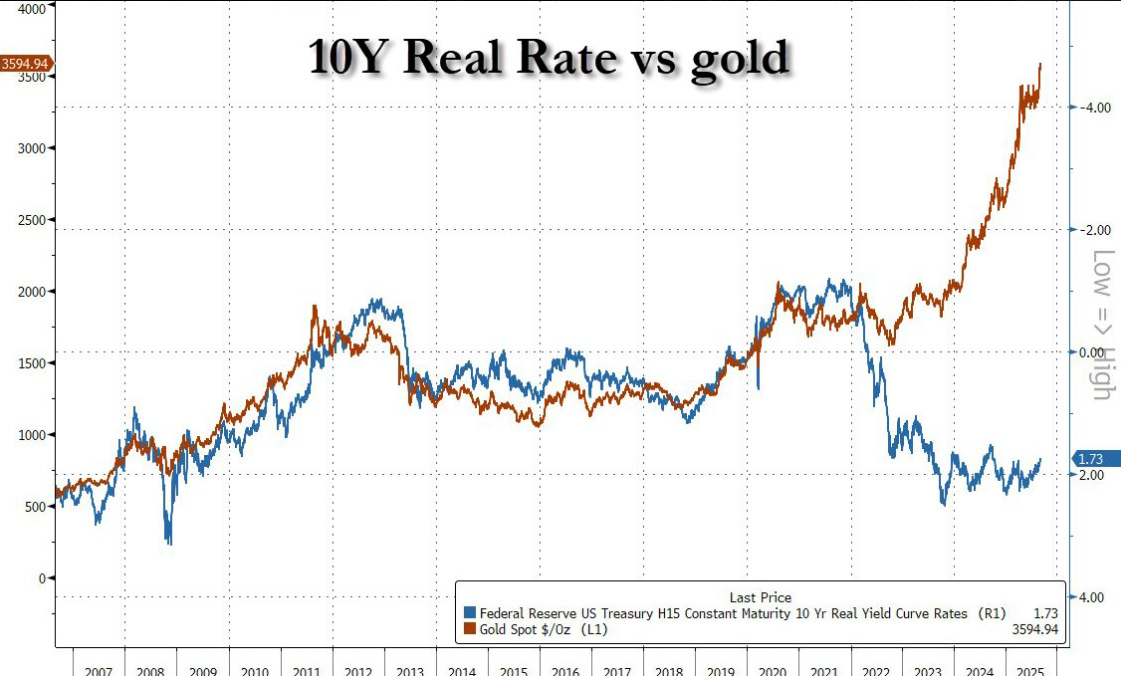

The U.S. Treasury finds itself with a U.S. debt load that is very high, with dramatically high interest rate expenses relative to U.S. tax receipts, and with global investors moving from U.S. Treasuries to gold.

Source: https://x.com/zerohedge/status/1964813380839211312

In the aftermath of the Covid response and the reemergence of inflation in the US, the last few years have witnessed the biggest selloff in long-duration U.S. Treasuries in decades, and unless those interest rate levels move lower, and the U.S. Treasury can find a way to sell more U.S. Treasuries into the market, they will potentially enter a debt spiral that could cause the U.S. to experience even higher levels of inflation as long term U.S. Treasuries sell off.

DOGE. Tariffs. The sale of golden passports. Government shutdown. All of these options have yet to balance the annual fiscal deficit the U.S. finds itself in, and leave the U.S. with few options.

However, if stablecoins start to absorb a significant market share of eurodollar transactions as a high-speed alternative to eurodollar providers, then the amount of U.S. Treasuries that back the global dollar system would likely have to increase, as stablecoins are backed with U.S. dollar-based assets like U.S. Treasuries at a 1-to-1 ratio, while the existing Eurodollar system is backed opaquely with a range of approximately 2x to 5x that we explained earlier.

Despite the ongoing decline of the dollar, the U.S. Dollar remains the currency of account for 54% of global trade as of 2025.

If eurodollar transactions migrated to USD stablecoins, then the net amount of backing by U.S. Treasuries would, at a global level, need to increase.

The result would be that the global eurodollar system would migrate to stablecoins, and provide a natural new place to sell Treasuries.

As a result, world players are starting to push back on this idea:

Russian President Vladimir Putin’s adviser, Dmitry Kobyakov, accused the US of orchestrating a crypto strategy to eliminate its $35 trillion national debt through the manipulation of stablecoins.

The debt problem

The adviser drew parallels to historical US debt strategies from the 1930s and 1970s, arguing America plans to solve financial problems “at the world’s expense.”

He stated:

“The US plans to solve its financial problems at the world’s expense—this time by pushing everyone into the ‘crypto cloud’. Over time, once part of the US national debt is placed into stablecoins, Washington will devalue that debt.”

He described a multi-stage process where the US would transfer its currency debt into crypto instruments before implementing devaluation.

Kobyakov characterized this as a deliberate scheme to eliminate sovereign obligations through digital asset manipulation:

“They have a $35 trillion currency debt, they’ll move it into the crypto cloud, devalue it—and start from scratch.”

Source: https://finance.yahoo.com/news/putin-adviser-accuses-us-planning-000019647.html

Couldn’t the same thing happen to U.S. domestic banking?

In a word, ‘No’.

The GENIUS Act was crafted to prevent stablecoins from accruing interest, which would eat into the market share of domestic U.S. banking.

By mid 2025, U.S. banks were growing concerned about stablecoins, and they potential they would siphon away U.S. Dollar deposits.

Source: https://www.wsj.com/finance/currencies/why-banks-are-on-high-alert-about-stablecoins-2f308aa0

As a result, Section 8 of the GENIUS Act explicitly prohibits payment stablecoin issuers from paying “any form of interest or yield” to stablecoin holders solely in connection with holding, using, or retaining the stablecoins. This prohibition is fundamentally different from the reserve backing requirements and represents a clear competitive barrier designed to protect banking deposits.

Summary:

U.S. dollar-denominated stablecoins offer a complex addition to the USD liquidity and transaction systems.

They are a faster technology that will be the new digital native currency for Web3, and DeFi projects.

They will be central to the high-velocity AI agent world of advanced AI transactions where AIs will operate freely on the internet with defined specifications.

They are likely a gateway experience for eventual CBDCs with everything that they bring.

And potentially, most importantly, they offer a potential new entrant into the eurodollar banking system that could eat into the market share of the legacy eurodollar banking system, and in doing so provide a new home for a large amount of U.S. Treasuries.

Night City residents would be proud.

We hope you’ve enjoyed this post on “How to think about Stablecoins”. Please subscribe to our Substack for our future posts, or if you have some spare dollars please consider one of our paid tier subscriptions for access to our Monthly Market Compass reports.

Until next time.