Monthly Market Compass: December 2024

Trump begins to make moves while DOGE assembles in the wings. Do global markets believe in U.S. Exceptionalism? We are about to find out. U.S. inflation and equity markets hang in the balance.

Hello again, and welcome to our Monthly Market Compass for December 2024. We send these chart heavy market summaries at the beginning of each new month for both our paying and free subscribers.

Please be aware that these notes are not investment advice and should be regarded as entertainment and informational content only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: Economy (currently focused on the potential for a Recession), Inflation, and Geopolitics. A conclusion follows these sections. Enjoy!

Introduction and Market Observations:

Welcome back to month two of a pending Trump 2nd term.

We have a lot to talk about and I’ve saved all of the long form theorizing for this month’s conclusion. So let’s blitz through where markets are currently, and then if you’d like some thought provoking ideas about where things will go from here you can read all of that towards the end.

In our November note, we explored several key ideas following the U.S. election results. As we move into December, let's recap those concepts we discussed:

Crypto markets were highlighted as the "easiest short-term trade" due to potential regulatory clarity under Republican control.

The U.S. Energy complex, geopolitical re-shoring efforts (tariffs fall under this topic), and AI/robotization efficiencies all point to a domestic and near-shore manufacturing boom.

Gold remains a strong focus, with various institutions raising their targets and a persisting divergence between the yellow metal and long-term U.S. Treasuries as a key indicator of global reserve market preferences and inflation concerns.

We emphasized the U.S. Dollar as a crucial factor for market performance under the new administration, as our two correlation scenarios of Reagan's first election and Argentina under Milei both had equity markets move in the opposite direction of the local market's currency.

Long-duration bonds were suggested as a potential opportunity if entitlement spending cuts materialize under Trump.

The stock market was identified as an area of interest, given the likelihood of policies prioritizing market performance, and Trump's natural inclinations: "America must win".

So the Dollar remains in focus for us currently. And inspecting it this month we see that it might have rolled over during the previous month:

Source: https://www.marketwatch.com/investing/index/dxy

As we noted last month, the pair trade of Gold to Bitcoin appears to be re-converging after a summer apart, with Gold moving down:

Source: https://www.kitco.com/charts/gold

With Bitcoin’s and Crypto’s move up, not surprising given the inflows into the crypto markets:

Source: https://x.com/zerohedge/status/1860526770371396027

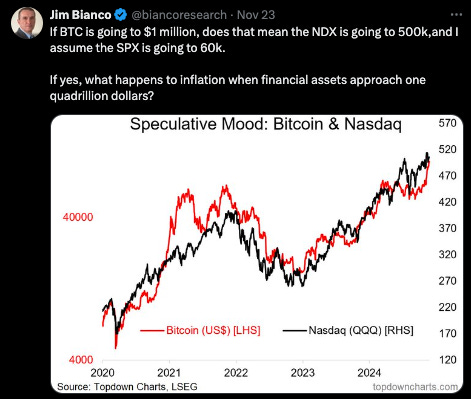

Those inflows put Bitcoin back on the Nasdaq trend:

Source: https://x.com/biancoresearch/status/1860456881912721611

Inflation Watch:

Much of the inflation watching world is fixated on the chart below - how this period today could continue to rhyme with the 1970s with respect to inflation:

Source: https://x.com/RealEJAntoni/status/1856839200177344619

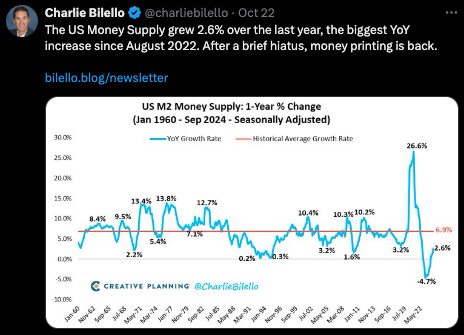

M2 has been increasing in support of this concern:

Money Printing: https://x.com/charliebilello/status/1848903521162183040

Economy Watch:

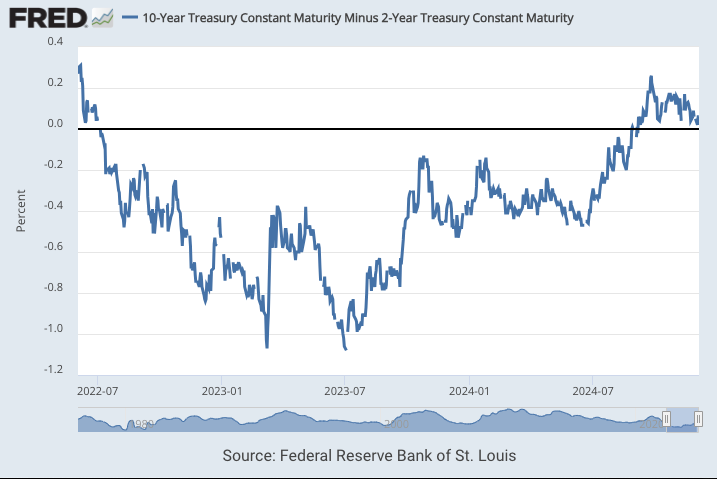

We have a weird set up in economic activity. While Equities and Crypto continue to rip, the Yield curve is only a few basis points from re-inverting:

Source: https://fred.stlouisfed.org/series/T10Y2Y

Under normal circumstances, an increase in Fed Funds would signal a coming rise in Unemployment:

Source: https://x.com/bravosresearch/status/1859235577985687838

Which is supported by numerous other indicators, such as Small Business Earnings:

Source: https://x.com/bravosresearch/status/1859292173973455148

And multi decade high Credit Card defaults:

Source: https://x.com/bravosresearch/status/1864331778577846344

Warren Buffet is loading up on cash:

Source: https://x.com/jessefelder/status/1859623289414615471

Meanwhile the U.S. Retail world is deeper into equities as a percentage of assets than any other point in the last seventy years - likely due to the outperformance of equities in the post COVID timeframe:

Source: https://x.com/TicTocTick/status/1855637987356283112

Junk bonds spreads to Fed Funds are at a low, which is never good:

Source: https://x.com/TaviCosta/status/1846326174487642455

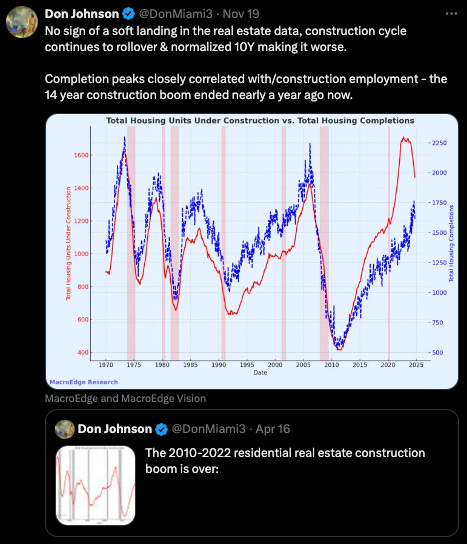

Housing under construction vs total housing completions looks like we are headed towards a downturn:

Source: https://x.com/DonMiami3/status/1858869449723383919

And the 10yr rate looks like it is pointing to a downturn in 2025:

Source: https://x.com/PeterBerezinBCA/status/1862850173111509095

Geopolitics:

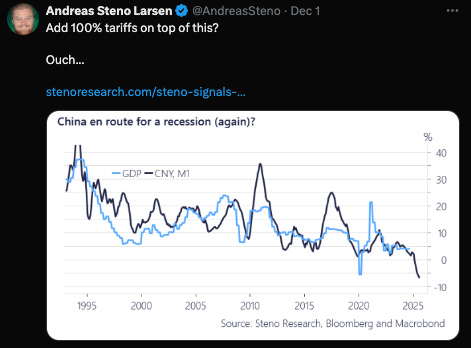

Elsewhere, China looks like it might be headed towards a Recession:

Source: https://x.com/AndreasSteno/status/1863334519404650670

ISM and Liquidity Overview:

If we look at the yield curve as a predictor of the ISM, then directionally, we are headed up (not down) in the ISM in 2025:

Source: https://x.com/AndreasSteno/status/1858506392228794793

Conclusion and Thoughts on the Market:

So how do we make sense of all of this?

Last month we looked at two scenarios that hold the potential to rhyme with what will occur soon in U.S. Markets following the re-election of President Trump. Those two examples were the election of Ronald Regan as U.S. President in 198?, and the election of Javier Milei, in Argentina last year.

The key focus area that dictated the direction of those two example markets was the local currency. In the early 80s Regan and the Fed needed to strengthen the U.S. Dollar following the inflation of the 1970s. A strong dollar followed and the U.S. equity market turned down.

By contrast Javier Milei was able to devalue the currency while reducing inflation. Argentina can source most goods locally, and this tango dance between the currency and subduing the already dramatic inflation in Argentina lead to a surge in local Argentine equity markets.

The U.S. has a similar set up to Argentina in that most goods can be manufactured domestically through the combination of re-shoring efforts and cheap energy. Add in the potential for large efficiency gains from LLM and robotization and U.S. might be on the cusp of an incredible golden age of domestic production. Chip manufacturing and other high value manufacturing will need to be re-shored without destabilizing Asia, but this seems achievable.

But importantly, where Javier Milei had a clear, urgent, and palpable mandate to focus on Inflation, the impulse to control inflation in the U.S. for Trump is not as urgent and more of a theoretical one as inflation feels subdued despite increased yields in duration bonds.

Something that I continue to point here is the Gold markets in contrast to long term U.S. Treasuries as a key indicator of global sentiment on U.S. Treasuries and inflation.

Elon and Vivek’s DOGE is titularly focused on creating government efficiencies, and not on curbing inflation.

This begs the question - that if a real downturn in economic activity manifests in the coming months for Trump, how will Trump react?

The adventurous fiscal policies of the Biden administration in the post-COVID era might be too tempting for Trump. He could enact policies that are themselves inflationary, knowing that the Inflation they cause will be temporary.

Where Monetary Policy was the main lever of the early Regan years, with Elon and Vivek the Fiscal restructuring from DOGE might be the most important inflation constraint for the U.S. today, regardless of short term policies by Trump.

Given this backdrop, Trump could have short term fiscal spending policies that the market could view very differently than similar short term policy’s under Biden.

In this view, Trump might do one time inflationary policy moves to ease the transition of re-shoring and near term economic pain, blame the previous Biden administration for the situation and count on Markets to look through to long term cost cutting and a reduction in Fiscal spending with the narrative of U.S. exceptionalism.

The longer duration part of the curve seems to be moving in that direction already:

Source: https://x.com/AndreasSteno/status/1863634167730208860

In this scenario, Trump would react to an economic downturn with Executive Fiscal policies that were similar to Biden COVID efforts but different this time in their target. Biden offered various student debt payment moratoriums, or outright forgiveness. But the subtext for student loans is that they skew differently in terms of political affiliations.

Broadly speaking and referencing the NYT graphic in the link below, men and women in the U.S. pay down student debt at different rates. Because of this, the forgiveness of student debt impacts women more, and as such helps Democrats more than Republicans.

NYT: https://www.nytimes.com/interactive/2023/07/13/opinion/politics/student-loan-payments-resume.html

Perhaps for Trump, similar efforts for modified workout programs for Economic Injury Disaster Loans (EIDL) would be a type of Republican skewing loan forgiveness program that would fit the bill of enabling some amount of economic recovery at the expense of resurgent inflation.

For reference: EIDL loans originated between 2020 and 2022, and assuming borrowers took full advantage of the 30-month deferment and all Hardship Accommodation periods, full repayments could begin as early as March 2025 for the earliest 2020 loans, and as late as December 2027 for the latest 2022 loans. The majority of borrowers would likely start full repayments between 2025 and 2026, with those who received loans later in the cycle or took maximum advantage of deferment options potentially extending into 2027.

Small business owners skew Republican. So while any modification of the loans would be inflationary, politically the modifications would align with Trump’s base.

Source 1: https://news.gallup.com/poll/284396/small-business-owners-highly-engaged-2020-election.aspx

Source 2: https://www.prnewswire.com/news-releases/new-analysis-answers-the-question-how-does-political-affiliation-affect-small-business-owners-300179891.html

During this, the Fed, whether due to animosity toward Trump or deeper economic concerns, may keep rates high, knowing that the Fiscal DOGEing of the government would be the most needed action the U.S. would need to do, and which is out of their control.

In summary, the key will be first if and how a major economic downturn arrives in early 2025, and then how Trump responds.

The Fed for its part is likely to keep rates high, but Trump might be tempted to pull the fiscal levers that the Executive branch found under Biden as a way of simulating the Economy.

Markets might lift off in that environment despite the Economic downturn.

Inflation pressures would be seen at the front end of the curve, but depending on the interpretation of ongoing DOGE efforts, we could be living with a re-inverted yield curve for a longer period of time.

The Dollar in this environment would be deteriorating, but not in free fall, especially if the rest of the world was also in Recession, and the U.S. was producing cheap goods from cheap energy.

American Energy helps build all goods and the U.S. looks more like Argentina this time around than the Reagan years, embracing short term inflation as a path through.

Until next month.

Please subscribe if you haven’t already and also please consider our Founding Tier.