Monthly Market Compass: January 2025

Trump's deregulation looms as all yield curves uninvert. Will AI-driven efficiencies and DOGE's potential fiscal restructuring offset recession signals? The dance to roll US debt begins.

Hello again, and welcome to our Monthly Market Compass for January 2025. We send these chart heavy market summaries at the beginning of each new month.

Please be aware that these notes are not investment advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections. With this month a focus on the Economy, Inflation, and the Federal Reserve. A conclusion follows these sections. Enjoy!

Introduction and Market Observations:

Hello! And welcome! We are back with another month of our Monthly Market Compass.

There’s a lot going on in the world at the moment. But for the tea leaf readers active in markets much of the focus continues to be on President Elect Trump and the expectations around what his likely policies will be in the first few months of his second Presidency, along with how those policies will interact with the existing investment dynamic in the US.

To recap, in one of our recent notes, we wrote about how in both the first Reagan term of the early 80s and in Milei's Argentina last year, the local currency acted as a counter-directional indicator for the direction of the local stock market, with the US Dollar strengthening in the first Reagan term against a nasty Recession and correction in US markets, while last year Argentina had a decline in their peso against a dramatic rise in the local stock market.

And last month we continued to highlight the US Energy complex as extremely favorable to US energy consumers, as US produced natural gas world continues to run cheaper than global markets.

And with that, let’s look at some other ongoing factors.

The US Dollar has strengthened incredibly since early October:

Source: https://www.marketwatch.com/investing/index/dxy

Which is correlated with the pain in long term Treasuries:

Source: https://x.com/LukeGromen/status/1876995612157096087

Separately, the US is slated to roll a huge amount of debt in the near term.

And importantly, that debt is priced at a very high price relative to the debt that is rolling off.

Which, if rates stays at these levels, will add to an already cumbersome amount of interest expense:

Source: https://x.com/DLineCap/status/1869767146559160412

And -of course- longer duration Treasuries have already detached from Gold as a reserve asset as a reserve asset.

Source: https://x.com/TaviCosta/status/1877045941364207963

Yet Gold has been largely flat in the past few months, despite the rotation into it from US Treasuries.

The combination of which is leaving everyone debating the path forward: Austerity, Inflation, Growth Miracle, or some combination.

Source: https://x.com/LukeGromen/status/1872712327558250935

To add fuel to the fire, the SP500 looks overvalued, with PE valuations currently at a level that implies a low rate of return for the next decade.

Source: https://x.com/dailydirtnap/status/1876662034210619619

Trump is making noise about Greenland, Canada, the Panama Canal, and the Gulf of Mexico, which -to my eye- all seem to be related to firming up the US shipping lanes, including Arctic, and boxing out other non-US players from local shipping lanes.

And with that as prelude, we turn to the Economy…

Economy Watch:

First, for anyone that wasn’t impressed with one 10yr 2yr Yield Curve uninverting, feast your eyes on the rest of the various Yield Curves which have also now uninverted:

Source: https://x.com/bravosresearch/status/1876662703382843560

Those uninverting Yield Curves are almost always a signal for the coming of rising unemployment:

Source: https://x.com/bravosresearch/status/1876320363589861687

Which is in line with other unemployment indicators as well…

such as trucking employment, which looks flat … and which, if it rolls over would be in line with a Recession:

Source: https://x.com/bravosresearch/status/1869771675207909450

Similar story in temporary help:

Source: https://x.com/bravosresearch/status/1876275921692582124

Which would be in line with the more sensitive ‘Jobs Hard to Get less Jobs Plentiful’ stat:

Source: https://x.com/AndreasSteno/status/1869640450350743769

The unemployment rate movement above the 36 month moving average is always a foreboding indicator:

Source: https://x.com/bravosresearch/status/1875676635397287958

Looking more closely at how the US is doing, various other indicators are also showing strain in the Economy.

Home prices look overvalued:

Source: https://x.com/bravosresearch/status/1869435341989625860

The Rent vs. Buy question is also pointing towards overvalued home prices:

Source: https://x.com/VladTheInflator/status/1876679116566503668

And credit card interest rates are increasing:

Source: https://x.com/bravosresearch/status/1867600367959281830

Inflation Watch:

As for inflation, Global M2 is set to decline, which usually means bad things for the crypto world:

Source: https://x.com/JoeConsorti/status/1869485519295648197

While M2 is dropping, the Yield Curve's steepening trajectory now comes from both the front and long end, with apparent inflationary concerns at the long end:

Source: https://x.com/zerohedge/status/1872285161611837922

Though breakeven rates appear to be fairly steady across durations - muddying the waters of how much the market is truly concerned about inflation:

Source: https://x.com/MikeZaccardi/status/1876404943168610431

Federal Reserve Watch:

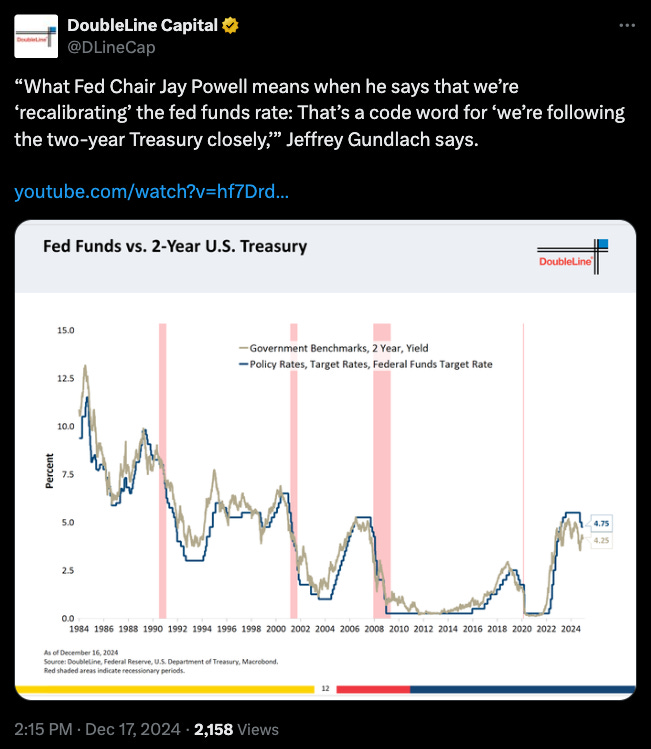

This inflation set up makes figuring out the Fed’s next move a challenge, but the great predictor of the Fed Funds -the US Treasury 2 year rate- looks flat to down in terms of the direction of additional rate cuts at the moment:

Source: https://x.com/DLineCap/status/1869129189929996634

But predicting the Fed Funds is a hard task:

Source: https://x.com/Aureliusltd28/status/1869416785684127783

Conclusion and Thoughts on the Market:

Within the first few weeks of his term, we can anticipate Trump deregulating much of the energy sector, which should cause a massive development and production increase in domestic US Energy production.

The US Energy sector famously has little restraint in development when the stars do ultimately align, so we can expect energy prices to potentially fall as that production comes online.

Inflation expectations seem tepid at the moment, which along with various indicators in economic growth looking weak, point to a potential risk of some type of market sluggishness.

The AI world continues to make advancements, with few signs of stopping, which would add to potential deflation concerns through productivity gains.

And with Energy as one of the major cost inputs into various types of goods throughout the Inflation basket, the risk to inflation seems to be in the direction of lower inflation or deflation for a short amount of time, and although the long term concern of inflation is now pervasive in investors’ minds, the potential for short term deflation seems more immediate to me.

As we noted in last month’s note, Trump is likely to ultimately attempt to stimulate the economy with various immediate fiscal inflationary measures even as the DOGE attempts to cut long term Government spending… but all those things haven’t happened yet.

The market is overvalued by some measures, so the risk for some type of market weakness (at least in the smaller cap part of the market) seems real.

The confluence of all of this makes finding a simple trade a challenge.

But with the Fed possibly in the beginning of a cutting cycle, increasing USD strength, Global M2 contracting, the potential for a market downturn in the US, deflationary pressures from the AI world and the likely Energy price decrease from early Trump Energy sector deregulation, it seems like the ability to lock in short term Treasuries at above 4% is a reasonable place to wait until some more compelling trade comes along.

Moreover, if the Doubleline Tweet above is correct, the Fed is focused on 2yr rates for the direction of their next actions.

The Fed knows that the US needs to roll a huge amount of debt this year, and the fact that Elon Musk and others are politicizing this dynamic will put an unusual amount of political pressure on the Fed to lower rates to help that debt roll.

Ultimately, the US will have to roll its debt on a short term basis, but getting the Fed Funds rate down, even if long term rate increases, will buy time for the DOGE to do its work and hopefully reduce long term inflation concerns as Government spending gets addressed.

Until next month.

Please subscribe if you haven’t already and also please consider our Pro Tier.