Monthly Market Compass: February 2025

In the 1980s a strong dollar crushed US Equity markets. But that was forty years ago and the world has changed. US Economic activity looks bad. But are exceptional US markets the exception or is gold?

Hello again, and welcome to our Monthly Market Compass for February 2025. We send these chart heavy market summaries at the beginning of each new month.

Please be aware that these notes are not investment advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: Inflation, the Economy, and Geopolitics. A conclusion follows these sections. Enjoy!

Introduction and Market Observations:

“May you live in interesting times.” The old quote, said to be a Chinese curse (though dubious in origin), feels like the apt launching point for our discussion today.

The factors at play that swirl around the US Economy are numerous, but all seem to orbit the discussion of the US Dollar, inflation expectations, and the implications for the US Treasury Markets long term.

To recap, the two scissor's blades of this discussion are:

Inflation: with tariffs, trade war implications, a pending low point in the liquidity cycle, the rising Federal Government interest expense, and a lack of a current plan to address US Government entitlement spending.

And, on the other side….

Deflation: the zooming performance in AI capabilities and the prospect for removing large chunks of labor from the Economy, the growing Energy sector and potential drop of energy prices that could follow, a drop-off in various types of economic activity that we will see in our charts, the new administration’s deregulation of multiple parts of the economy, the recent USD strength, the small but impressive DOGE cost cutting in government spending, and lastly the hope that somehow long term entitlement spending will eventually be addressed.

In our November note we looked at two similar election scenarios of Reagan’s first term election, and the recent Argentina election of Javier Milei. And we noted how in each case the direction of the currency matched the inverted direction of the stock market. The USD strengthening into an early 1980s recession, and separately we’ve had a decline in the Argentine peso against the rapid rise in the Argentine’s market since Javier Milei’s election.

What is the backdrop of all of this?

Well, Gold is back on an upward trajectory after moving sideways for a few months following the US Election:

Source: https://www.tradingview.com/symbols/XAUUSD/

The US Government’s Interest Expense is exploding:

Source: https://x.com/bravosresearch/status/1886074598875406742

But despite this the US Dollar is looking very strong post election:

Source: https://www.marketwatch.com/investing/index/dxy

Where is US Dollar strength coming from?

Well, the US dollar's strength is underpinned by several interconnected factors in the current economic landscape.

The United States’s growth trajectory is higher than most other developed markets, which combines with historically wide interest rate differentials to attract foreign investment flows.

The Fed's monetary policy is maintaining these attractive yields, while the AI tech boom - which is still mostly US based, despite new entrants from China - drives continued productivity advantages.

The US energy complex remains an amazingly cheap source of energy for US domestic consumers.

And the dollar's status as a safe-haven currency reinforces all this.

Moreover, these factors seem unlikely to change quickly toward the opposite direction. If anything they seem ready to continue towards more dollar strength.

Here’s the Citi Economic Surprise Index vs DXY:

Source: https://x.com/BittelJulien/status/1879129169084174718

That pink line is the DXY inverted, shooting towards 110 in the next few months. Ouch!

And even the Dollar bears are expecting another month or so of strength before a decline:

Source: https://x.com/AndreasSteno/status/1886079108158837165

Inflation Watch:

Looking at inflation, we see a mixed bag of immediate indicators:

New rents are in decline:

Source: https://x.com/AndreasSteno/status/1882101091523027336

But the Food Index is headed higher:

Source: https://x.com/AndreasSteno/status/1878384114841088425

And energy prices are likely to continue downward as development in the US steps out from a regulatory thaw.

Economy Watch:

The Economy continues to look weak in various ways:

Job openings are declining:

Source: https://x.com/bravosresearch/status/1886794960416203069

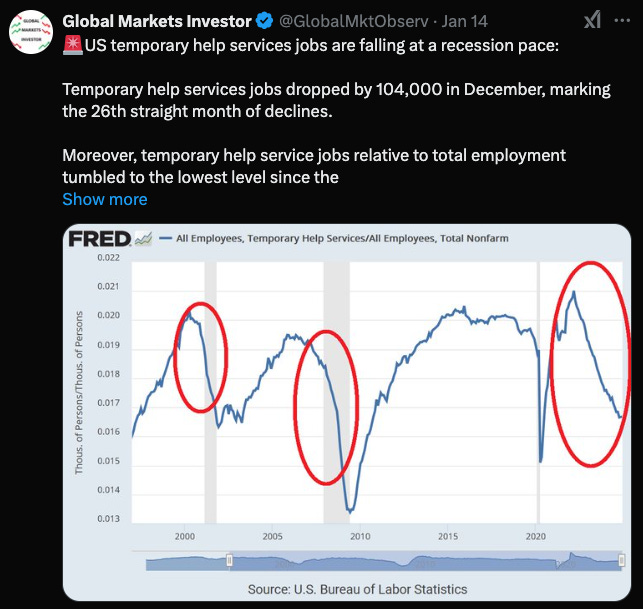

Temporary Jobs Downturn:

Source: https://x.com/GlobalMktObserv/status/1879163712239509764

So it’s not surprising that wage growth is trending down in some lead indicators:

Source: https://x.com/JamesEastonUK/status/1883502383449485657

Home buyers are pessimistic:

Source: https://x.com/bravosresearch/status/1882413868489855339

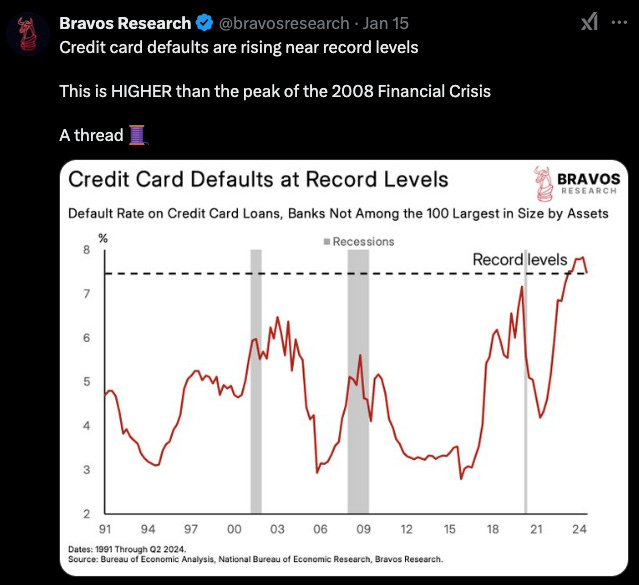

And Credit Card Defaults don’t look good either:

Source: https://x.com/bravosresearch/status/1879535295315726378

So it wouldn’t be too crazy to see some type of short term downturn in US Equities:

Source: https://x.com/i3_invest/status/1879180420673106204

Liquidity and ISM Overview:

In the longer term, various types of liquidity indicators look ready to turn higher:

From a rising demand for Bank loans:

Source: https://x.com/AndreasSteno/status/1886739272549445843

To expected Chinese liquidity:

Source: https://x.com/BittelJulien/status/1879148956166344925

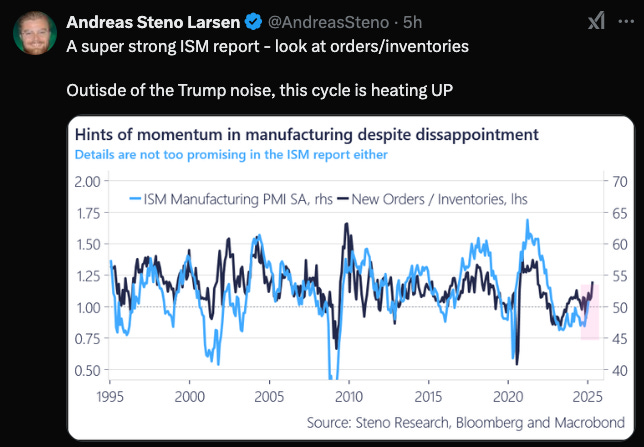

New Orders/Inventories looks to be leading the ISM higher:

Source: https://x.com/AndreasSteno/status/1886696299673628719

And despite the downturn in the Economy noted above, the PMI might be heading much higher:

Source: https://x.com/AndreasSteno/status/1881084693048877123

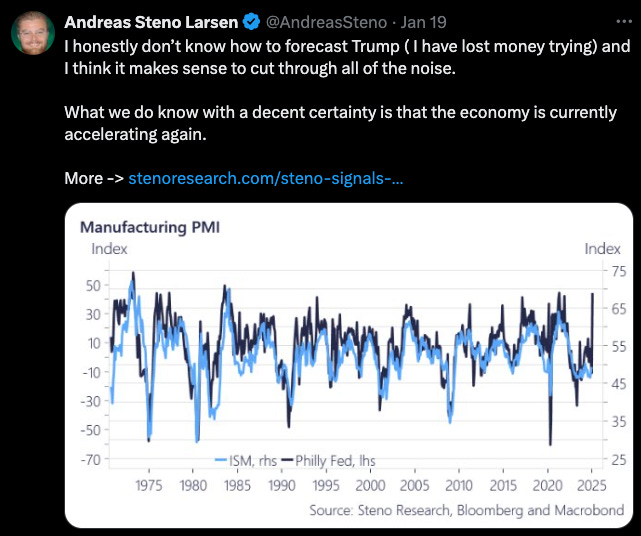

Philly Fed Manufacturing tells a similar story:

Source: https://x.com/AndreasSteno/status/1879884937601638641

Geopolitics:

Recalling the gold chart from the introduction, it’s worth noting that the Gold market appears to be in some kind of fresh turmoil.

The London gold market is currently facing a severe liquidity crisis, with delivery times from Bank of England vaults extending to 4-8 weeks versus the normal 2-3 days. This stems from a rapid 12.2 million ounce outflow to U.S. COMEX warehouses amid potential tariff concerns. While London vaults hold 279 million ounces, only 36 million are available for immediate market use, creating a significant shortfall against 380 million ounces in outstanding contracts.

Source: https://x.com/zerohedge/status/1886603858282959095

COMEX inventories have surged 75% since November 2024, reaching 926 metric tonnes, as market participants seek alternative sources. The crisis exposes structural weaknesses in London's gold market and challenges its fundamental premise of guaranteed prompt delivery, compounded by delayed reporting and unclear regulatory oversight.

Source: https://www.usagold.com/paper-promises-collide-with-physical-reality/

Many have died while waiting for Gold Miners to respond to underlying fundamentals, so I won’t make a call on them.

That said, I’ll simply note that US domestic miners have access to relatively cheap energy, and the backdrop of a rising Gold price, a new de-regulation focused administration, with a US based COMEX repatriation of Gold ongoing:

Source: https://www.google.com/search?q=GDX+chart

Federal Reserve Watch:

We’ve said for months, that the Fed and Monetary policy is no longer in the driver’s seat. Government spending and the Fiscal side are now more important factors in determining long term inflation expectations.

The ‘Fed follows the 2yr’ is a useful phrase, but is not providing much information at the moment.

Fed Funds vs 2yr:

Source: https://fred.stlouisfed.org/series/FEDFUNDS#https://fred.stlouisfed.org/series/FEDFUNDS#

Conclusion and Thoughts on the Market:

Last month I concluded with a view that short duration Treasuries were a reasonable place to be…

But with the Fed possibly in the beginning of a cutting cycle, increasing USD strength, Global M2 contracting, the potential for a market downturn in the US, deflationary pressures from the AI world and the likely Energy price decrease from early Trump Energy sector deregulation, it seems like the ability to lock in short term Treasuries at above 4% is a reasonable place to wait until some more compelling trade comes along.

And I haven’t changed much from this stance.

I still believe the risk of a market downturn, or a large drop in inflation which gives cover to the Fed cutting more, and the potential for clearer buying opportunities is still a great set of reasons to be in cash and short duration Treasuries.

If you're particularly concerned about inflation, then just come in a bit on duration.

That said, if you can look out with a further time frame, then Gold seems to be in a different place structurally than it has been in many decades.

A ‘Grey Swan’ event that President Trump does something to make Gold a more important part of the US financial landscape seems like a real possibility.

And unless entitlement spending gets addressed, then Gold will need to eventually go even higher.

Trump seems sensitive to the need to constrain Federal Government spending, but his inner Real Estate developer will ultimately yearn for lower interest rates and likely some type of short term stimulus to juice markets.

The timing of that sequence seems tricky at best to get right. But the longer things go on, the more you have to just start buying the US as it enters an exceptional moment.

So, some type of wait-and-see approach between short term Treasuries and Gold seems like a reasonable place to hang out until we get better clarity on if the US market will see a downturn.

And along those lines, if I trusted a US Gold miner to not screw up an amazing situation, I might buy it too - as it would be the natural arbitrage between a high gold price (priced in a stronger dollar!), cheap energy (which could get cheaper if economic activity flags), a new deregulation focused administration, a AI fueled productivity boom, and the great sucking sound at the COMEX.

Until next month.

Please subscribe if you haven’t already and also please consider our Pro Tier.

Great insights!