Monthly Market Compass: August 2025

The summer doldrums are here with sideways action across many markets. The battle between Fiscal and Monetary continues with President Trump raging against the political machine.

Hello again, and welcome to our Monthly Market Compass for August 2025. We send these chart heavy market summaries at the beginning of each month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: an introduction and inflation watch, an economy section, a Fed focused section, and a geopolitics and commodities section. A conclusion follows these sections. Enjoy!

Introduction and Inflation Watch:

Welcome back to another month!

Many of the macro fixtures we’ve discussed in previous months continue to stay in place, despite the political raging over US employment numbers.

For awareness, the July jobs report certainly didn't disappoint in terms of drama. US unemployment ticked up to 4.2% from 4.1% in June, with the economy adding only 73,000 jobs. More importantly, the Bureau of Labor Statistics revised down May and June job creation by a staggering 258,000 positions total. That's the largest two-month revision outside of a recession since 1967.

President Trump's response was swift —he fired BLS Commissioner within hours of the report hitting the wires. Trump declared the numbers "RIGGED" to make Republicans and himself "look bad," pointing fingers at the BLS head—a Biden appointee—for allegedly cooking the books "for political purposes."

In our April note conclusion we wrote that:

…with the hyper-political nature of the US during the recent election cycle, and the dramatic nature of the first few months of Trump’s second term, it seems like all options are on the table for President Trump and his team.

One thing they could do is to review the various government metrics during the past few years (perhaps throwing many of those metrics out entirely) and declare that the US has already been in a Recession for the last few quarters (playing the political game of piling onto the Democratic party who has lost the support of the American people, and blaming the Biden Administration further for the current predicament the US finds itself in), and is now on its way out of a Recession.

Given this past month’s events, we don’t count out the possibility that President Trump could do something that would be in this vein, though he may just try to power through the moment.

The US Treasury curve remains high at all point of the yield curve, forcing the US to navigate a challenging path to finance its debts.

Net interest payments for the US remain high, with the US paying an increasing share of its budget on financing its spending.

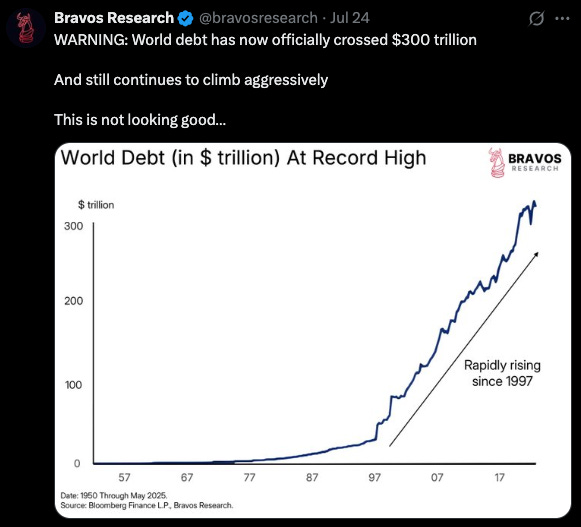

Global debt levels remain high alongside the US:

Source: https://x.com/bravosresearch/status/1950926926656450957

Last month we showed how a note that President Trump had sent Fed Chair, Jay Powell, on bringing down the Fed funds rate, but this past month Powell kept rates flat.

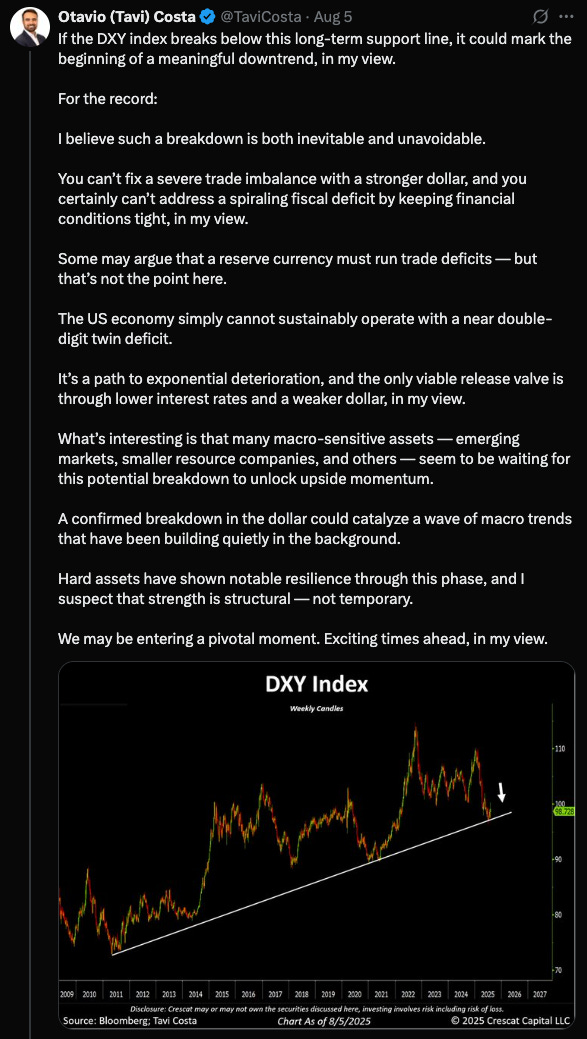

The dollar looks like it could falter further in coming months—though the timing of when might be tricky:

Source: https://x.com/TaviCosta/status/1950757846523506695

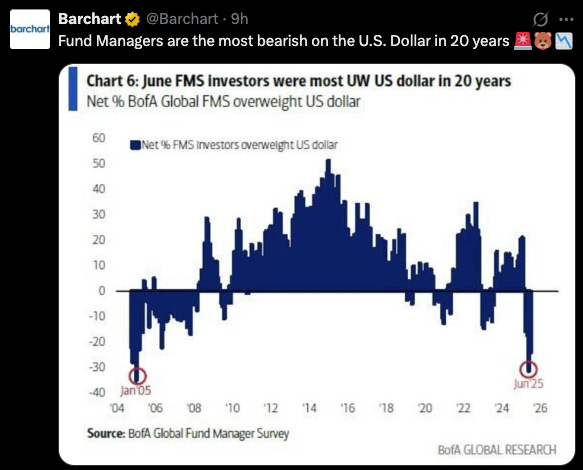

Consequently, the Dollar is unloved by fund managers currently, which we’ve highlighted in our previous notes:

Fund managers bearish on the USD amidst high long term inflation concerns - so some type of pullback on the Dollar might be something to be wary about:

Source: https://x.com/Barchart/status/1953064555011002643

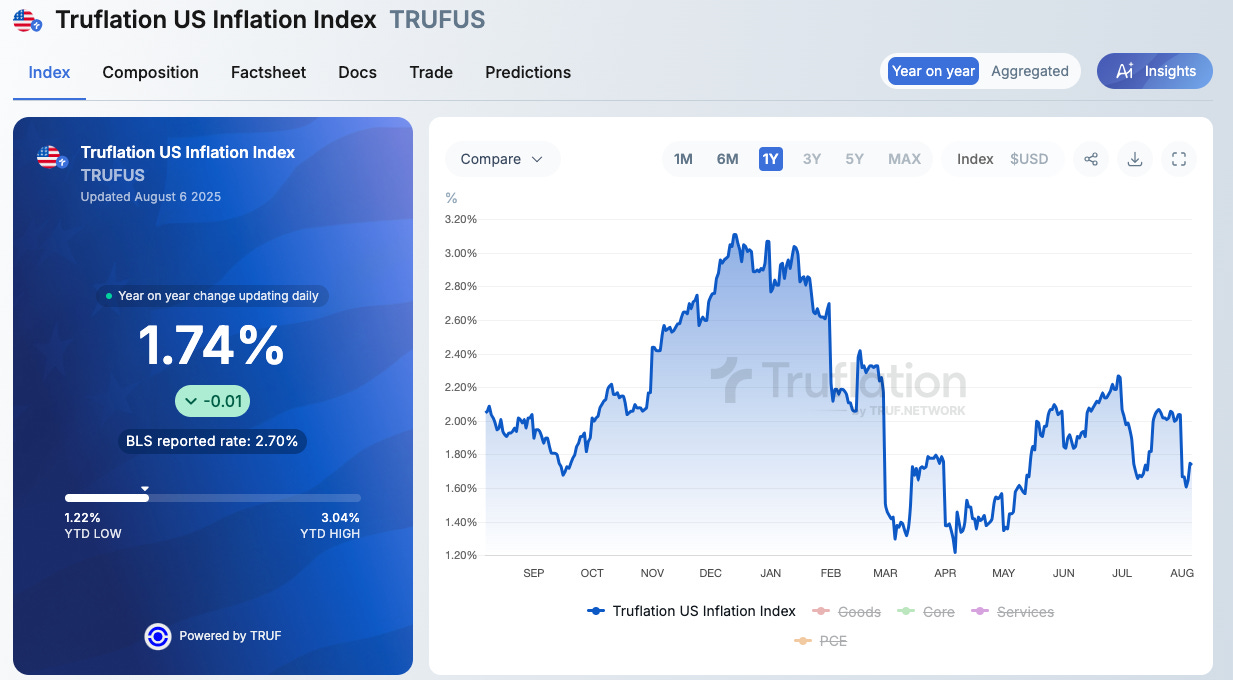

We noted last month how there is a continuing narrative divergence on both current inflation figures and inflation expectations.

CPI continues to show higher inflation, while Truflation figures show current inflation to be much lower:

Source: https://truflation.com/marketplace/us-inflation-rate

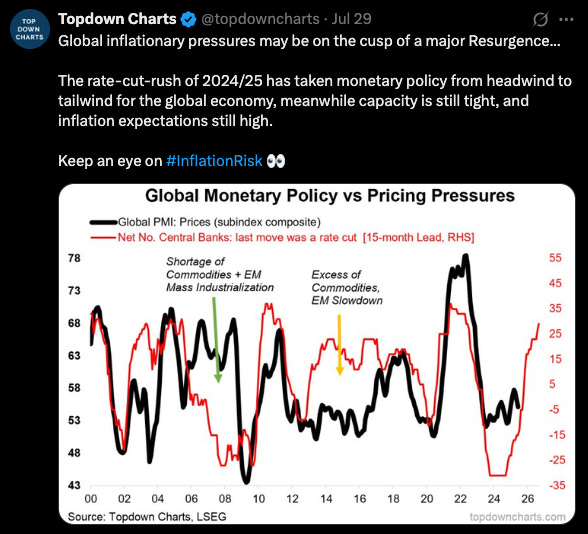

Global PMI prices look ready to start increasing in the wake of global central bank easing:

Source: https://x.com/topdowncharts/status/1950290175785127981