Monthly Market Compass: March 2025

"A national debt, if it is not excessive, will be to us a national blessing." - Alexander Hamilton

Hello again, and welcome to our Monthly Market Compass for March 2025. We send these chart heavy market summaries at the beginning of each new month.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: Economy (currently focused on the potential for a Recession), Inflation, and Geopolitics. I threw in a section on the ISM, Equity Markets, and Bitcoin, this month. And a conclusion follows these sections. Enjoy!

Introduction and Market Observations:

Welcome back to our monthly note! We’ve got a lot to cover so let’s jump right in.

The most important dynamic in macro markets remains the intersection of issues surrounding the US Dollar and US Treasury markets.

The individual pairs of issues that bookend these topics are:

Gold vs. US Treasuries as the global preference of reserve assets.

Inflation vs. Deflation as the outlook for the US Dollar.

The US Deficit vs. DOGE related to US fiscal spending.

US Government Debt vs. US Growth

As we enter the spring season, these tensions have only intensified.

The US Dollar has started to weaken over the last month:

Source: https://www.marketwatch.com/investing/index/dxy

On the inflation front, we're witnessing a fascinating tug-of-war. Inflationary pressures from tariffs, trade war implications, and unaddressed entitlement spending are counterbalanced by powerful deflationary forces: AI-driven productivity gains, the expanding domestic energy sector, and the new administration's regulatory rollbacks.

The DOGE (Department of Government Efficiency) initiatives have introduced a new variable into this equation, with early cost-cutting measures showing promise but still dwarfed by the scale of long-term fiscal challenges.

Meanwhile, the global shift in reserve asset preferences continues to evolve.

The Basel III update for banks significantly impacted the treatment of physical gold in financial markets. It reclassified physical gold as a Tier 1 asset, considered risk-free and equivalent to cash, which improved its status in the global financial system.

Although delayed numerous times, the Basel III rules on bank liquidity began to apply on 28 June 2021, with the full reform coming into force in all markets (Europe was the last holdout) on January 1st of this year, 2025. (Source)

Roughly the same time the Gold price started to trade in a dramatically different fashion than did US Treasury 10yr real rates:

Source: https://x.com/DTAPCAP/status/1777139680599027872

So, while this divergence coincides with growing questions about the sustainability of US debt levels it also coincides with the Basel III banking update.

Now, the Dollar and the US 10yr are strongly correlated - so we will need to see some more weakness in the Dollar if yields are to fall:

Source: https://x.com/LukeGromen/status/1895115088228687919

How exactly did the Dollar perform the last time Trump was elected?

Source: https://x.com/AndreasSteno/status/1897323644277416305

In November we highlighted how Trump’s second term post-election market might compare to both Reagan's first term and Argentina under Milei.

It looks like we are getting elements of both of those historical periods – but with unique characteristics shaped by today's technological revolution and energy landscape.

The most important highlight of November’s note was that the strength (or weakness) of the local currency in each of the two historical periods defined the shape of the associated stock market.

Which makes Trump’s recent focus on devaluing the US Dollar the key factor for managing the ongoing reshaping of the US Economy.

Consider Trump’s newly announced plan - the “Mar-a-lago Accord”:

President Trump announced two weeks ago the idea of a “Mar-a-lago Accord”, that might shape the US Dollar, and the US Treasury market’s trajectory along with US Trade and Security relationships for the foreseeable future.

President Donald Trump’s proposed economic plan dubbed the "Mar-a-Lago Accord," would aim to reshape America's global economic position and address perceived imbalances in trade and currency.

The key components of the Accord would be:

A strategic devaluation of the US Dollar

A debt restructuring converting short term US debt into 100 year ‘century bonds’ with little to no regular interest

Tariffs - likely to penalize countries that don’t take part in the Accord

A Sovereign Wealth Fund

And a Security-Economic Integration that would look to leverage America’s security umbrella to extract economic concessions from allies.

Some sources are indicating that the 100 year bonds would be non-transferable, making the bonds more geopolitical instruments of influence.

The hope being that the US can dodge the high US Interest Expense that is currently snowballing into a larger and larger problem:

Source: https://x.com/bravosresearch/status/1886074598875406742

If the dollar is set to weaken then we might expect inflation to be a concern… let’s check that next:

Inflation Watch:

The coming months are going to be one of those good old fashion debates on what the actual inflation rate is. For people that were around in 2020 and 2021 this might be a replay of those years but in reverse.

Where 2020 and 2021 had higher inflation rates than the Government figures and markets lagged behind, here the actual inflation rate might be much lower than everyone is expecting and once again the Government and markets might be lagging behind.

Truflation is a modern inflation measurement tool that aims to provide a more accurate and timely alternative to the traditional Consumer Price Index (CPI). Where the US BLS tracks CPI by hand through 80,000 data points in an opaque calculation, Truflation tracks 14 million data points in a real time using decentralized oracles, blockchains, and open source algorithms providing full transparency.

The Truflation metric is currently deviating dramatically from market’s expectations of inflation:

Source: https://x.com/AndreasSteno/status/1889774882897973381

If Truflation is correct, then both long bonds…:

Source: https://x.com/AndreasSteno/status/1888947978494206049

…and short bonds may be mis-priced:

Source: https://x.com/BittelJulien/status/1894366260240028056

As we considered in our most recent notes, Trump’s deregulation focus is likely to drive domestic oil and gas prices even lower, exacerbating an already dramatic US Energy dynamic compared to the rest of the world (cheap Oil and Nat Gas in the US vs. the rest of the world).

Those lower Energy prices - which feed into the inflation calculation in numerous ways - are correlated to declining Bond yields also:

Source: https://x.com/AndreasSteno/status/1897334188963192907

The inflation hawks have a different story. Specifically, that we are at the turning of a commodity cycle, which you have to get right on or miss a once in a generation shift to commodities.

Source: https://x.com/TaviCosta/status/1897364467132121557

Economy Watch:

As a reminder, the Yield Curve has un-inverted and now looks to be on the rise:

Source: https://fred.stlouisfed.org/series/T10Y2Y

This is usually a bad sign of the impending Recession that almost always follows a yield curve un-inversion.

To that end, Housing Starts have weakened:

Source: https://x.com/bespokeinvest/status/1893667056341643381

Housing market looks expensive:

Source: https://x.com/bravosresearch/status/1895149125089513490

Which is usually not a good sign for the economy:

Source: https://x.com/bravosresearch/status/1895173963933983135

And usually correlates with a reduction in employment:

Source: https://x.com/bravosresearch/status/1896554360613830889

Job openings are set to trend lower by CPI Core Services:

Source: https://x.com/AndreasSteno/status/1890385612684865961

And Jobs might have turned a corner for the worse:

Source: https://x.com/GlobalMktObserv/status/1894742714974900389

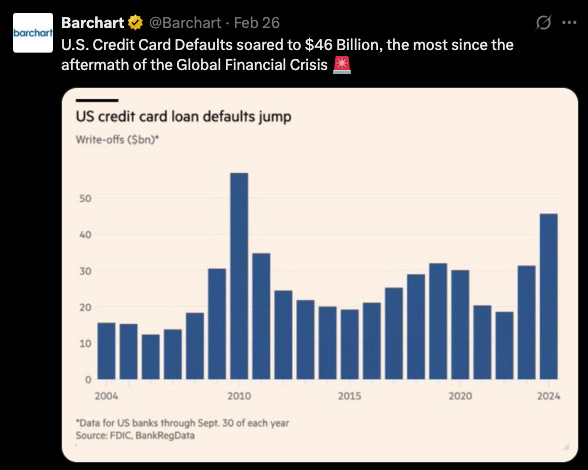

Credit Card defaults are up last year:

Source: https://x.com/Barchart/status/1894847335810978001

Consumer spending tells a similar story:

Source: https://x.com/TaviCosta/status/1894577084783366254

So overall the regular (non-tech) Economy looks to be in a bad place.

Geopolitics:

Turning to Geopolitics…

Gold is arguably the most important Geopolitical asset to watch - as it contends with US Treasury markets for the premier reserve asset status.

And despite a small wobble in Gold Prices we remain near all time highs in the yellow metal:

Source: https://www.kitco.com/charts/gold

Physical Gold at the US COMEX exchange has been correlated with Gold Prices since December.

Source: https://x.com/zerohedge/status/1894175995705360527

That looks like this in detail:

Source: https://x.com/zerohedge/status/1889152370950709623

Gold demand out of Asia is surging with India catching upto China in buying:

Source: https://x.com/KobeissiLetter/status/1894095324270244064

But while Gold is arguably the most important Geopolitical asset, we shouldn’t forget about the Dollar given the ongoing discussions around the Mar-a-lago Accord.

Recall, that we saw in the introduction that the Dollar correlates with the 10yr.

Well the USD and the 10 yr are lead by the Citi Economic Surprise index:

Source: https://x.com/BittelJulien/status/1893612817271435515

That Citi Economic Surprise Index will possibly start to recover in March, and if so then the Dollar and the 10yr will follow in April, but we aren’t there yet:

Source: https://x.com/BittelJulien/status/1895047884460171442

Elsewhere in Geopolitics, tariffs on US trading partners look dramatic, but have yet to make their impact felt on Inflation despite being of Great Depression size:

Source: https://x.com/bravosresearch/status/1894090116160966865

Is Europe the spot to wait out the storm?

Source: https://x.com/MichaelAArouet/status/1895377974129754429

Maybe not.

Federal Reserve and Liquidity Watch:

The way I think about Liquidity involves four pillars. First are the three: the Fed, China, and US Banks loan creation. In addition to those, I view the fiscal side of US Government spending as an additional input to track.

At the moment, the US Government is trying to spend less, and in a YoY calculation is cutting spending through the DOGE Efforts.

Out of the other Big Three, two look like they are growing liquidity (China and Banks), while the Fed has yet to signal a return to cutting.

However the Fed might be a short month or two away from reversing their cutting posture. Let’s look deeper.

We’ve seen above that Inflation might be coming down more rapidly than the CPI would have you believe.

Also the Economy could be stalling, with an increase in Unemployment soon to arrive.

The all important 2yr Treasury, which often leads the Fed Funds rate has dipped under the 4 handle back into the high 3s:

Source: https://fred.stlouisfed.org/series/DGS2

Which is in line with rising rate cut expectations:

Source: https://x.com/zerohedge/status/1894477275329867896

Other rate cut leads think even more are coming:

Source: https://x.com/BittelJulien/status/1878807933498118387

Looking at US Private Banks loan creation, we see that increasing:

Source: https://x.com/AndreasSteno/status/1888898197101146182

And Chinese Liquidity looks ready to increase as well:

Source: https://x.com/BittelJulien/status/1889418501120561570

Longer term these Liquidity inputs will drive assets, but first we need the US Fiscal spending, DOGE, and the Mar-a-lago accord to work whatever magic they hope to:

The ISM, Equity Markets, and Bitcoin:

Looking at Equities, the risk asset of Bitcoin, and the input/lead of the ISM…

The ISM looks a bit flat for now:

Source: https://x.com/AndreasSteno/status/1895390841310793916

But trending higher:

Source: https://x.com/BittelJulien/status/1888165436971237632

Equities might be near a top - but it’s always a vanity trade to try to call the top:

Source: https://x.com/TaviCosta/status/1894456488682557682

Other overvaluation metrics look similar:

Source: https://x.com/Barchart/status/1893711020402803096

But in a chart that should remind us for the Gold vs. 10yr real rate chart from the first section, equities have not been behaving since 2022 either:

Source: https://x.com/i3_invest/status/1894130180861698312

Never-the-less, Warren Buffett has an all time high in the size of his cash hoard:

Source: https://x.com/KobeissiLetter/status/1893313267759563199

And other institutional investors are leaving equities also:

Source: https://x.com/KobeissiLetter/status/1892968419865002136

Turning to Bitcoin:

Bitcoin looks very correlated to global liquidity:

Source: https://x.com/QuintenFrancois/status/1897196682863108165

Looking at this chart again, Bitcoin appears likely to remain flat until April?

Source: https://x.com/Andre_Dragosch/status/1894299843218059519

Other leads tell a similar story:

Source: https://x.com/BittelJulien/status/1895427153321251261

Possibly the top of a channel:

Source: https://x.com/FinanceLancelot/status/1894829098838409420

Long term Bitcoin still looks like a buy:

Source: https://x.com/TuurDemeester/status/1894450800295911805

And is below production cost:

Source: https://x.com/DrProfitCrypto/status/1894347923472765352

Conclusion and Thoughts on the Market:

As we navigate these complex crosscurrents, the key question remains: can the combination of energy abundance, AI-fueled productivity gains, and regulatory reform, with the Mar-a-lago Accord create a "Goldilocks scenario" that attracts (and/or compels) global investment despite fiscal concerns? Or will the weight of government debt and interest expenses eventually force a more painful adjustment?

For the moment the Dollar looks set to weaken, driving down US 10yr rates. The various Economic measures we track seem to support this, and various types of bond trades look better than the set up in Equities for the time being.

Two months ago I liked 2 yrs Treasuries, and last month I liked Gold Miners. I still like the 2yr, but I have not sufficiently worried about how likely a Trumpian move against the Basel III banking regulations might be.

Right now the easiest trade seems to be a bit further out on the yield curve than the 2yr. I’m not sure I like 10yrs in terms of the risk, but picking your duration comfort level and then going there for a month or two while the world waits to see the effects of these geopolitical gyrations, seems like a reasonable thing to do.

The Fed will likely be slow to help out the new administration, so if the economy starts to turn downward, the 2yr will likely have to compel the Fed into rate cuts, which should allow for a bit longer for the trade to exist than if a different party was in office in the US.

Until next month.

Please subscribe if you haven’t already and also please consider our Pro Tier.