Monthly Market Compass: November 2024

Trump has won. The fight for the Dollar begins. Elon takes aim at Government spending. We examine Reagan's first term and Milei's Argentina as possible corollaries to a pending Recession.

Hello again, and welcome to our Monthly Market Compass for November 2024. We send these chart heavy market summaries at the beginning of each new month, but understandably, delayed this month to see what resulted from the US election.

Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes into several sections: Economy (currently focused on the potential for a Recession), Inflation, and Geopolitics. A conclusion follows these sections. Enjoy!

Introduction and Market Observations:

We have a lot to get through this month. Obviously we will discuss the U.S. Election and the results and ramifications, but I’d like to leave that until later.

To start I’d like to run through the charts so we all have the same frame of reference.

So to begin with, let’s review the US Dollar. Here the likelihood and eventual reelection of Trump has correlated with a strengthening of the Dollar into and through the Election. Note the spike in USD strength at the far right edge of the chart, on Election night.

Source: https://www.marketwatch.com/investing/index/dxy

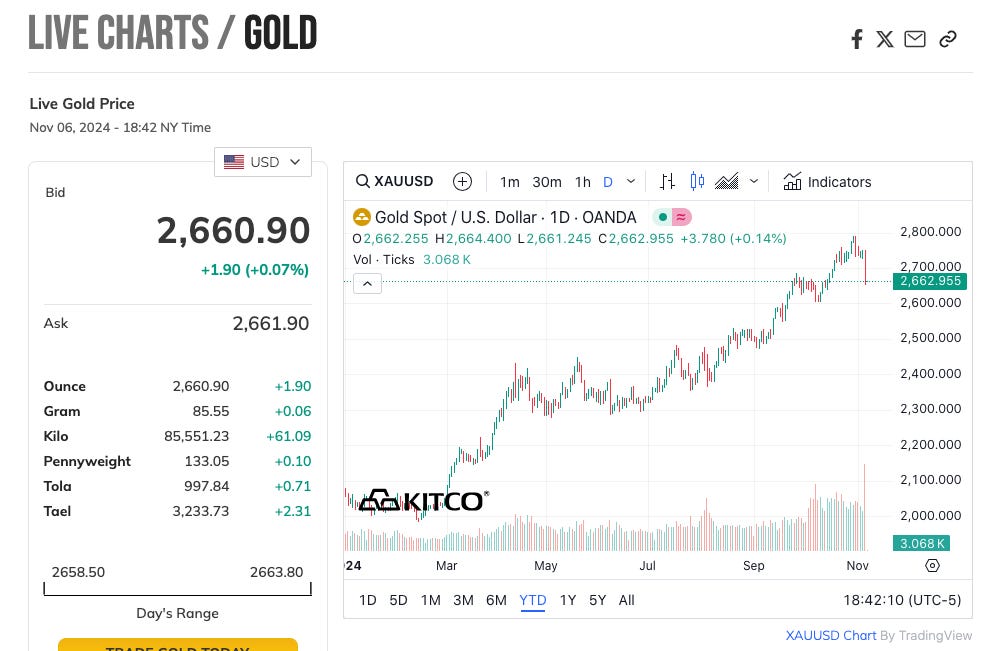

Gold remains near all time highs, though it fell as the Dollar strengthened during the U.S. Election.

Source: https://www.kitco.com/charts/gold

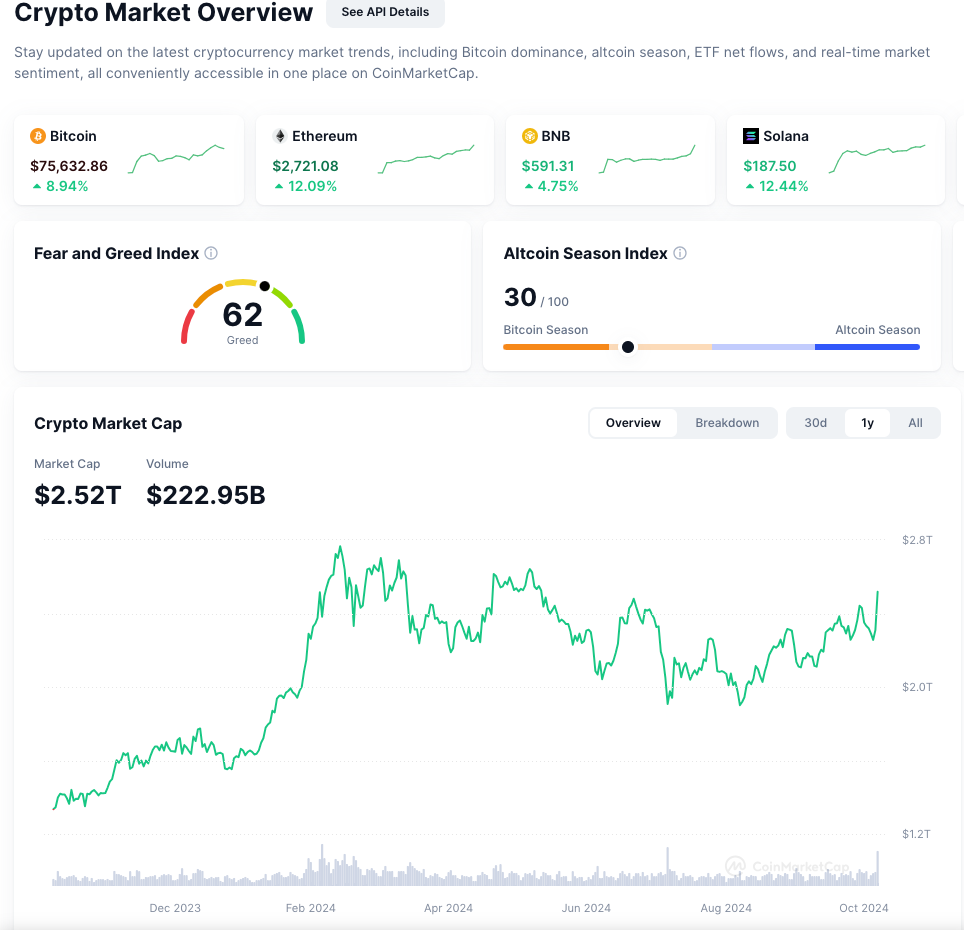

Crypto, by contrast, has surged post-election, on the prospect of regulatory clarity in the U.S., following what is looking -at the time of this writing- as a Republican sweep of the Presidency, Senate, and House. This after months of choppy sideways to down activity in Crypto’s total market cap.

Source: https://coinmarketcap.com/charts/

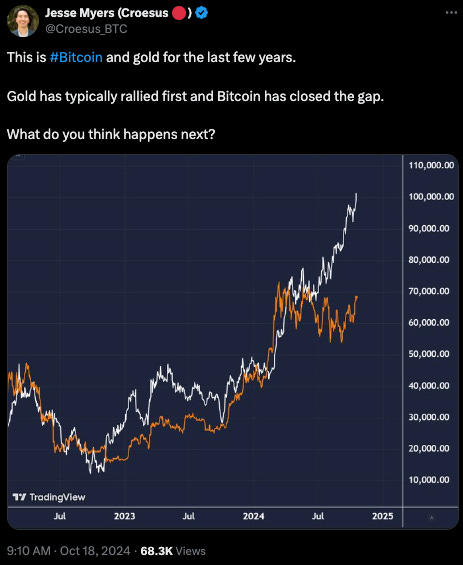

Gold to Bitcoin looks like a re-converging pair trade at this point:

Source: https://x.com/Croesus_BTC/status/1847294288725479471

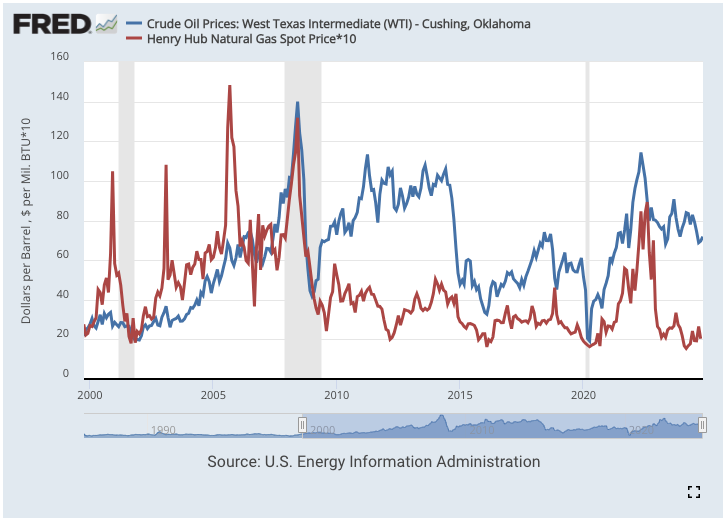

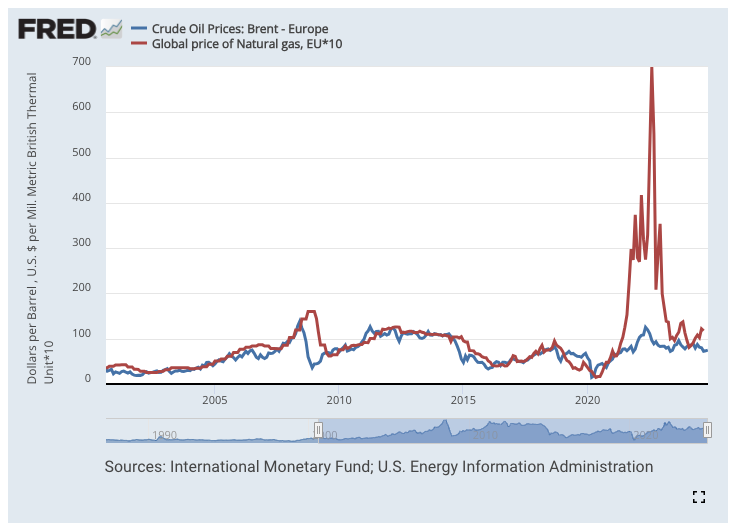

US Energy still enjoys a significant arbitrage in Natural gas relative to Oil:

Which doesn’t seem to be available elsewhere in the world. If anything natural gas runs at a premium to oil:

Source: https://fred.stlouisfed.org/

Inflation Watch:

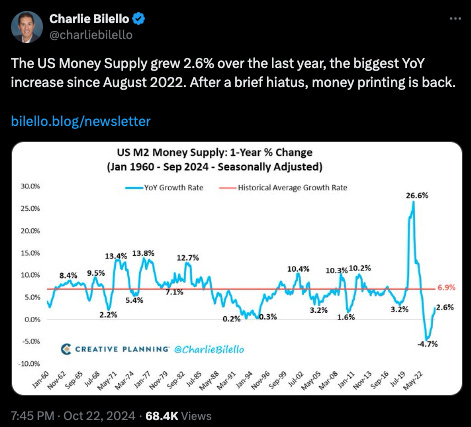

Global Money Supply is on an upswing:

Source: https://x.com/charliebilello/status/1848903521162183040

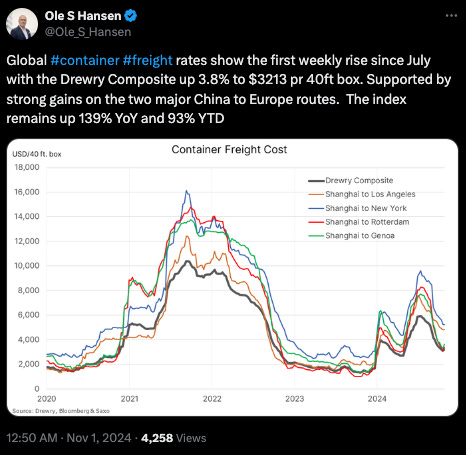

Freight shipping rates are down however after rising into the summer:

Source: https://x.com/Ole_S_Hansen/status/1852241748275171677

Economy Watch:

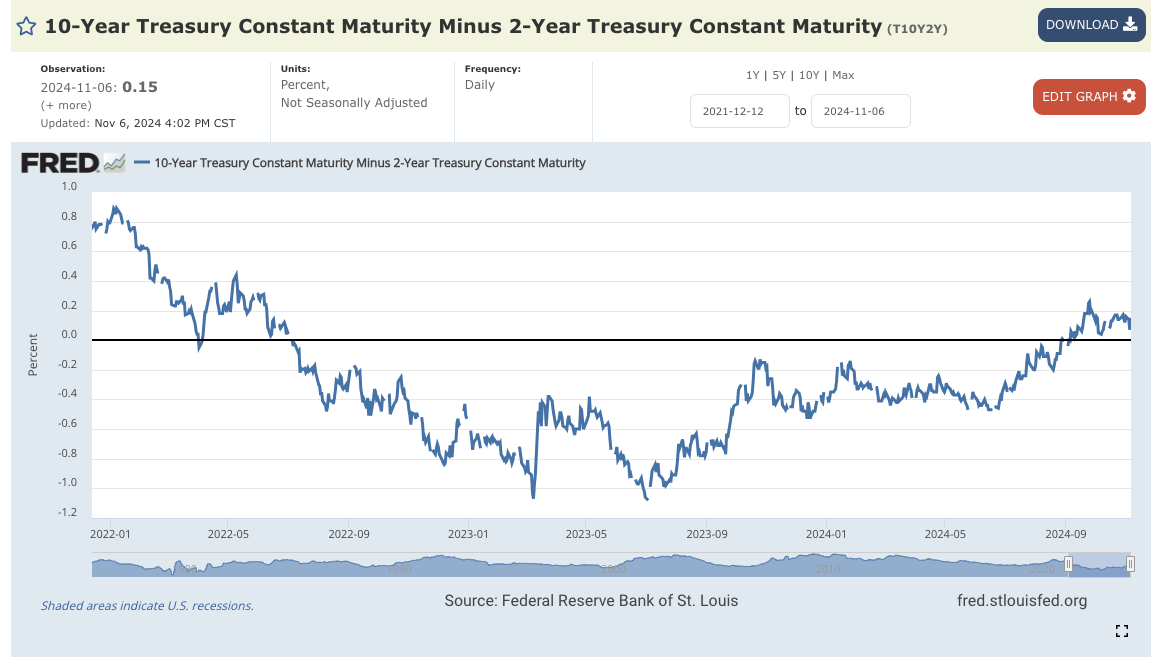

The Yield Curve has un-inverted, but seems to be flirting with re-inverting:

Source: https://fred.stlouisfed.org/series/T10Y2Y

Multiple parts of the Economy still look like they are struggling.

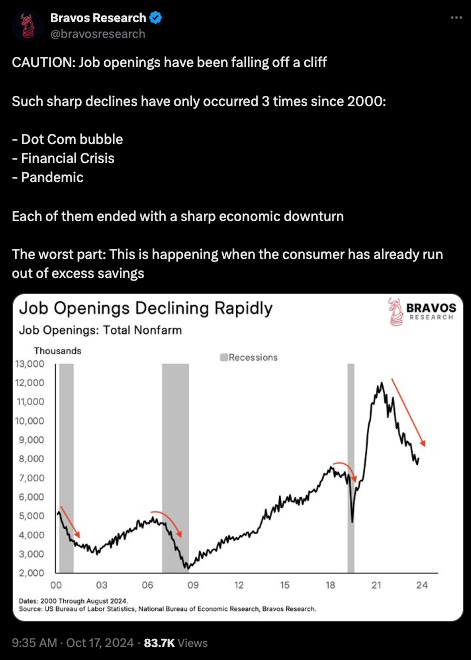

From declining Job Openings:

Source: https://x.com/bravosresearch/status/1846938084178645157

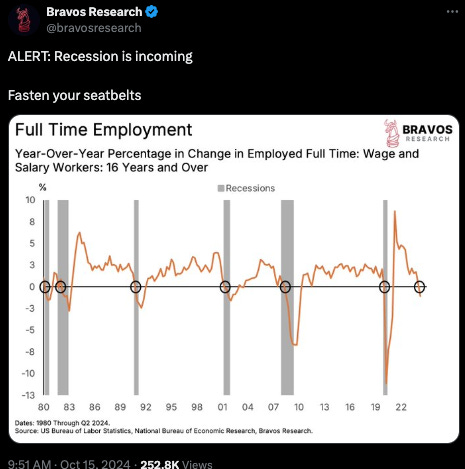

To associated Full Time Employment:

Source: https://x.com/bravosresearch/status/1846217452252024994

Temporary Services jobs are declining:

Source: https://x.com/GlobalMktObserv/status/1842270965637476583

Which together look bad:

Source: https://x.com/Econimica/status/1841920230844678304

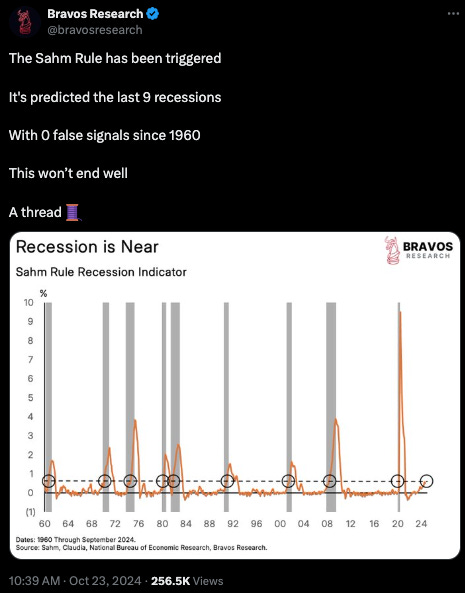

A sharp rise in Unemployment triggers an indicator called the Sahm Rule. It has an impressive track record of predicting recession, and it is currently triggered again:

Source: https://x.com/bravosresearch/status/1849128647875330106

The indicator of Trucking Employment is still in decline:

Source: https://x.com/bravosresearch/status/1842598674976923868

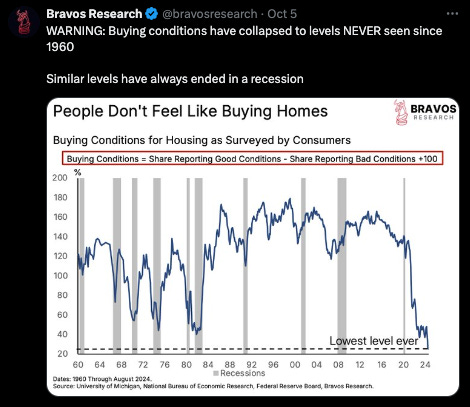

Home buying conditions are low:

Source: https://x.com/bravosresearch/status/1842552002334855528

Geopolitics:

A BRICS conference ended a few weeks ago with a gesture towards a new BRICS currency, and a new rival to SWIFT called mBridge.

The conceived currency in not scheduled for deployment yet, but is conceptualized as having 40% gold and 60% BRICS currency backing.

Likely the world doesn’t really want to get rid of the USD very quickly, so this all gives time for Trump to make whatever moves he will make.

https://www.jpost.com/business-and-innovation/precious-metals/article-823389

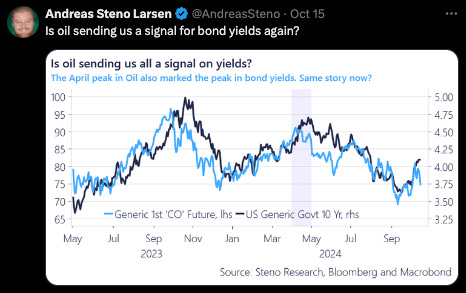

Elsewhere Oil and duration US bonds are in tension with Oil pointing towards a downturn in Bond yields:

Source: https://x.com/AndreasSteno/status/1846077243736383814

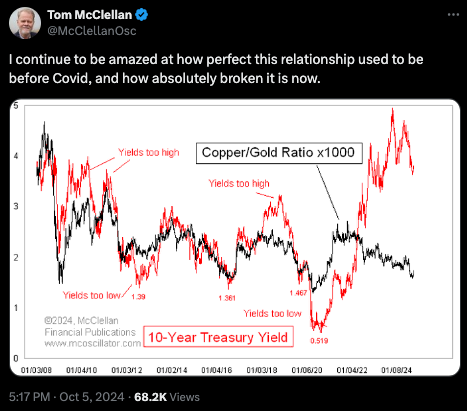

Copper/Gold is still at odds with long term Bonds:

Source: https://x.com/McClellanOsc/status/1842705811166077060

ISM and Liquidity Overview:

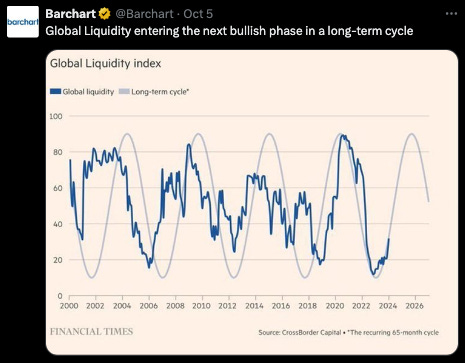

Liquidity looks like it is set to move up:

Source: https://x.com/Barchart/status/1842753246093246853

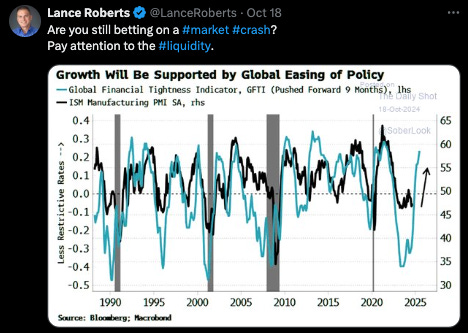

And Global Financial Tightness points towards an increasing ISM Manufacturing PMI:

Source: https://x.com/LanceRoberts/status/1847236533767590306

And the un-inverting Yield Curve seems to echo that idea:

Source: https://x.com/AndreasSteno/status/1843002313193201708

Conclusion and Thoughts on the Market:

Let’s talk about the Election.

To my thinking the two historical parallels we have for this are the first Reagan election, and what we’ve seen this year down in Argentina. Both had Recessions waiting in the wings for a Conservative leader who enacted large spending cuts.

For the Reagan years, let’s set the stage. Reagan gets elected on November 4th, 1980. He is sworn in on January 20th, 1981. Reagan launched his first term’s spending cuts in February of 1981 with proposed budget cuts, including cuts to 200 government programs. A 16 month Recession would begin in July of 1981. And in August, Reagan would sign the Economic Recovery Tax Act of 1981, cutting taxes and reducing government spending again.

US Treasury 10yr rates see their highest rates of all time in September of 1981, and then drop 500 basis points before the Recession is over:

Source: https://fred.stlouisfed.org/series/DGS10

Inflation during this period would begin a decline from election night that would trend down, with a hiccup in the early months of the 1981 Recession.

Source: https://fred.stlouisfed.org/series/CPIAUCSL

Assisted by the Volcker Fed, the US Dollar began a upswing that ended the 1970s Inflation, and would lead ultimately to the highest Dollar value ever in adjusted terms:

Source: https://www.macrotrends.net/1329/us-dollar-index-historical-chart

As you might imagine, Gold sank during the same time frame after a dramatic run up during the carter years:

Source: https://www.macrotrends.net/1333/historical-gold-prices-100-year-chart

The SP500 sank almost immediately after the election and would only start to rebound towards the end of the election:

Source: https://www.macrotrends.net/2324/sp-500-historical-chart-data

While the Reagan era provides one historical parallel, Argentina currently offers a different set of responses.

Next up, let’s look at Argentina:

When Javier Milei took office as President of Argentina on December 10th of 2023, markets had little understanding of what would soon follow.

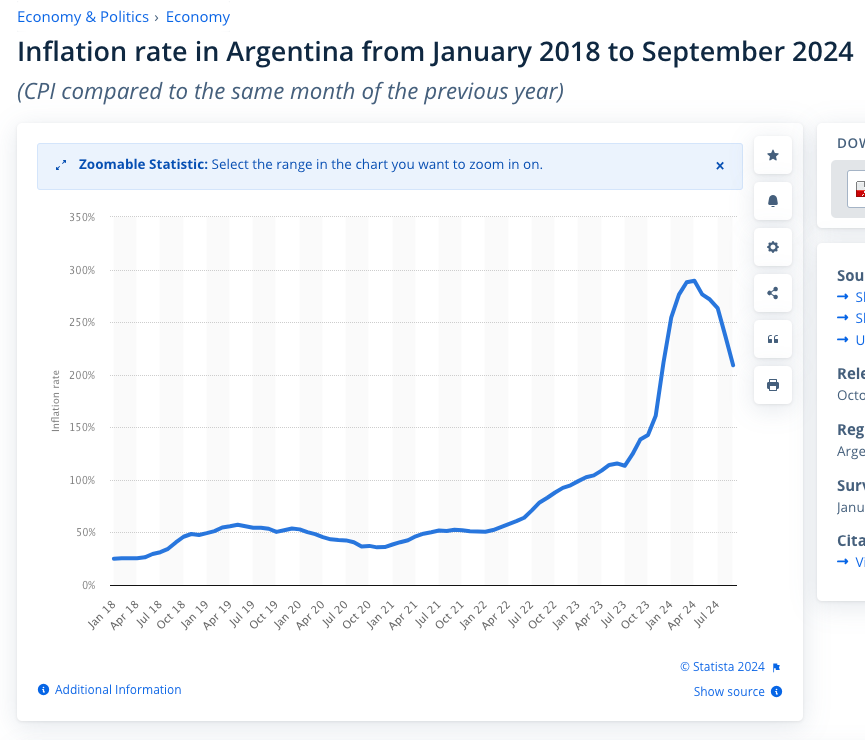

Argentina’s Inflation was running at a whopping 211.4%, and wouldn’t peak for another five months:

Source: https://www.statista.com/statistics/1320016/monthly-inflation-rate-argentina/

After his Election in December, in January of this year, Milei gave his now famous speech at Davos - which AI bots translated for everyone to watch:

And macro investors like Stan Druckenmiller took notice:

And impressively the Merval stock index has nearly doubled so far in 2024.

Why?

Well, since taking office in December 2023, Argentina's President Javier Milei has implemented sweeping austerity measures, cutting overall government spending by approximately 30% in real terms.

His administration has eliminated 13 ministries, fired around 30,000 public employees (about .10% of the labor force, 10 basis points), slashed state subsidies, and made dramatic budget reductions across sectors including infrastructure (-74%), education (-52%), social development (-60%), and healthcare (-28%). His government reported achieving a fiscal surplus in early 2024, the first in nearly 20 years.

These aggressive cuts have generated significant controversy and social upheaval. Argentina had a poverty rate of 41.7% in the second half of 2023, and by January of 2024 that rate had shot up to 57% by one study, later settling to around 53% in official figures for the first half of 2024 (source).

The austerity measures Milei put in place are viewed largely to have led to a Recession, though the Recession ongoing in Argentina may have already been coming when Milei took office.

Nevertheless, the combination of austerity measures and the Recession have sparked mass protests from unions and affected sectors.

Why does any of this matter?

Well at the time of this note’s publication it appears as though Donald Trump and the Republican party will sweep the 2024 elections, winning the Presidency, and both the Senate and the House.

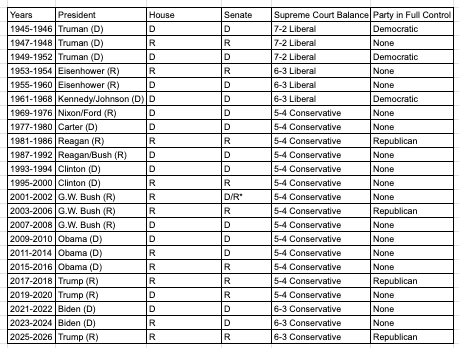

If the House goes Republican, then we are in a rare situation.

As one party having all three branches has only happened five times in the post WW2 era:

1945-1946/1949-1952: Democratic control under Truman

1961-1968: Democratic control under Kennedy/Johnson

1981-1986: Republican control under Reagan

2003-2006: Republican control under G.W. Bush

2017-2018: Republican control under Trump.

(Link)

And importantly for conservatives, never with a 6-3 majority in Supreme Court Justices.

For at least two years, Republicans will have the rule of D.C. in a way that has never been seen in modern times.

For his part, Elon Musk has offered that his focus in the new regime will be in organizing a Department of Government Efficiency. A moniker designed to spell DOGE (a popular crypto token) when put in acronym form.

Source: https://x.com/cb_doge/status/1833320271471907220

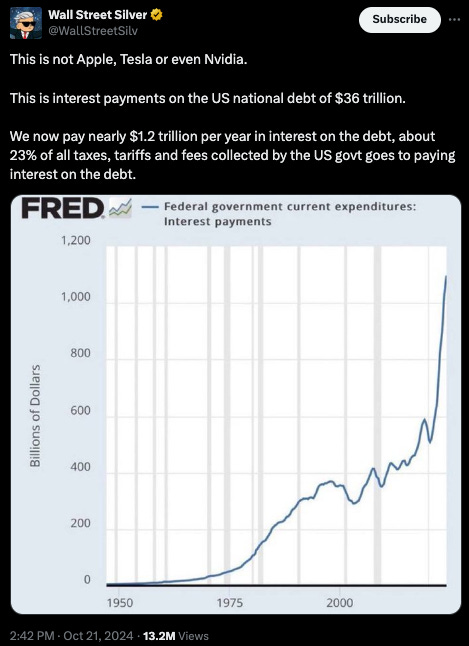

For reference, Fiscal spending does not look great. Most importantly US Interest expenses are surging:

Source: https://x.com/WallStreetSilv/status/1848464997526937666

So, if Musk takes his cues in fiscal cost cutting from Milei, then Argentina might be a good reference point with respect to assets and estimates as we consider what comes next.

That 10 basis point cut in government workers, for example, would translate to about 230,000 government workers in the US.

So how have Argentina’s longer duration bonds and its currency done since Milei took office? I’m glad you asked.

Since taking office in December 2023, Milei's economic policies have produced great results across Argentina's financial markets but at the expense of currency.

In a dramatic early move, the Milei administration devalued the Argentine peso by 54% from 365 to 800 pesos per US dollar, implementing a crawling peg system targeting 2% monthly depreciation thereafter. By May 2024, the peso had weakened to around 934 per dollar, with analysts projecting it to reach 1,200 by year-end.

Against the currency weakness, other financial markets have shown strong performance.

As noted above, the Merval stock index nearly doubled so far in 2024, reaching record highs, with particularly strong gains in energy and utilities sectors.

Similarly, Argentine sovereign bonds have rallied significantly so far in Milei’s tenure, with spreads over US Treasuries falling below 10 percentage points - their lowest level since August 2019.

The 5-year Credit Default Swap value has dropped by about 79%, reflecting improved investor confidence in Argentina's debt despite the ongoing economic challenges and social impact of Milei's austerity measures.

Dollar is Key

In my view, the key indicator in both of these scenarios was the direction of the currency.

With Inflation as the primary concern of the early 1980s, Reagan took actions alongside Volcker to tame Inflation, and absorbed the worst of the coming Recession because he knew voters cared more about stopping the Inflation hemorrhaging they’d just lived through than getting great stock market returns.

A strong Dollar followed and assets responded accordingly.

For Argentina, Javier Milei took a different path, devaluing the Peso while drastically cutting government spending.

So the trick we all get to guess at now is how strong or weak the Dollar will get under Trump.

Moreover, in both of the examples above, Inflation was a more urgent specter in the voting populace.

Current US voters remember the challenge of post Covid Inflation, but it seems less urgent than the Carter years and +200% Argentina Inflation. Current US voters feel the Inflation at the grocery store, and in the pain of higher mortgage prices currently baked into home buying decisions.

The Energy complex that the US currently enjoys is amazing, and Trump is likely to allow for more Energy exploration and development, driving Oil and other Energy costs down.

Meanwhile Trump has gestured at tariffs, most recently on the Joe Rogan Podcast. This would likely create a walled garden for the dollar, which might spike the dollar’s strength temporary as the rest of the world clamors for Dollars to repay obligations.

More likely tariffs are just a negotiating tool.

That said, Trump bringing back jobs and protecting them, while deporting undocumented workers all feels correct.

Trump has also gestured at crypto being a potential component of paying down national debt. Likely that was just chum for crypto voters. The only way it would be meaningful is if the Dollar devalued dramatically.

Trump will likely let Elon cut government programs for a good amount of time - maybe a year or so before reining him in. Part of that will be punitive toward the perceived excesses of the Government, and part of that will be acknowledging how effective Musk has been at cutting costs at Twitter.

However, the USD genie only goes back in the bottle if the long end of the bond market is ultimately tamed.

If that happens, then obviously the Bond, PE, and Commercial Real Estate markets all create oceans of wealth in the US for asset holders.

Crypto

Looking at immediate market implications, the easiest short-term trade is Crypto, as the ouster of Gary Gensler and coming regulatory clarity will encourage innovation cycle.

Boomers probably relinquish the financial markets driver’s seat here. Vance, Musk, Ramaswamy, and the rest are all going to skew towards younger advisors. And the older generations at government agencies will be busy fighting Elon.

So crypto probably gets a chance to run if the USD breaks down.

Summary

Beyond these initial reactions, Trump has shown an ability to be creative in where he finds solutions.

If Trump likes the style of Milei’s reforms, then the USD possibly slides gently down as the fiscal cost cutting, Energy complex, and regulatory picture will all provide an incredible investment platform in spite of USD erosion and an ongoing Recession.

Milei’s reforms launched a new style of bond, and that seems like an option for a Trump who wants to show a clear break with Fiscal spending under the Biden administration.

Unlike the 1980s under Reagan, the vast majority of retail investors today are heavily invested in the S&P 500 and other indexes. Recognizing this, Trump will likely prioritize market performance for its positive effect on voters' sentiment. A weaker USD presents the path of least resistance to achieve this goal, so long as Inflation remains tamed and the long end of the bond market doesn’t continue upwards.

Stocks. Crypto. Trump will love the Asset price inflation of the mid 2010s while side stepping the CPI inflation of the Covid years.

The Fed likely has a natural inclination to keep rates higher during Trump’s Presidency in-spite of potentially subdued Inflation.

Asset price inflation will of course help with Tax revenues - which will be needed if Trump cuts taxes.

This won’t shock anyone, but the long term key to the Dollar will be entitlement spending. If a Republican House and Senate starts to chew on cutting entitlements with a view of a long term defense of the Dollar, and Trump buys into the idea, then my USD calculus would change and the crypto bros will marvel as duration bonds become the greatest thing to own in a generation.

Until next month.